Are you considering how to turn your $500,000 into a steady income stream that will last the rest of your life. If so, a $500K guaranteed income annuity can help!

But, what does a $500K annuity pay? In this article, we’ll go through how much income a $500k annuity pays, and how it affects your retirement income plan.

Summary

- A $500K annuity can pay approximately $35,000/year to $55,000/year in guaranteed lifetime income. However, the payout from a $500K annuity depends on factors including your age, marital status, the type of annuity you get, payout options chosen and other factors.

- Maximizing a $500K annuity payout involves strategies such as deferring income, diversifying your investment portfolio, and consulting a professional for personalized guidance.

- A $500K annuity can bridge the retirement income gap, and its effectiveness depends on analyzing pensions, Social Security, and assets, as well as selecting the right annuity products and companies based on payout rates and customer satisfaction.

Need help deciding whether annuities are a worthwhile option for your retirement needs? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

Estimating a $500K Annuity Payout

Determining the payout of a $500,000 annuity requires careful consideration. A myriad of factors come into play, including:

- The initial investment amount

- Interest rate

- Selected payout options

- Personal considerations such as age and the choice of receiving income immediately or later

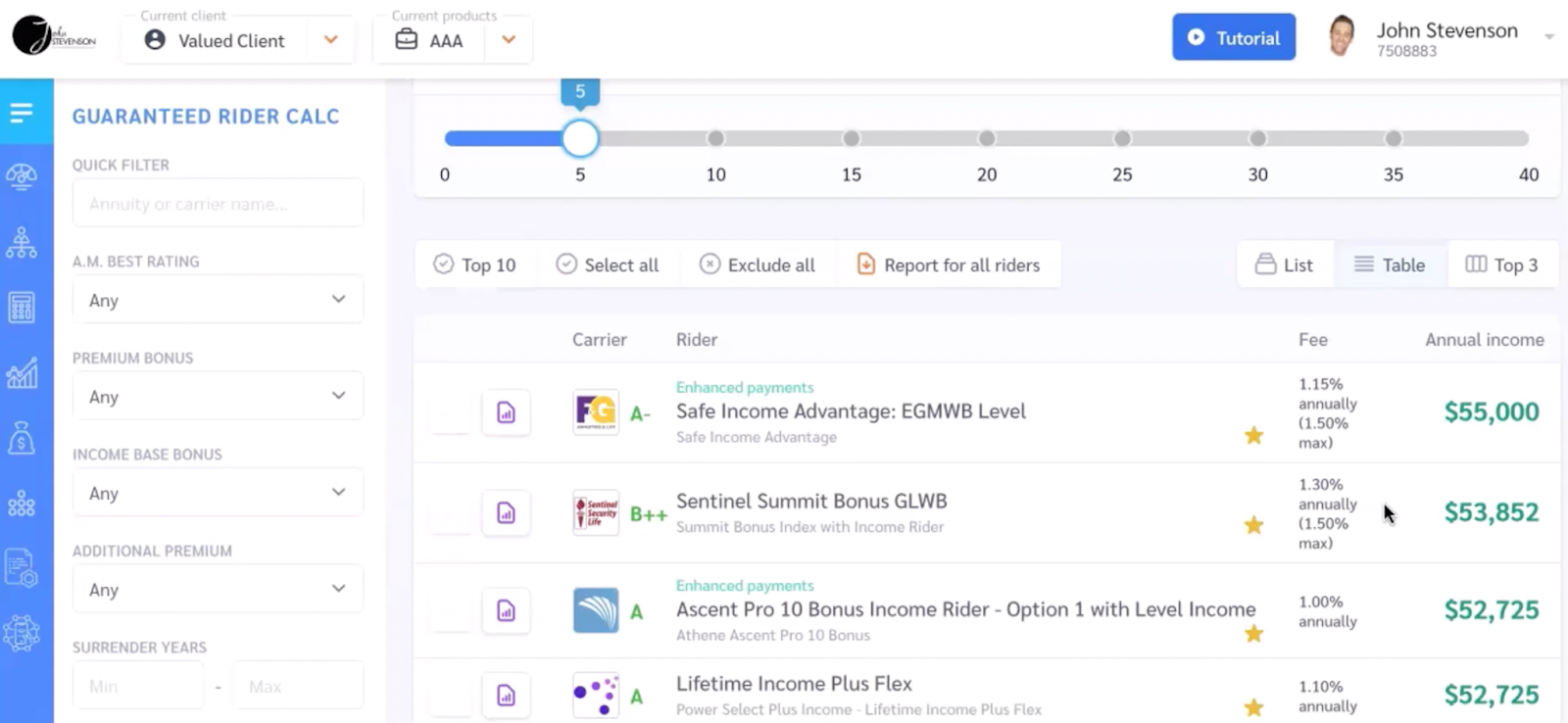

One of the most practical tools to simplify this process is to compare all the different annuity payouts based on your unique circumstances.

If you watch this video, you’ll learn how I can show you all your annuity payout options based on your unique circumstances.

This allows you to actually see and compare the best annuities available for you.

Another good option is an annuity calculator. An annuity calculator does the heavy lifting by taking into account all these variables to provide an estimate of your annuity payments.

Nonetheless, bear in mind that your payment distribution, once selected, cannot be altered. This is a critical point to remember, whether you’ve chosen an immediate annuity and started receiving income right away, or opted for a deferred annuity with income payments set to commence at a later date.

Age and Life Expectancy

Age and life expectancy significantly impacts annuity payouts. The mechanics are straightforward – shorter life expectancies equate to higher payments. This is why women, who typically have a longer life expectancy than men, receive smaller annuity payouts.

The question now is, how do you estimate your life expectancy for the annuity calculator? It’s a simple subtraction of your current age from the average life expectancy for your sex. But remember, these are averages, and actual life spans can differ.

An immediate annuity calculator can help estimate the payouts based on life expectancy and other factors.

Types of Annuities

Exploring the annuity landscape reveals various kinds: fixed, variable, and indexed. Each type has unique characteristics that impact how much monthly income you receive during the payout phase.

A fixed annuity offers a stable return, easing your financial planning process. It guarantees a consistent interest rate on your investment over a predetermined duration, providing a dependable guaranteed lifetime income.

On the other hand, a variable annuity, which is a type of annuity contract, combines the steady income of annuities with stock market growth potential, albeit with an associated mortality and expense risk charge.

Lastly, an indexed annuity provides protection against losses while enabling potential growth, serving as a safety net during market declines.

Payout Options

Annuity payout options significantly influence the amount and duration of payment. If you’re a fan of windfalls, you might opt for the lump-sum payment option.

This allows you to withdraw the full account value of your annuity in one go, after you reach the age of 59 ½ without penalties, albeit subject to income taxes for that year.

Alternatively, you might prefer the consistency of a fixed payment amount. This option ensures that you receive a set monthly payment until your annuity’s balance is exhausted. If you fancy a combination of both, the fixed-length payout option could be your perfect match.

It guarantees that your annuity payments are provided for a specified time period. If you pass away before the end of the chosen period, the remaining periodic payments are passed on to your heirs.

Strategies for Maximizing a $500K Annuity Payout

With the basics established, let’s explore how to maximize your $500K annuity.

Strategies for maximizing your annuity payout include deferring income, diversifying your portfolio, and consulting a trusted advisor.

Deferring your annuity income can lead to increased interest rate credits and mortality credits, potentially enhancing your payout amount. Here are some strategies to optimize your annuity payout:

- Implement the bucket strategy to diversify your portfolio.

- Explore a bond market hedge to protect against interest rate fluctuations.

- Consider wealth transfer options to maximize your legacy.

- Consult with an advisor for guidance on annuitization, laddering annuities, or exploring products that guarantee higher payments.

An annuity expert can help you navigate the complexities of annuities and provide practical advice tailored to your specific needs.

Deferring Income

Deferring annuity income refers to delaying income payments, typically until retirement. This strategy involves a careful consideration of factors such as:

- the type of annuity

- potential tax implications

- your age

- the size of your investment portfolio

The beauty of deferring annuity income is that it gives your contract more time to grow, potentially resulting in higher future income increments.

For instance, delaying the receipt of a $500,000 annuity income generally leads to increased monthly payments compared to immediate payouts, thus maximizing the annuity’s value.

Diversifying Portfolio

Diversifying your portfolio can be likened to distributing your eggs across various baskets. It helps balance risk and return, ensuring a more stable income stream. When diversifying a portfolio with an annuity, consider integrating various types of investments, including stocks, bonds, and cash.

The allocation of assets for annuity investments also plays a crucial role in spreading risk and diversifying the investment portfolio, reducing the risk of depleting funds during retirement. Your risk tolerance significantly influences this diversification strategy.

An investor with low risk tolerance might prefer conservative investments like bonds and cash, while someone with higher risk tolerance might allocate a larger portion of their portfolio to stocks in pursuit of greater returns.

Consulting an advisor

The annuity landscape, including annuity contracts, can be challenging to traverse. This is where an advisor comes in handy. They can provide personalized guidance on maximizing annuity payouts and selecting the best annuity products.

By analyzing the annuity that meets your financial objectives and assessing factors like income, growth, legacy, and care, they can identify the best annuity products for you.

Bridging the Retirement Income Gap with a $500K Annuity

A $500K annuity can serve as a bridge to fill your retirement income gap. The retirement income gap is the shortfall between essential expenses and other reliable income sources such as a pension and Social Security.

Determining the required income for retirement involves developing a budget tailored for retirement, identifying expenses and sources of income, and making adjustments as necessary.

When considering the allocation of assets for annuity investments, it is advisable to allocate no more than 50%-70% of your liquid net worth to an annuity due to the surrender charge associated with excess withdrawals during the surrender charge period.

That way, you can ensure a balance between guaranteed income and liquidity.

Analyzing Pension, Social Security, and Assets

Evaluating your pension, Social Security, and assets is essential in forming your retirement income. For instance, single retirees can anticipate an average monthly pension of approximately $1,500, whereas couples typically receive around $2,500.

Social Security benefits are determined by your average indexed monthly earnings (AIME) during the 35 highest-earning years after reaching the age of 21.

Evaluating the value of your personal assets involves totaling all your assets and then subtracting any liabilities from the total. All these sources of income together form the cornerstone of your retirement income.

Allocating Assets for Annuity Investments

A balanced portfolio approach is vital in allocating assets for annuity investments. This involves dividing your retirement contributions among stocks, bonds, and annuities in a manner that is consistent with your retirement timeline and risk tolerance.

The annuity industry typically advises that individuals allocate no more than 50% of their investable assets in annuities to maintain a balance between guaranteed income and liquidity. If your income needs are higher than what that ratio will provide, then it is advisable that you don’t invest more than 75% of your total liquid assets into an annuity.

Your allocation can be adjusted based on factors such as age and income, with a potential allocation being 40% in stocks, 25% in bonds, and 35% in annuities.

Selecting the Best Annuity to Bridge the Gap

Choosing the right income annuity product can help bridge the gap between your current income and your desired retirement income.

When choosing an annuity product to bridge the retirement income gap, it’s crucial to consider the performance of investments, which directly impacts the income you receive, and your personal risk aversion.

Immediate fixed annuities and period certain income annuities are considered the most suitable types for bridging the retirement income gap. Fixed annuities offer a stable and predictable income stream that can complement other retirement income sources such as Social Security.

On the other hand, variable and indexed annuities provide a guaranteed stream of income during retirement and principal protection, respectively, making them versatile instruments for bridging the retirement income gap.

Annuity Companies and Their Payouts

Choosing the appropriate annuity provider is as crucial as picking the right annuity product. This involves comparing annuity companies and their payouts to select the best provider for your $500K annuity.

The payouts of various annuity companies are determined based on the following factors:

- The annuitant’s life expectancy, which encompasses factors such as age, gender, and health status

- The specific type of annuity chosen

- The selected payment duration

- The prevailing interest rates.

Comparing Annuity Providers

It is vital to evaluate average rates, typically ranging from about 5.78 percent to 7 percent, when comparing annuity providers. Keep an eye out for administrative fees, mortality expenses, and potential flat fees, as these can eat into your annuity’s value.

It’s also advisable to analyze the financial stability of an annuity provider. You can do this by checking the ratings provided by prominent rating agencies like Fitch, Moody’s, and S&P.

Watch this video to see how I can compare all the top annuities for you.

Top Annuity Companies for $500K Annuities

The top choices for $500K annuities include:

- Athene Annuity

- Allianz Life Insurance Company

- North American Company

- American Equity Investment Life Insurance Company

Click here to compare all the best annuity options.

Book a Call for Personalized Annuity Strategies

Booking a call with an annuity expert can provide you with personalized guidance on annuity strategies, and help you make informed decisions about your retirement income.

They can help you with:

- Navigating complex investments

- Making individualized recommendations

- Providing support as needs change over time

- Helping you reach your financial goals, including maximizing the use of annuities

Click here to schedule a call.

Conclusion

A $500K annuity can be a powerful tool in your retirement planning toolkit.

From estimating your annuity payout based on age, life expectancy, type of annuity, and payout options, to strategies for maximizing your annuity payout through deferring income, diversifying your portfolio, and consulting an advisor there’s a lot to consider.

Have more questions about annuities? Click here to book a free consultation.

In this consultation, I can provide personalized advice and strategies, guiding you to make informed decisions about annuities and optimize your retirement planning.

I can also compare all the annuities so you can see which one is best regardless of the commissions associated with the annuity.

During the consultation, you will:

- Be able to compare different annuity options

- Learn how to grow & protect your wealth in retirement

- Get all of your questions about annuities answered

I look forward to speaking with you soon!