If you are planning to retire in 2024, knowing how much you really need to retire is essential to achieving a satisfying retirement.

This comprehensive guide outlines the critical components for building your retirement fund and pinpoints exactly how much you really need to retire in 2024.

From lifestyle costs to health care and income streams, we’ve got you covered with practical insights to secure your financial future.

Summary

- When you retire, you want to ensure you have the same standard of living that you have now, so it’s important to consider how much income you need each month.

- According to Stash.com, the average individual needs between $1.2 million and $1.5 million to maintain their lifestyle, but most retirees only have between $200K and $250K.

- An annuity with guaranteed income for life can supplement the monthly income you need in order to maintain your current lifestyle.

- Accurately estimating retirement income needs involves assessing lifestyle preferences, anticipated expenses, and existing savings while considering factors like debts, taxes, and living standards.

Need help choosing the best annuity for your unique situation? Have questions about getting an annuity? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

Determining Your Retirement Income Needs

The first step in crafting a successful retirement plan is estimating your desired retirement income. This is not a simple task, as it requires a deep understanding of your personal lifestyle preferences, anticipated expenses, and existing savings.

Think about the lifestyle you want to lead once you retire. Are you dreaming of exotic travels or perhaps a quiet life in a cozy community? The type of lifestyle and activities you anticipate in retirement are significant factors affecting your retirement savings goals.

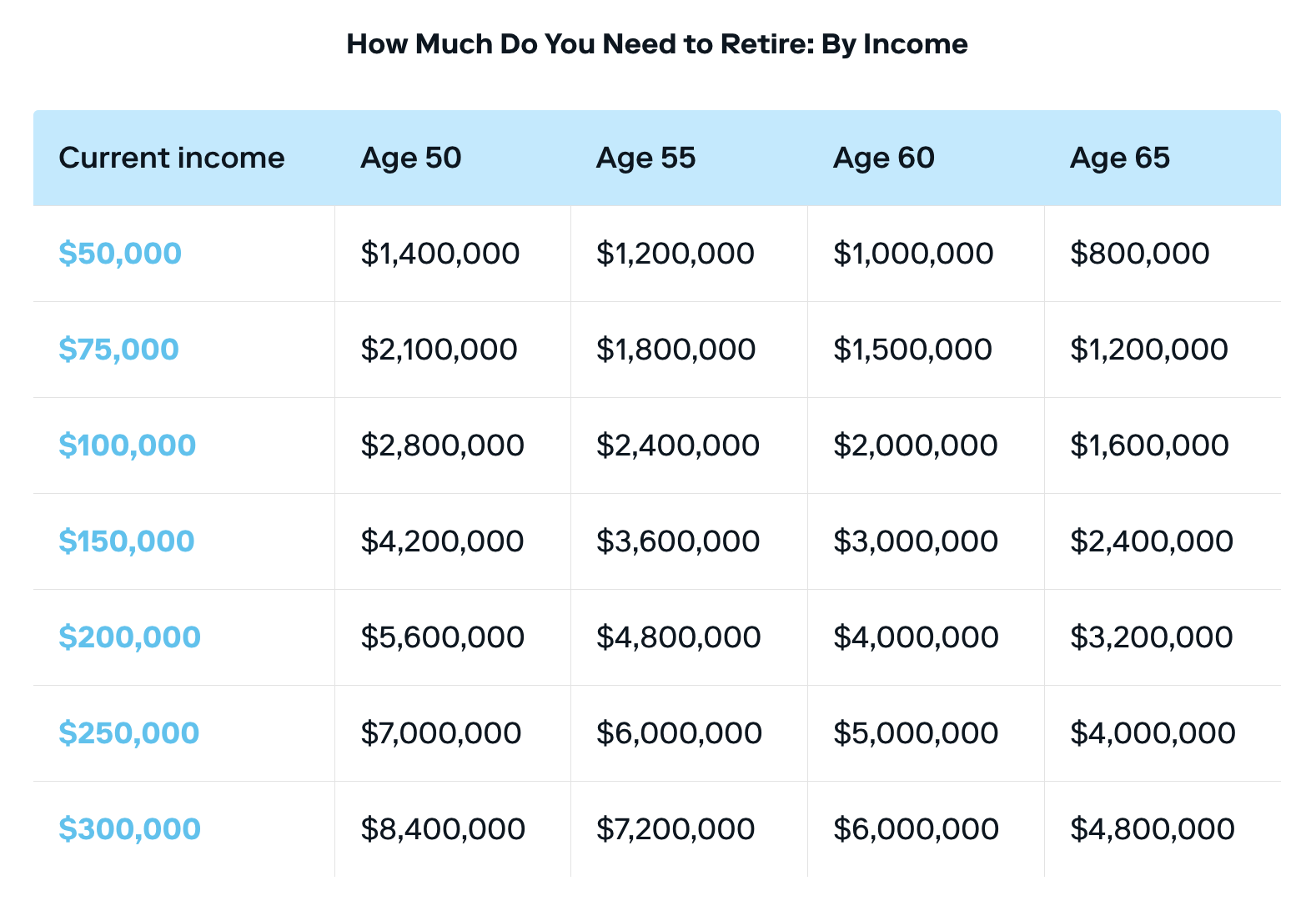

Here’s how much you need saved up in order to maintain your income level:

Source: Stash

However, it’s worth noting that you may need less than you think to maintain your current income with certain annuities. Schedule a call with me to review your options.

Online retirement calculators can also be useful for setting realistic expectations and creating scenarios based on lifestyle preferences and current savings.

These tools consider variables such as your pre-retirement income, retirement age, and retirement lifestyle, guiding you toward a clear savings target based on your pre-retirement salary.

Having a defined retirement target is crucial, as it provides clarity and a concrete goal to aim for during the planning process.

However, it’s important to remember that your retirement planning should not be limited to lifestyle expenses alone. Consider other factors such as:

- Existing debts

- Homeownership status

- State taxes

- The standard of living in your preferred retirement location, taking into account after tax dollars.

These factors can significantly impact your retirement fund requirements and ultimately, the amount you’ll need to retire comfortably.

Analyzing Retirement Income Sources

After estimating your retirement income needs, it’s time to analyze your potential sources of retirement income. These sources can be diverse and include:

- Social Security benefits

- Pensions

- Employer-sponsored plans

- Annuities

- Personal investments

Each source has its own set of rules and benefits, and understanding these nuances will help you build a solid retirement plan that aligns with your financial goals.

1. Social Security Benefits

Social Security benefits are a fundamental aspect of retirement planning. They provide a monthly payment that replaces a portion of income when individuals reduce working hours or retire completely.

If you’ve been contributing to Social Security throughout your career, these benefits can provide significant support during your retirement years. However, to maximize your benefits, it’s important to understand how they’re calculated and when to claim them.

Social Security benefits are calculated based on your 35 highest-earning years, so it’s crucial to work for at least 35 years and verify your annual Social Security statement for accuracy.

Also, consider waiting until your full retirement age or beyond to claim benefits, as this can result in delayed retirement credits and increased monthly payments.

Consider also the potential of spousal and survivor benefits. These benefits enable individuals to claim up to 50% of their partner’s eligible Social Security benefit and might provide the surviving spouse with a higher benefit if their deceased spouse’s Social Security payment was higher.

However, if you continue to work while receiving Social Security, monitor your earnings to ensure you don’t exceed the set limits, which could reduce your benefits.

2. Pensions and Employer-Sponsored Plans

In addition to Social Security benefits, pensions, and employer-sponsored plans such as 401(k) plans, retirement accounts can play a significant role in your retirement income.

A 401(k) is an employer-sponsored retirement plan in which contributions are invested and grow over time, typically with employer matching contributions. These plans are often offered with a Roth option, allowing for after-tax contributions, contrasting with traditional 401(k) plans, which utilize pre-tax dollars.

Pensions, although less common today, provide a specific monthly benefit upon retirement, contributing to a reliable source of income during your golden years. If you’re fortunate enough to have a pension plan, it’s important to understand the terms of your plan and how it will affect your retirement income.

Moreover, retirees can apply for dependent benefits, which provide dependents under 19 with up to 50% of the retiree’s benefit without reducing the retiree’s own Social Security benefits. This can be a significant advantage for those with children still in school.

3. Annuities

Annuities are financial products that can guarantee income for life, thereby reducing the anxiety of potentially outliving your savings.

When you purchase an annuity, you make a lump-sum payment or a series of payments to an insurance company, providing you with periodic payments that can start immediately or at some point in the future.

The predictability of annuities makes them an attractive option for retirees seeking stability in their income streams. With various types of annuities available, including fixed, variable, and indexed, retirees can choose the one that best fits their financial situation and risk tolerance.

- Fixed annuities offer a guaranteed interest rate and a predictable income, making them a safe choice for conservative investors.

- Variable annuities, on the other hand, allow for investment in a selection of funds, which means income can vary based on the performance of the investments.

- Indexed annuities offer a middle ground, with returns tied to a market index but with certain guarantees in place.

One key benefit of annuities is the option to add riders, such as a death benefit or living benefits, which can enhance the annuity’s value to the retiree or their beneficiaries.

See also: How much does a $500K annuity or $1 Million annuity pay per month?

Incorporating annuities into your retirement plan can provide peace of mind and a sense of financial security, knowing that you have a steady income to rely on, regardless of market fluctuations or other economic uncertainties.

4. Investments

Retirement income doesn’t only come from Social Security benefits and employer-sponsored plans. Personal investments can provide an additional income stream and further diversify your retirement portfolio.

Dividend investing, owning municipal bonds, and investing in real estate are investment strategies that can complement annuities and other retirement income sources.

Dividend investing involves purchasing stocks of companies that pay out a portion of their profits to shareholders. This can provide a steady income stream during retirement, supplementing your other sources of income.

On the other hand, municipal bonds offer a means to earn tax-free interest income, making them an attractive option for retirees in higher tax brackets.

Real estate investments can also be an effective way to diversify your retirement portfolio. They have the potential to generate both rental income and capital appreciation over time, providing another layer of financial security during your retirement years.

The Power of Annuities in Retirement Planning

Annuities can play a powerful role in a comprehensive retirement plan. Annuities offer:

- Guaranteed income streams

- Alleviation of concerns about outliving one’s savings

- The benefit of fixing income gaps

- Providing a sense of financial security during retirement.

Income annuities offer a simple and predictable annual income, like receiving a paycheck, making financial management easier for retirees.

This regular income stream can be a great comfort, knowing that you’ll have a consistent flow of money to cover your living expenses, including household income needs and taxable income obligations.

Moreover, annuities can be a powerful tool to combat the effects of inflation. Inflation-adjusted annuities can safeguard retirees’ purchasing power over time, providing a guaranteed income stream for life, including options for joint and survivor annuities with inflation-indexed payments.

This can be particularly beneficial in years of high inflation, ensuring that your retirement income keeps pace with the rising cost of living.

Impact of Retirement Age and Medicare Eligibility

The age at which you choose to retire can significantly affect your retirement income and healthcare coverage. Retiring at an earlier age, such as 62, increases the need for a larger nest egg due to the additional years without work-based income.

It’s therefore essential to consider the financial implications of your retirement age carefully.

Healthcare is a significant concern for many retirees. If you retire before the age of 65, you’ll need to secure alternative health insurance until you become eligible for Medicare. This requires additional funds and planning for unexpected healthcare expenses.

Even after reaching age 65, if you have employer-provided health insurance, you have the option to delay Medicare enrollment, which could be advantageous depending on your work status and insurance coverage.

Despite discussions to potentially increase the Medicare eligibility age to 67, the current age of eligibility remains at 65, affecting many individuals’ retirement timing. Therefore, it’s crucial to keep up-to-date on any changes in Medicare eligibility that could potentially impact your retirement planning.

Joint Annuities for Couples

Joint and survivor annuities can provide peace of mind for couples. Designed to provide a guaranteed lifetime income for both the primary annuitant and the co-annuitant, typically a spouse, these annuities ensure financial support continues for the surviving spouse after the primary annuitant passes away.

Joint annuities offer a range of payout options, including level, reduced, or increasing payments, allowing couples to tailor their retirement income according to their needs.

This can be especially beneficial in providing financial security and stability during the retirement years, ensuring that both spouses can maintain their desired lifestyle.

Inflation Considerations in Retirement Planning

Inflation is an often overlooked factor in retirement planning, but it can significantly impact retirement income and purchasing power.

When saving for retirement, it’s important to consider historical inflation rates, keeping in mind that Social Security benefits adjust for inflation but should not be the main source of income.

Inflation-adjusted annuities can safeguard retirees’ purchasing power over time, providing a guaranteed income stream for life, including options for joint and survivor annuities with inflation-indexed payments. Moreover, to maintain purchasing power, it’s advisable to:

- Reevaluate your investment portfolio to include stocks that historically outpace inflation

- Invest in inflation-protected bonds such as TIPS that adjust for inflation

- Consider commodities that often perform well during high inflation

Additionally, saving more and spending less is a proven strategy to ensure enough funds during retirement to cope with inflation.

This simple yet effective strategy can buffer against inflation’s eroding effects on your retirement savings.

Seeking Professional Guidance

The journey to retirement can be complex and challenging, necessitating the guidance of a professional annuity advisor. These experts can:

- Identify potential weaknesses in your retirement plan

- Provide tailored advice to manage risks and blind spots

- Manage complex financial decisions with expertise

Consulting with a annuity expert can significantly reduce time and stress, especially when seeking legal or tax advice, as they can provide valuable tax advice tailored to your specific needs.

Conclusion

Retirement planning is not a one-size-fits-all process. It involves a strategic blend of savings, investments, and careful planning, considering personal lifestyle choices, anticipated expenses, and factors such as inflation and healthcare costs.

From determining your retirement income needs to analyzing retirement savings sources and considering the impact of retirement age and Medicare eligibility, each step of the journey requires careful thought and planning.

Booking a call with an annuity expert can provide personalized guidance on annuity strategies and help you make informed decisions about your retirement income.

I can help you:

- Determine the best solution for your unique circumstances

- Navigate and make crucial decisions during your financial journey

- Find the best annuities for your unique situation

By clicking here to schedule a call, I can take a look at specific annuity options and strategize on how to minimize surrender charges.