If you have $1 million available for purchasing an annuity and you are wanting to ensure a comfortable retirement. Then finding the right annuity is important

Buying the right annuity can provide the highest income stream that can replace your job and provide financial security for your golden years.

But what does a $1 million annuity pay, and how can you maximize it?

In this article, we’ll learn how much income you can get from a $1,000,000 annuity, and learn how to make the right choices when dealing with annuities.

Summary

- The projected monthly payment for a $1 million annuity acquired between the ages of 60-70 ranges between $6,000 and $9,500. However, payouts can depend on age, which annuity provider you use and other factors.

- Maximize your payouts by comparing all the available annuity providers.

- It’s important to consider the safety rating of the annuity provider when buying an annuity. I typically recommend using A rated annuity companies. In some cases, a B++ rated company might be better.

- Professional advice is essential for assessing suitability of an annuity in one’s broader retirement strategy.

Need help finding the best annuity for your unique situation? Want to see how much each annuity provider will pay you? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

The Monthly Income Potential of a $1 Million Annuity

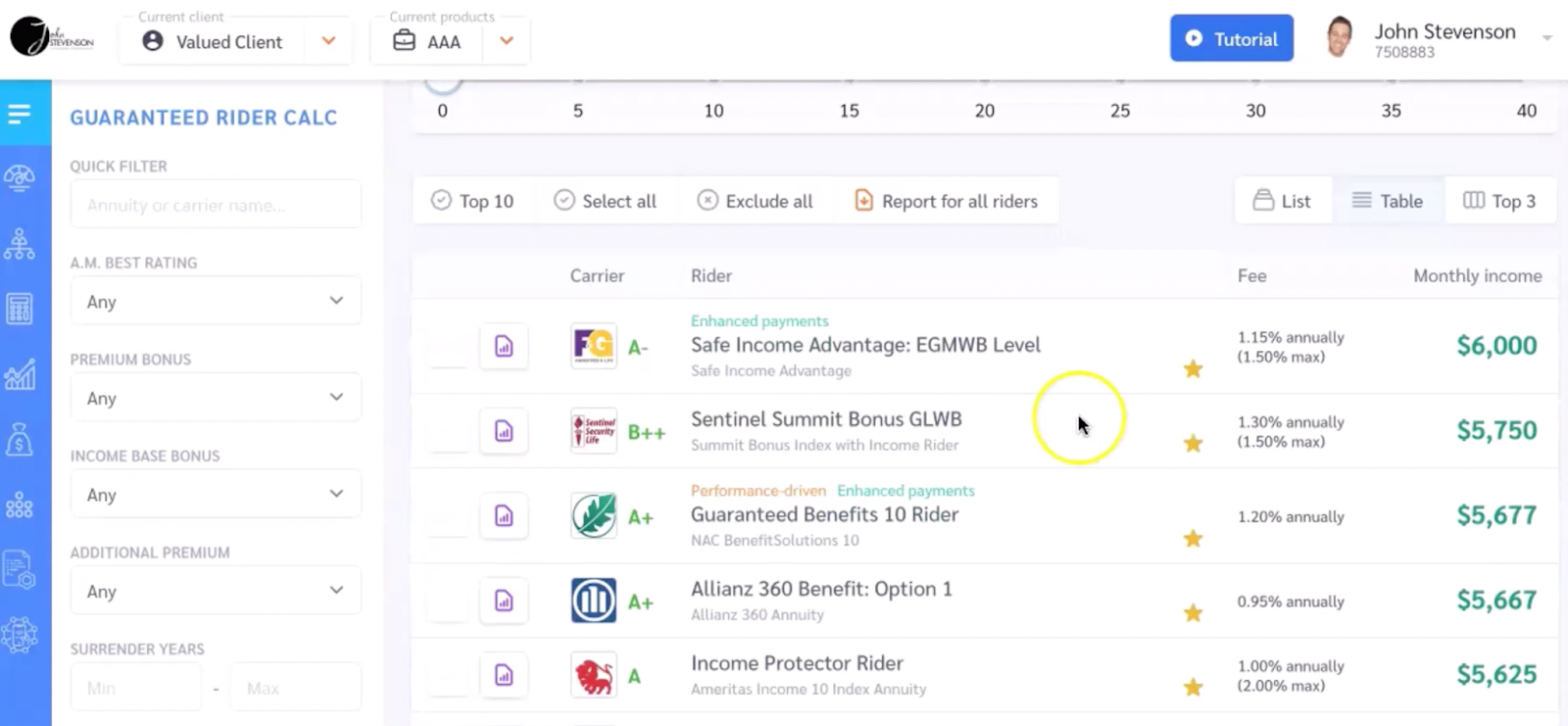

The projected monthly payment for a $1 million immediate annuity acquired at the age of 60 ranges between $5,600 and $6,000, as seen here:

These figures, however, are not set in stone.

They can fluctuate based on several factors that influence the annual payout of a $1 million annuity, including:

- The interest rate at the time of purchase

- The length of the annuity term

- The type of annuity (fixed or variable)

- The annuity provider’s fees and charges

- Any additional riders or features added to the annuity

It’s important to carefully review your annuity contract and consult with a financial advisor to understand the potential earnings and risks associated with a $1 million annuity, as investing involves risk.

These factors include:

- The type of annuity

- Age at annuity purchase

- Interest rate

- Chosen payout option

These seemingly minute details can significantly impact your monthly income and overall financial security.

Therefore, gaining a comprehensive understanding of your personal financial situation before making a decision is imperative.

Want to see how much an annuity would pay you? Click here to schedule a call.

Single vs. Joint Annuity Payments: A Comparative Look

When it comes to annuities, one size doesn’t fit all. This is particularly true in the case of single and joint annuity payments. A single annuity is based on one life, while a joint annuity provides income for both the annuitant and their spouse or partner.

This difference might seem inconsequential at first glance, but it can significantly influence the payout you receive and the financial security of your spouse or partner.

In a joint annuity arrangement, both the annuity owner and their spouse are entitled to receive income payments for the duration of their lives.

On the other hand, annuity payments for single beneficiaries generally cease upon the annuitant’s death. Some annuities also offer a lump sum payment option, which can be beneficial in certain situations.

Therefore, considering factors such as retirement income, benefits, and payment amount is vital when comparing single and joint annuity payments.

Adjusting Payouts for Age: What You Need to Know

Age plays a significant role in determining the payout amount of an annuity. The general rule of thumb is that purchasing the annuity at an earlier age results in a higher rate of payment. Conversely, annuity payout rates may decrease notably around the age of 85. So, what does this mean for you?

This implies that strategic planning is key to optimizing your annuity payout.

For instance, you can structure annuity payments for a set number of years or choose an inflation-adjusted annuity, which can provide a steady income stream right after the purchase.

Such strategies can help you navigate the impact of age on annuity payouts and ensure you receive an income that matches your lifestyle and retirement goals.

Monthly Breakdown: Navigating Annuity Payment Options

Annuities indeed have the capability to offer a fixed or variable monthly income, providing a steady income during retirement. This flexibility allows you to make strategic choices that align with your financial goals and risk tolerance.

Whether you choose regular payments or a lump sum payout, getting a good grasp of these options is crucial for making an informed decision that fully exploits your annuity’s potential.

The Impact of Timing: Deferring Your Annuity for Increased Income

Now that we’ve explored the various factors influencing your annuity payout, let’s delve into the role of timing.

More specifically, how can deferring your annuity lead to increased income in the future? The answer lies in the power of compound interest and the tax advantages associated with deferred annuities.

Deferring an annuity allows for growth over time. A longer deferral period can result in a higher income in the future. Furthermore, deferred annuities often provide higher returns as a result of the extended accumulation of earnings on a tax-deferred basis.

However, it’s important to recognize that delaying an annuity to an older age generally results in increased payout rates, depending on the specific terms of the annuity.

Planning Ahead: The 5-Year Deferral Strategy

The 5-year deferral strategy in annuities pertains to a term deferred annuity that enables the postponement of receiving payments for a span of five years.

During this deferral period, the balance of the annuity continues to accrue, resulting in higher monthly income once the payments commence. Sounds enticing, doesn’t it?

However, like every financial strategy, the 5-year deferral strategy is not without its drawbacks. It limits liquidity, which can result in costly access to funds before the deferral period ends. Moreover, there may be penalties for early withdrawals from fixed annuities.

Thus, balancing the potential advantages against the drawbacks and evaluating the strategy in the context of your financial goals and retirement plan is of paramount importance.

Comparing Immediate vs. Deferred Annuity Rates

Choosing between immediate and deferred annuity rates can seem like a daunting task. An immediate annuity commences payments immediately and generally has lower rates due to the immediate payout structure.

On the other hand, deferred annuities offer potential tax-deferral benefits and the chance to gain additional income in later retirement, which can be especially advantageous for long-term financial planning.

However, the decision between the two should not be made in a vacuum. It’s vital to take into consideration factors such as the age and health of the annuitant, the effect of inflation on payment value, and the financial stability of the annuity carrier.

Therefore, a comparative analysis of immediate and deferred annuity rates, considering these factors, can help you make an informed decision.

Annuity Carriers and Their Offers: Finding the Best Rate

Choosing the right annuity carrier is just as important as deciding on the type of annuity. With a wide range of annuity carriers in the market, each offering unique terms and rates, it can be challenging to find the best fit for your retirement plan.

Thus, when choosing an annuity carrier, it’s important to take into account multiple factors such as:

- Timing

- Rate of return

- Payout term

- Fees

- Death benefits

Notably, leading annuity carriers like Massachusetts Mutual Life Insurance Company, North American Company, and American Equity have exhibited growth in recent years. These carriers offer a variety of annuity options, each with its own set of features and benefits.

But how can you choose the right one? Let’s dive in and analyze these carriers to find the best rate for your retirement plan.

Comprehensive Carrier Analysis: Maximizing Lifetime Income

To make a well-informed decision, conducting a thorough analysis of annuity carriers is paramount. This involves comparing their payout rates, which can differ based on factors such as:

- the amount of the bonus credit

- increased charges

- the duration of holding the annuity

- any additional features or benefits offered

By comparing these factors, you can determine which annuity carrier offers the best value for your needs.

Moreover, the financial stability of annuity carriers is another essential factor to consider. This can be assessed through financial strength ratings and coverage by state guaranty funds.

Carriers also calculate their payout rates by considering factors such as the annuitant’s age, the duration of the payment period, and an assumed rate of return.

Hence, a comprehensive career analysis can help you maximize lifetime income from an annuity.

Joint vs. Single Annuities: Carrier-Specific Advantages

Each annuity carrier offers unique advantages for joint and single annuities. For instance, joint annuities offer guaranteed income distributions for the duration of both annuitants’ lifetimes, ensuring payments continue to a secondary annuitant after the primary annuitant’s death.

On the other hand, single annuities generally provide higher payments as they ensure income for only one individual.

Therefore, comprehending the carrier-specific benefits for joint and single annuities is vital in selecting the appropriate annuity for your retirement plan.

Annuity Calculator Demystified: Tailoring Your Retirement Plan

Navigating the world of annuities can seem overwhelming. But fear not! Tools like an annuity calculator can help simplify the process. An annuity calculator serves as a tool that offers personalized results to assist in retirement planning.

It can provide substantial benefits to your retirement planning by delivering precise and customized outcomes that aid in making well-informed decisions.

To effectively utilize a fixed annuity calculator, it is necessary to input details such as the initial investment amount, the anticipated interest rate, and the term length of the annuity.

These specific details enable the calculator to provide a precise estimate of the annuity’s future value, helping you tailor your retirement plan according to your financial goals.

From Annual to Monthly: Understanding Your Annuity Payments

Understanding your annuity payments is fundamental to retirement planning. A simple formula can help you determine your monthly payments based on annual income: Monthly Payment = Annual Income / 12.

However, these fixed payments may vary based on interest rates and market performance, as annuities pay differently under various circumstances.

For instance, a $1 million annuity is estimated to provide a monthly income of approximately $7,500. While this estimate can serve as a useful baseline, it’s essential to bear in mind that these figures can vary based on several factors, including:

- the type of annuity

- interest rates

- deposit amount

- life expectancy

Therefore, switching between annual and monthly views can provide valuable insights into your annuity payments.

Want to see how much an annuity would pay you? Watch this video to see how I can show you (at no cost to you).

Customizing Annuity Inputs: Aligning with Financial Goals

While annuities offer preset terms and conditions, you have the power to customize certain aspects of your annuity plan. These customizable factors encompass:

- The income growth factor

- Riders

- Deposit amount

- Age at the time of purchase

- The terms, fees, structure, and payouts of the annuity plan

These customization options allow you to align your annuity inputs with your retirement financial goals. This involves:

- Evaluating your retirement plan

- Choosing the appropriate annuity plan

- Optimizing income and expense inputs

- Revisiting your goals

Therefore, comprehending and customizing these inputs can significantly contribute to the realization of your retirement goals.

Booking a Consultation: Next Steps in Annuity Planning

You’ve learned about the various aspects of annuities, from understanding the potential of a $1 million annuity to customizing annuity inputs. But what’s the next step in annuity planning?

Booking a free consultation with a trusted advisor can be a wise move.

Advisors play a critical role in annuity planning.

They can help individuals with:

- Assessing how annuities integrate into their broader retirement strategy

- Offering advice on organizing annuities for income and safeguarding against inflation

- Providing comprehensive financial planning support

Ready to get started? Click here to schedule an appointment.

Summary

As we’ve seen throughout this blog post, a $1 million annuity can be a powerful tool in creating a secure retirement.

Whether you opt for a single or joint annuity, immediate or deferred payouts, or work with a specific annuity carrier, the decisions you make can significantly impact your financial security in your golden years.

However, understanding the complexities of annuities and making well-informed decisions requires research, planning, and professional advice.

With the right approach, you can unlock the potential of a $1 million annuity and secure a comfortable and fulfilling retirement.

Have more questions about annuities? Click here to book a free consultation.

In this consultation, I can provide personalized advice and strategies, guiding you to make informed decisions about annuities and optimize your retirement planning.

I can also compare all the annuities so you can see which one is best regardless of the commissions associated with the annuity.

During the consultation, you will:

- Be able to compare different annuity options

- Learn how to grow & protect your wealth in retirement

- Get all of your questions about annuities answered

I look forward to speaking with you soon!