Are you looking for the best fixed annuity rates from 1 to 20 years? This guide will show you what kind of income you can expect from fixed annuities ranging from 1 year to 20 year terms.

In this article, we’ll compare the different fixed annuity providers and explain how fixed annuities can help you in retirement when compared against other investment options.

Summary

- Fixed annuities offer a secure principal and a guaranteed fixed interest rate, which vary with the term of the annuity, providing higher rates for longer commitments such as 3-, 5-, 7-, and 10-year terms.

- Generally speaking the longer the annuity term, the higher your income can be.

- Different insurance companies offer different amounts of income from a fixed annuity. For this reason, it’s a good idea to work with a financial advisor who can compare ALL the fixed annuities from all the top insurance companies. Watch this short video to see how I can do this for you.

- There are several fixed annuity options to cater to different investment durations and risk profiles, ranging from short-term (1-4 years) to mid-term (5-10 years) and long-term (15-20 years), each offering specific benefits such as tax deferral, stability, and guaranteed income.

Need help choosing the best type of annuity for your unique situation? Have questions about getting an annuity? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

Understanding Fixed Annuity Rates Across Different Terms

Insurance companies offer fixed annuities as a form of retirement savings instrument. It mirrors the characteristics of a Certificate of Deposit (CD), promising a fixed rate of return over a predetermined period.

What sets fixed annuities apart is the security of principal and the assurance of fixed interest rates they provide.

Tip: The term of the annuity can influence the variation in fixed annuity rates. The rates can also change each month. So to see the latest rates, please click here to schedule a call (we’ll go through the rates together) or use the annuity search feature on our website.

At the time of writing this article, the best fixed annuity rates for the most competitive durations are as follows:

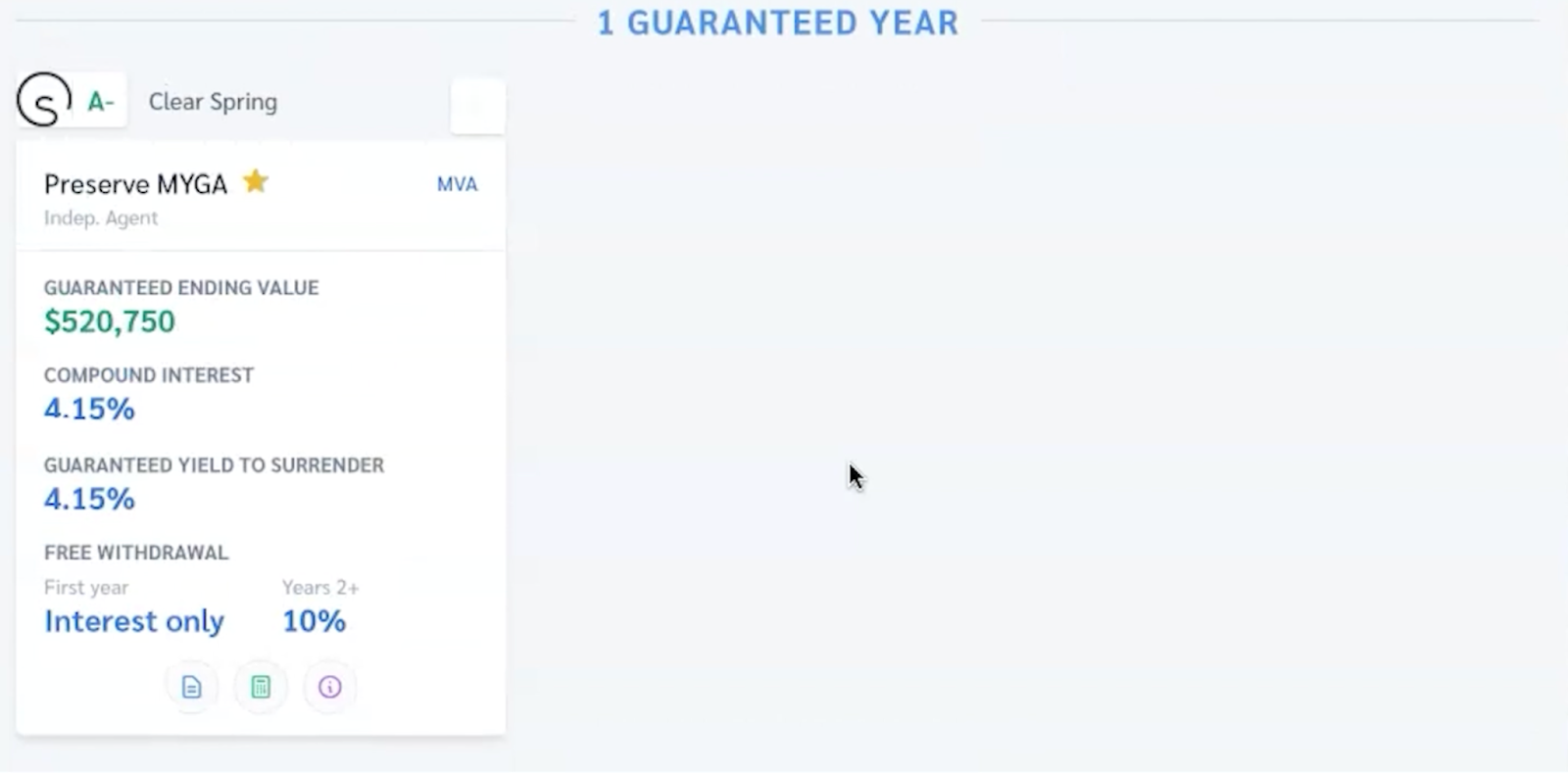

1 Year at 4.15%:

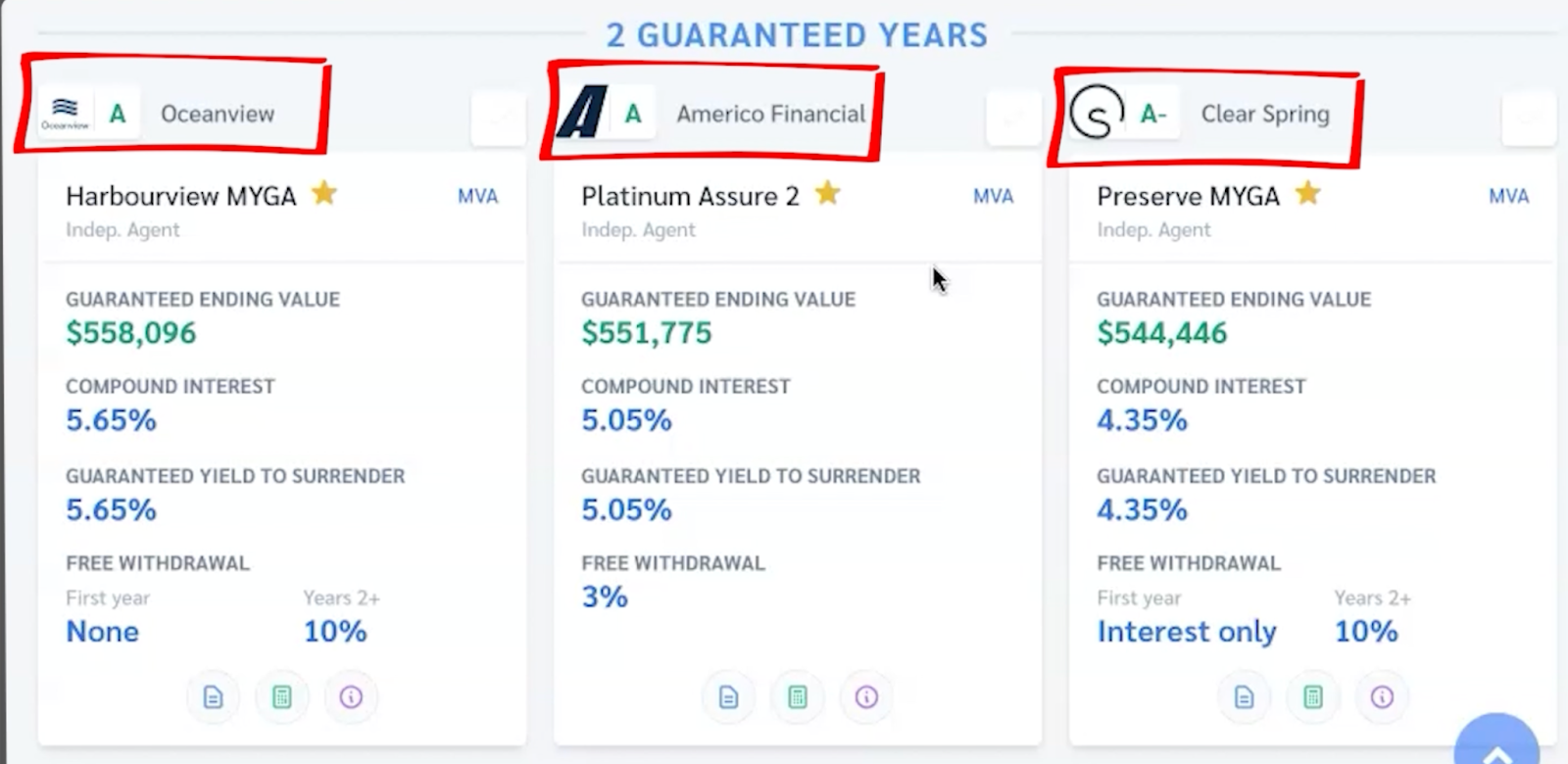

2 years at 4.35% to 5.65%:

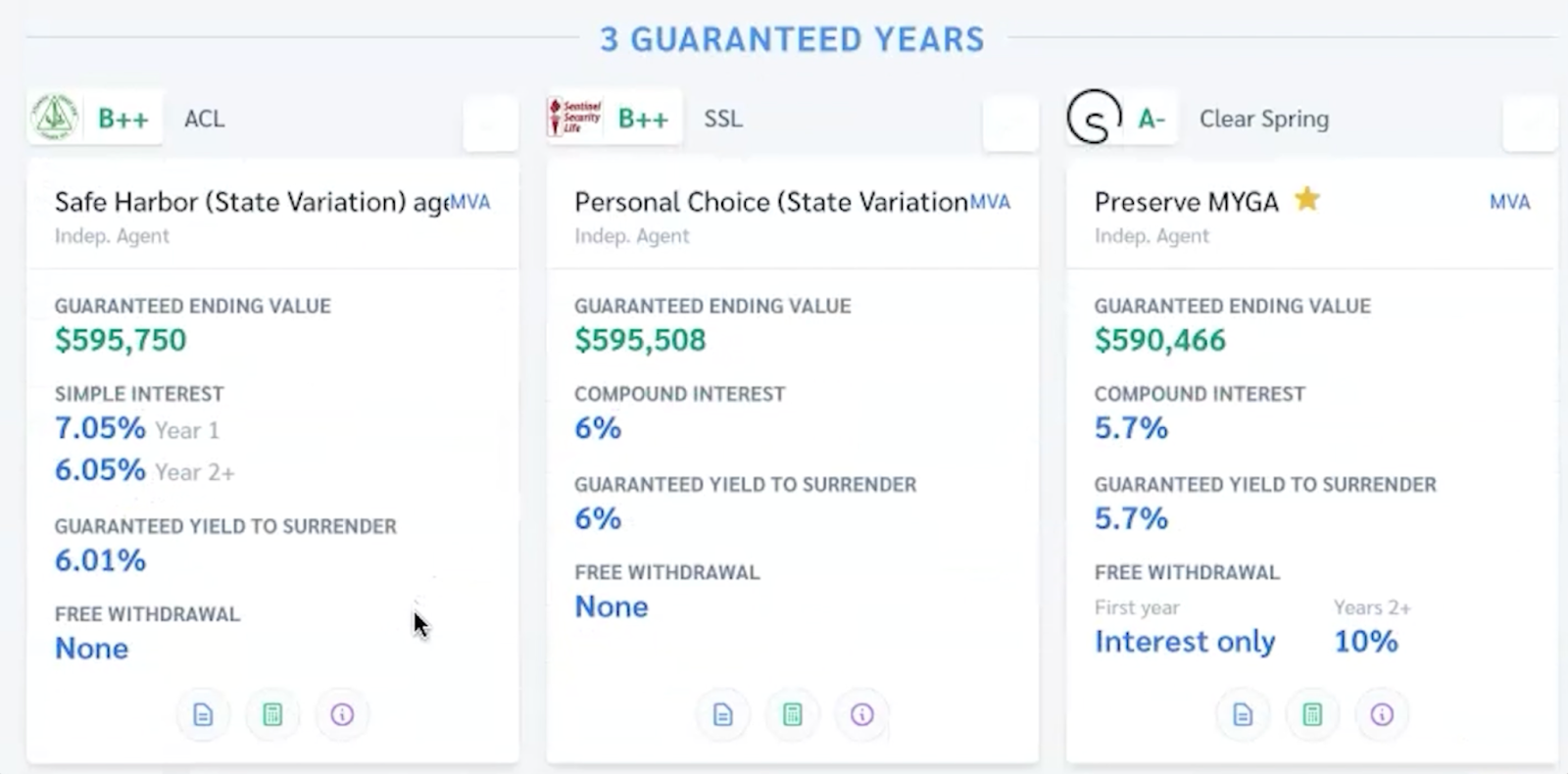

3 years at 5.7% to 7.05%

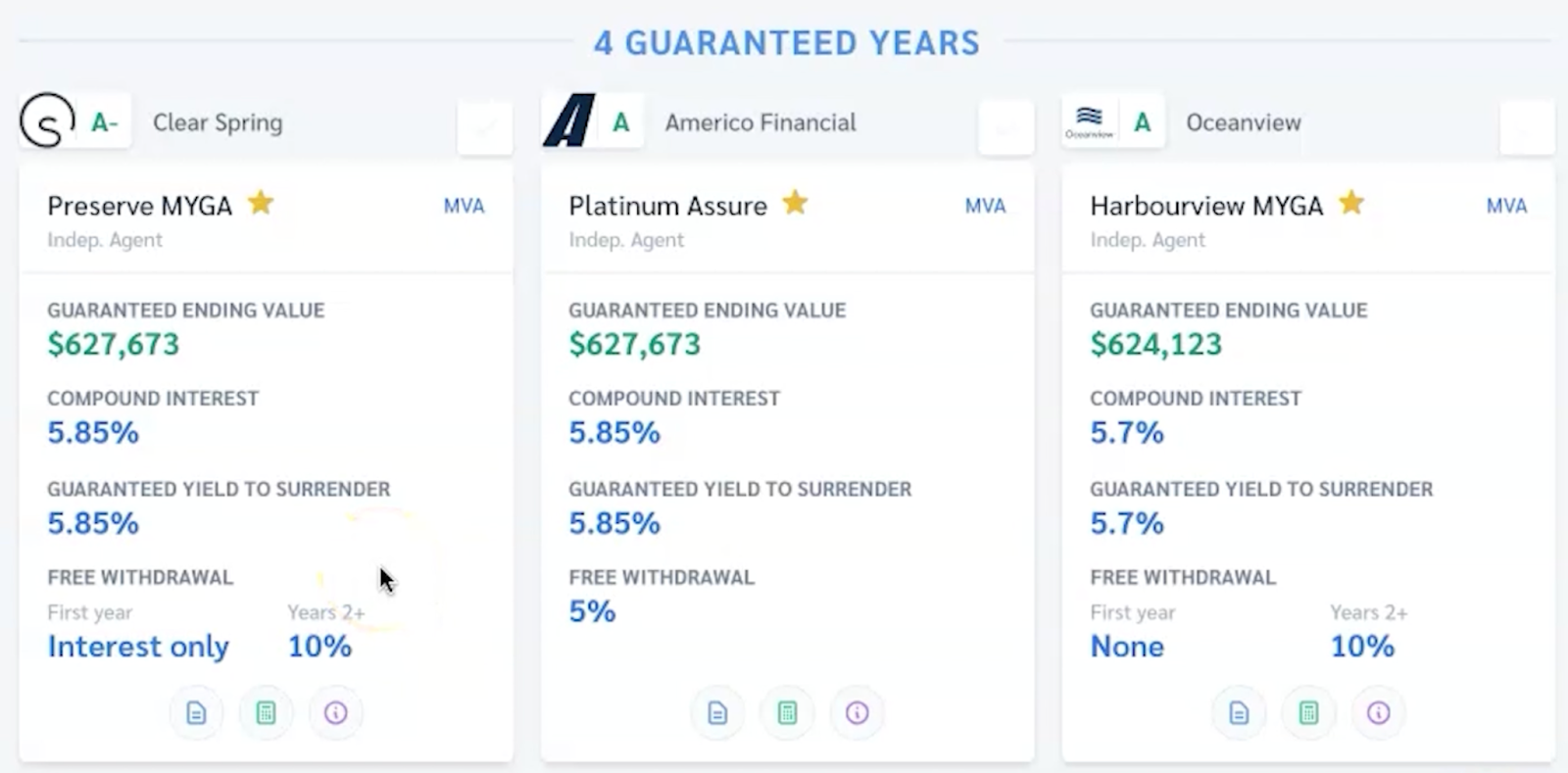

4 years at 5.7% to 5.85%:

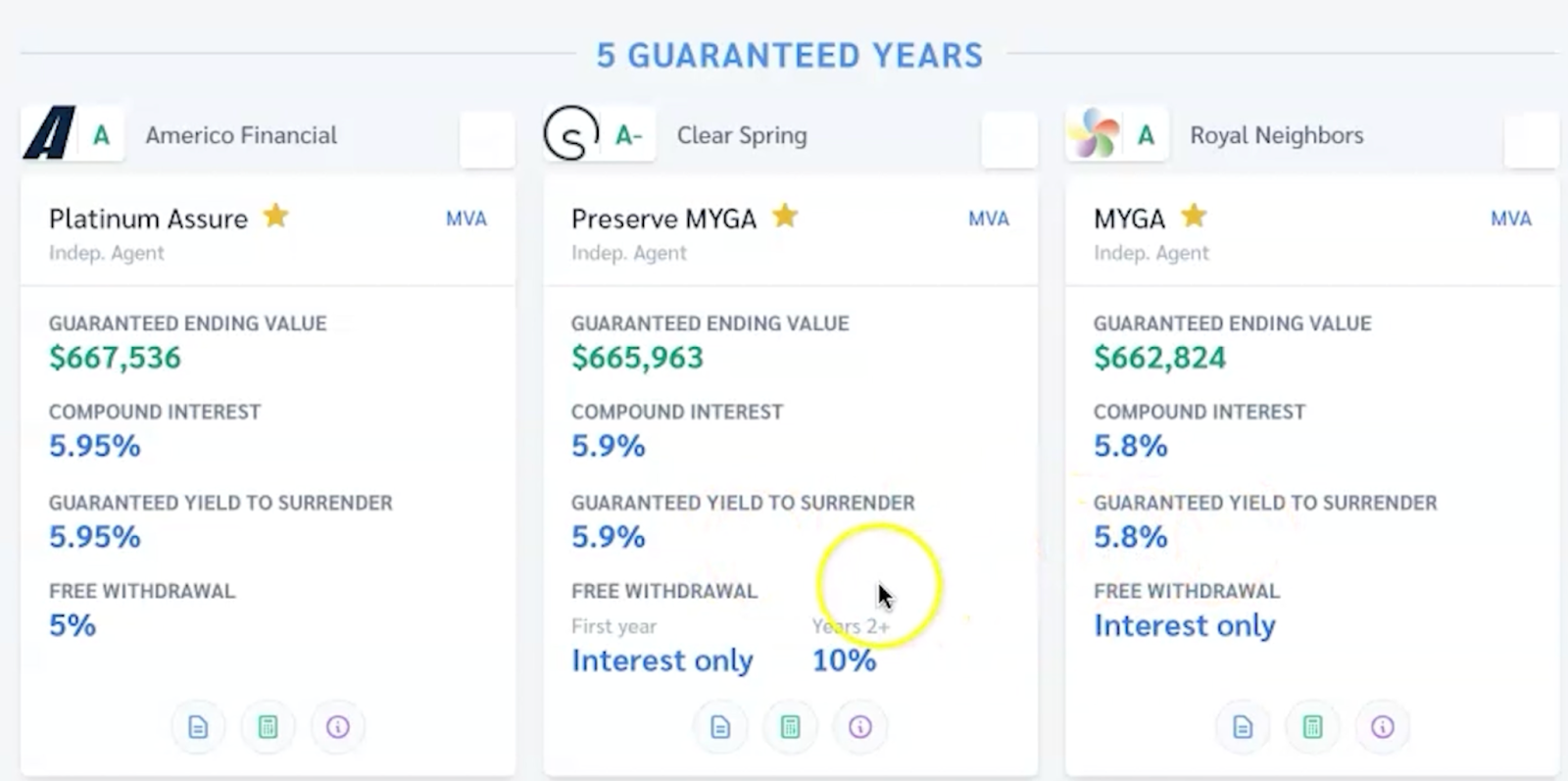

5 years at 5.8% to 5.95%:

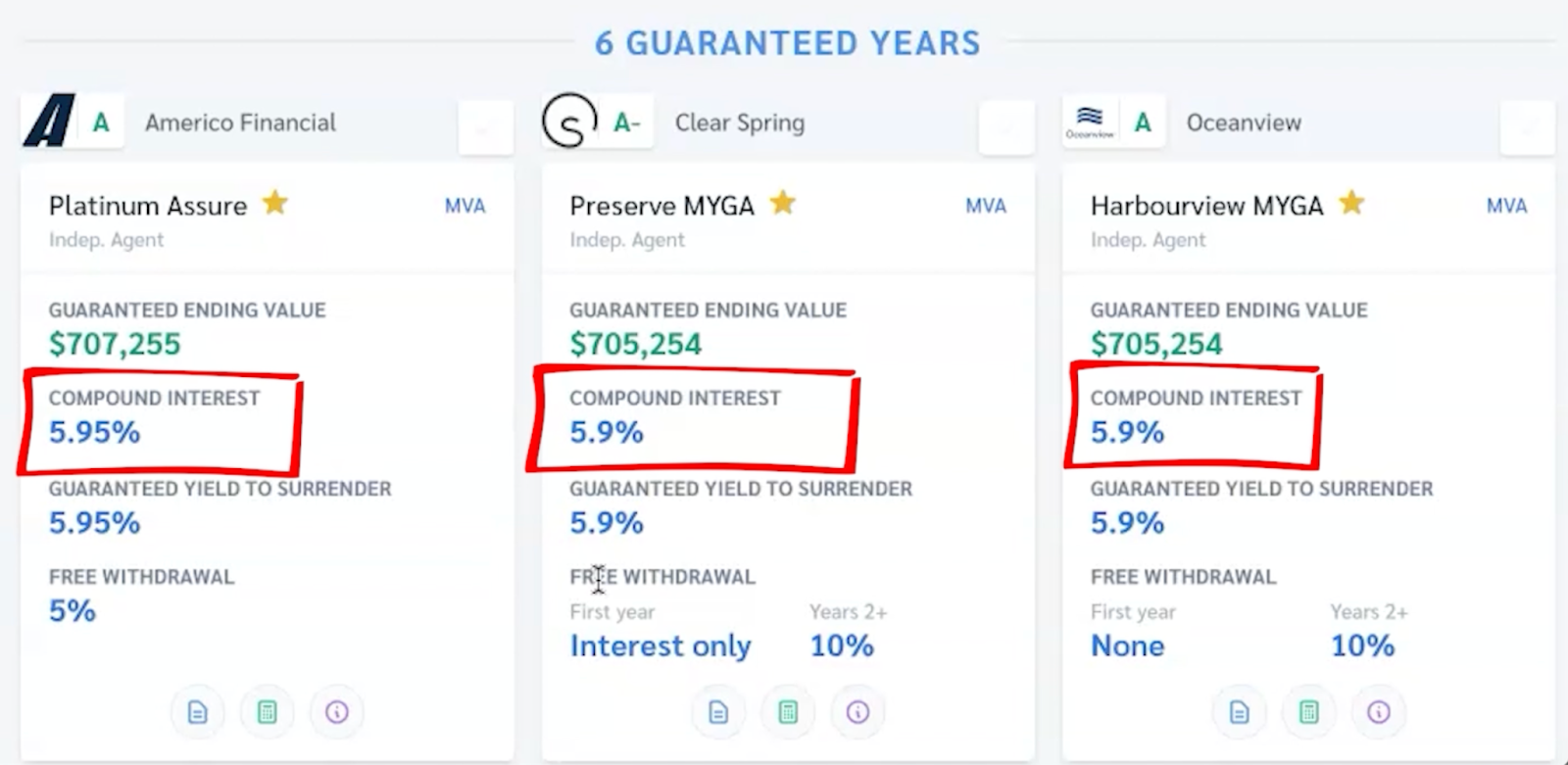

6 years at 5.9%:

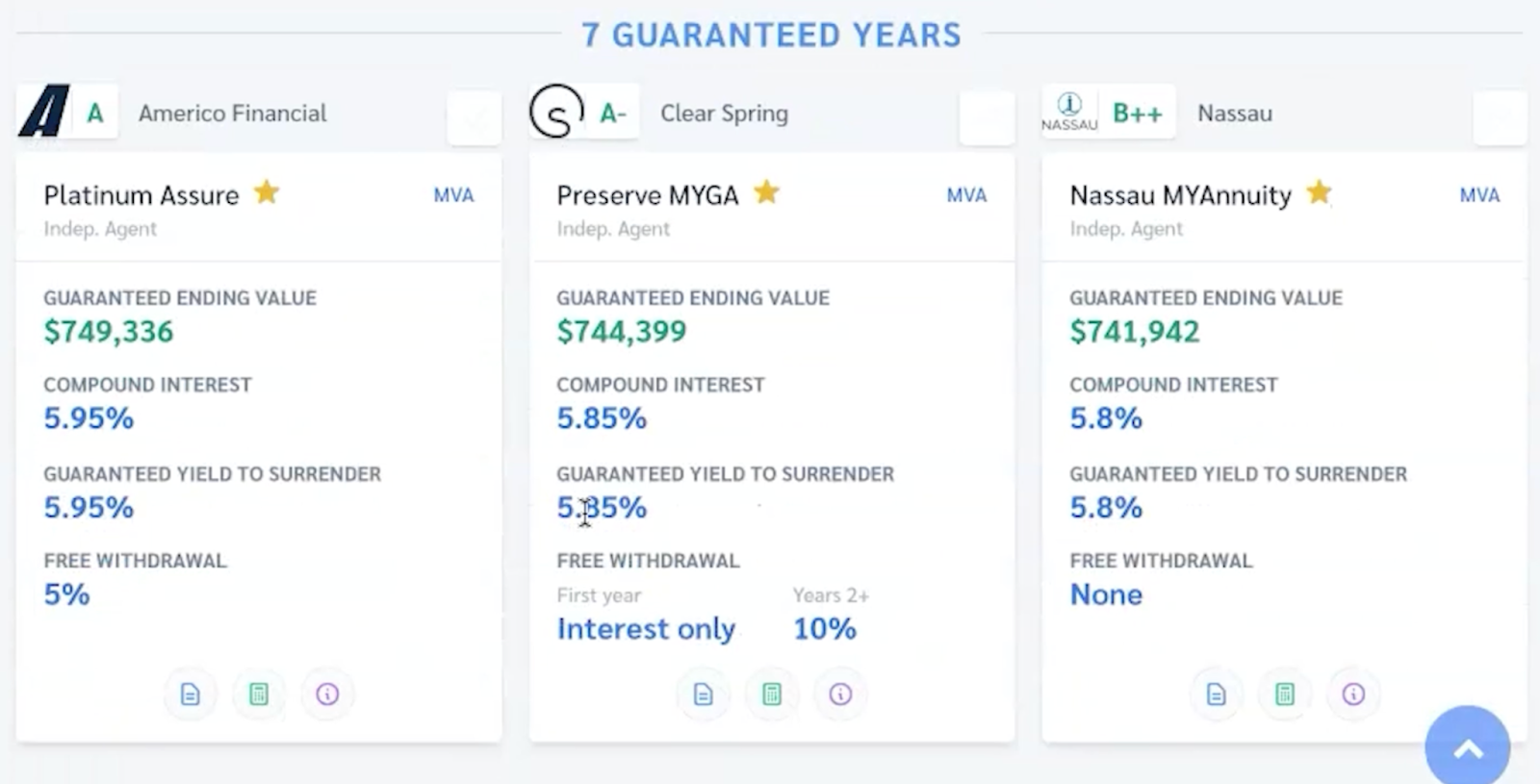

7 years at 5.8% to 5.95%:

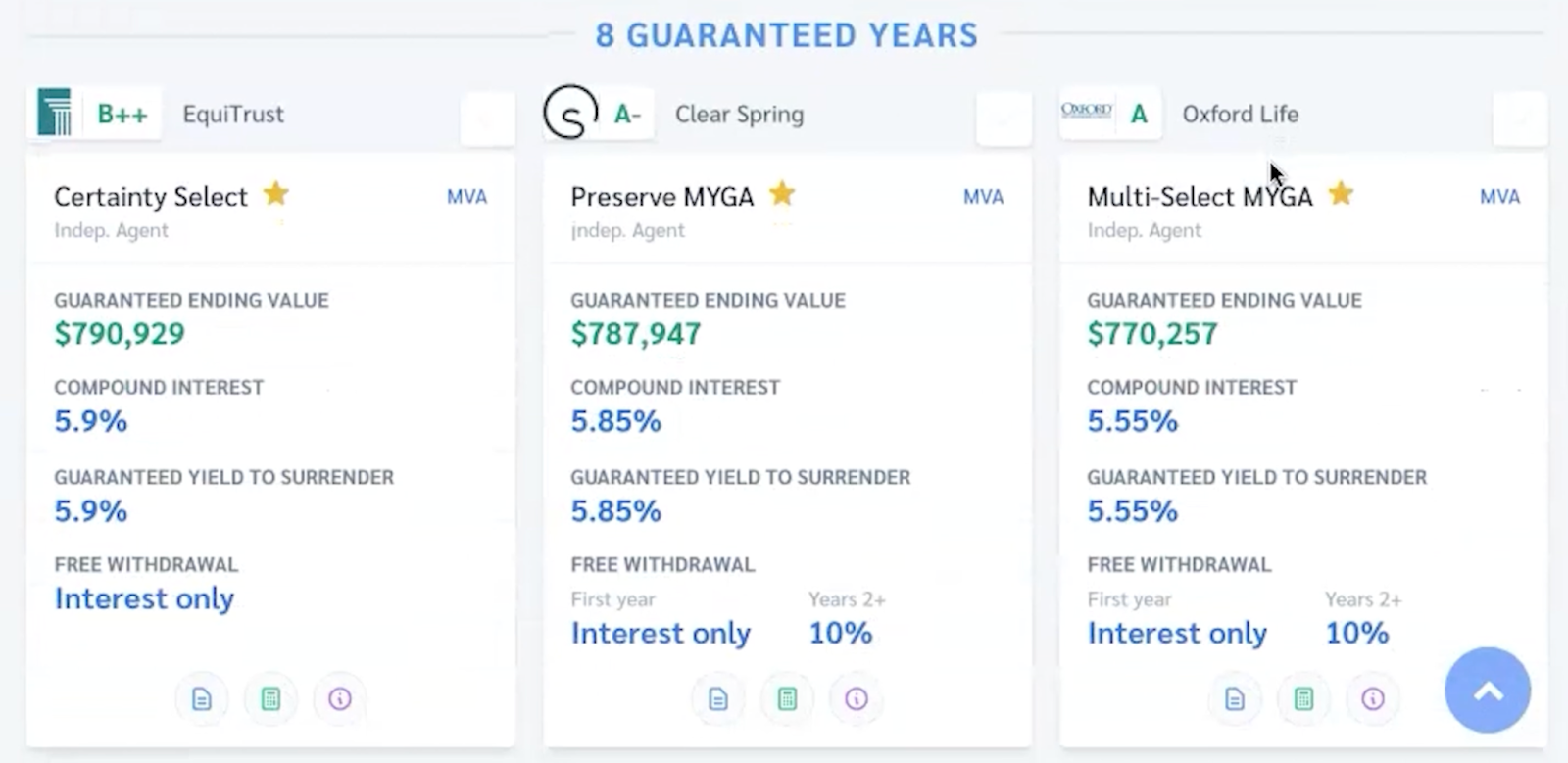

8 years at 5.55% to 5.9%

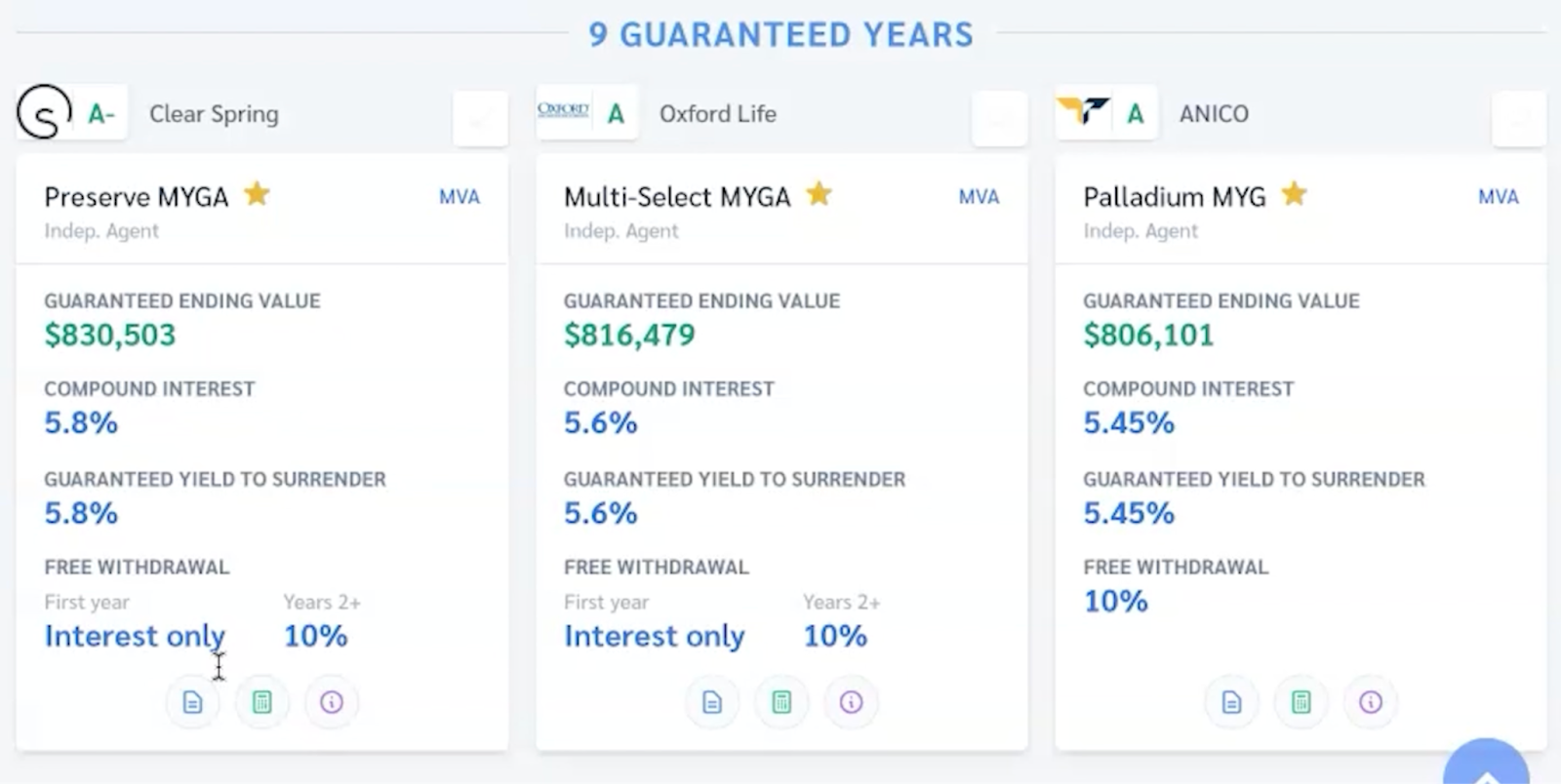

9 years at 5.45% to 5.8%:

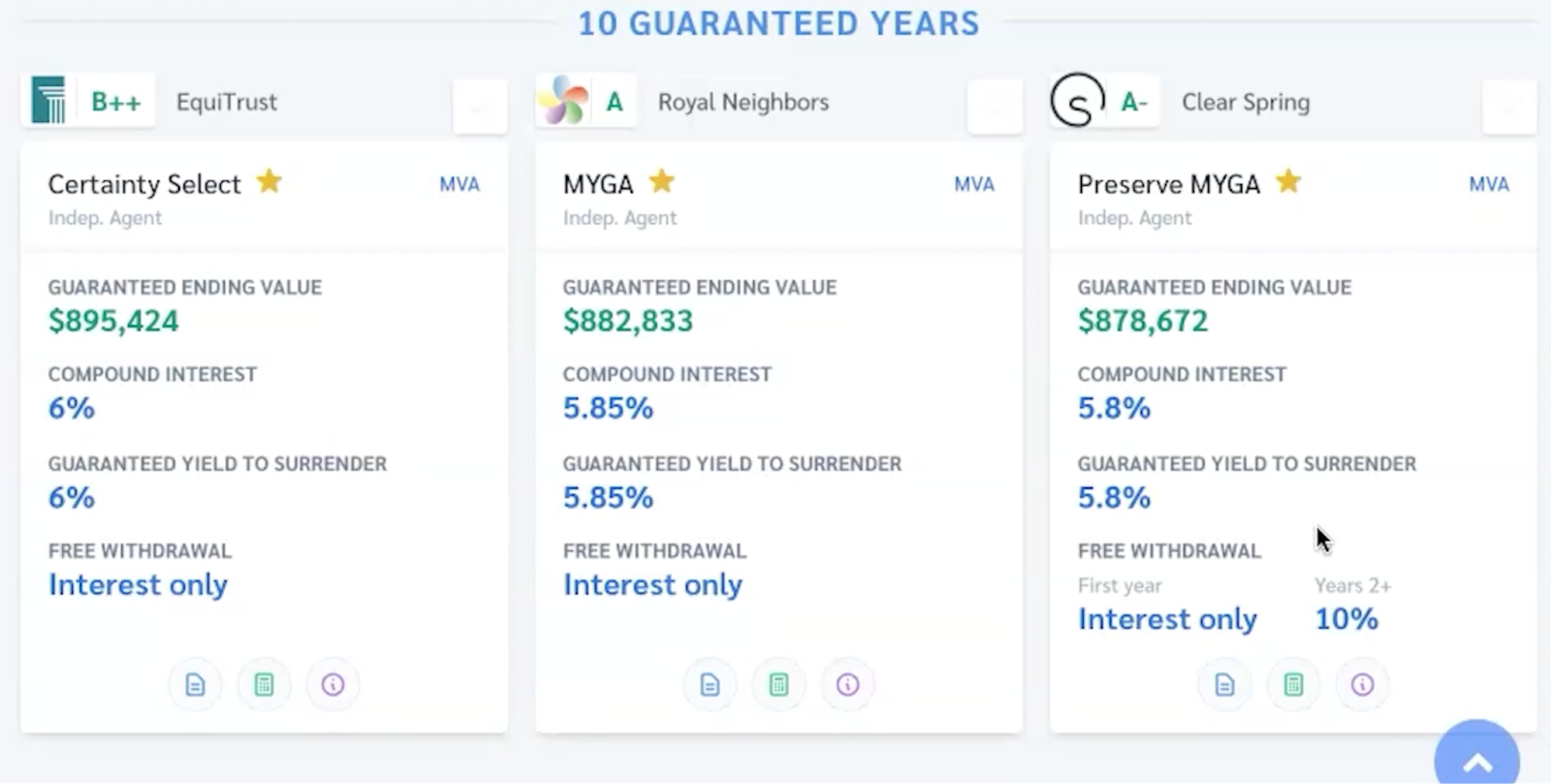

10 years at 5.8% to 6%:

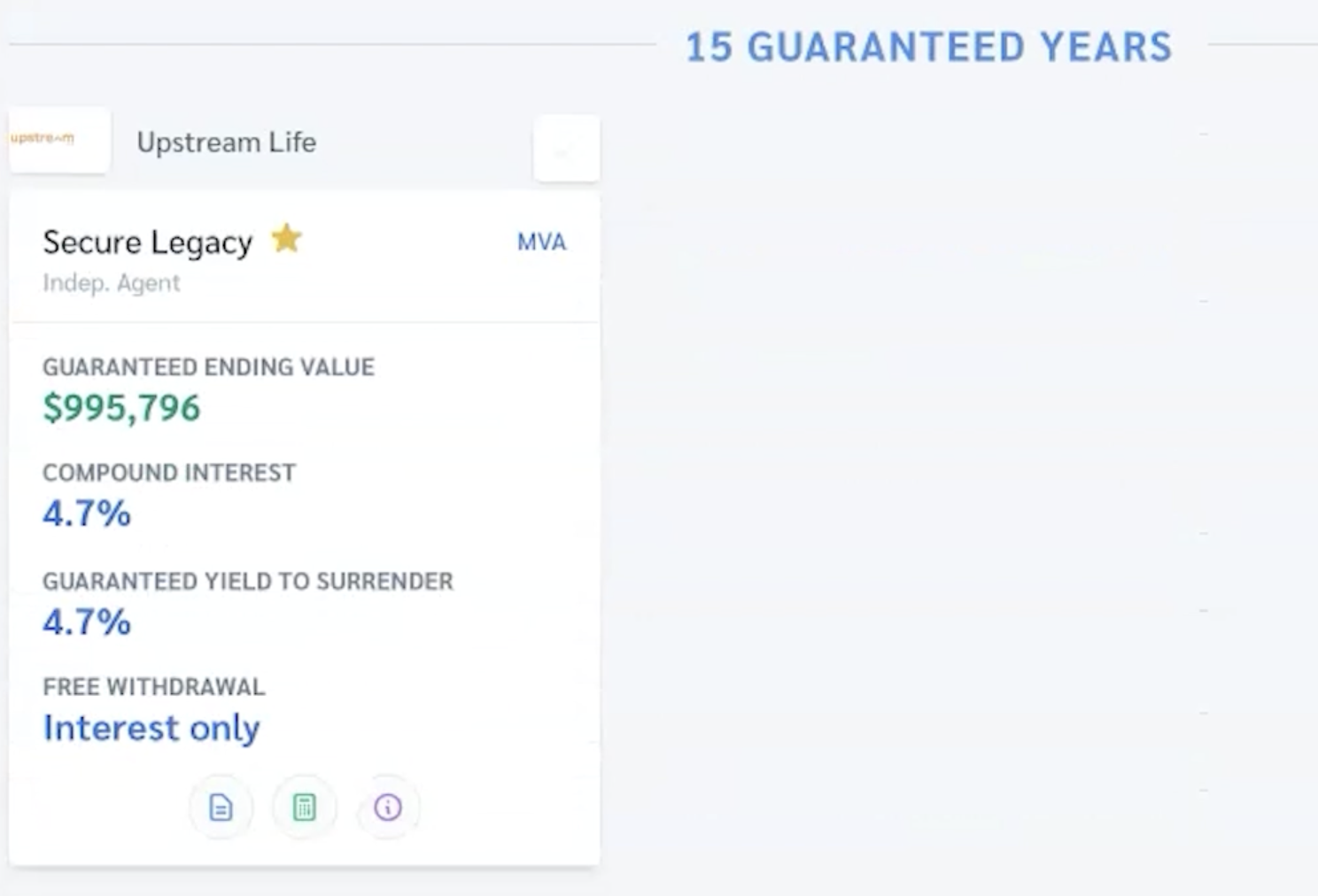

15 years at 4.7%:

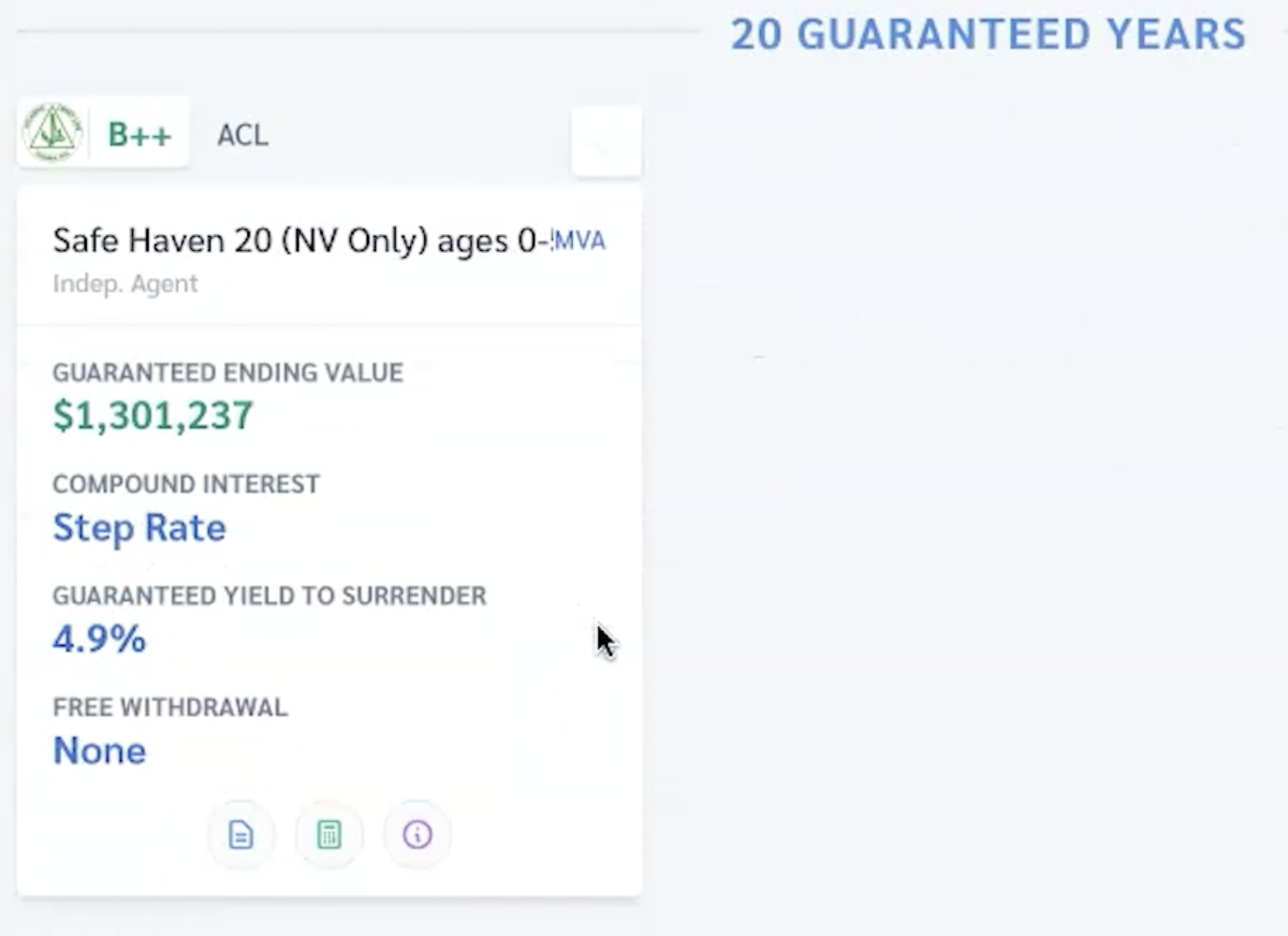

And finally 20 years at 4.9%:

It’s worth noting that fixed annuity rates are considered the best in the market. These rates are often higher than CDs due to extended investment periods and the ability of the insurance company to invest in a wider array of opportunities.

Navigating Short-Term Annuity Options: 1-4 Years

For those interested in short-term investment opportunities, consider Clear Spring’s 1-year fixed annuity, boasting a competitive 4.15% interest rate. This option offers the benefit of tax deferral, which allows the interest earned on your annuity to grow tax-free until you choose to make a withdrawal.

Due to their lower risk and greater flexibility, short-term annuities serve as a viable option for investors hesitant to commit their money for longer durations. However, they might offer lower returns compared to longer-term annuities.

Mid-Term Stability: 5-10 Year Fixed Annuities

Mid-term fixed annuities, particularly those with terms from 5 to 10 years, serve as an optimum choice for investors seeking to balance risk and return. They provide a host of advantages such as:

- Protection of the premium

- A guaranteed minimum interest rate

- Tax-deferred earnings

- A predictable income stream

- A death benefit.

Top options for 5-10 year fixed annuities include:

- Equitrust with Certainty Select rates ranging from 1.00% to 3.00%

- Royal Neighbors with their minimum guaranteed rates

- Clear Spring’s Preserve 5 with a rate of 5.55%

- Atlantic Coast Life offers competitive rates as well.

The Long Haul: Understanding 15-20 Year Annuities

Investors comfortable with long-term investments can opt for annuities with terms ranging from 15 to 20 years. These annuities, also referred to as fixed period or period certain annuities, provide the option to select a specific duration for receiving annuity payments.

While long-term annuities can offer higher returns due to their extended terms, they also come with potential risks, including:

- Complexity

- Limited upside potential

- Potential tax implications

- Accumulating expenses

- Erosion of purchasing power due to inflation

Fixed Annuity Interest Rate Trends

Various factors such as economic conditions, monetary policy, and market fluctuations can influence the variability of fixed annuity interest rates.

However, fixed annuities are recognized for their ability to offer stable and predictable income streams during retirement.

These annuities usually have a locked-in interest rate, providing a degree of predictability for returns.

Fixed Annuities vs. Other Investment Vehicles

Having established an understanding of fixed annuities, it’s worth exploring how they compare to other investment options. The main distinguishing factor of fixed annuities is the predictability and security they offer.

Variable annuities, for instance, link returns to the performance of the mutual funds in which they are invested. On the other hand, bank CDs, while similar to fixed annuities, often offer lower returns and lack the tax advantages associated with fixed annuities.

Why Choose Fixed Over Variable Annuities

Due to their predictable returns and lower risk profile, fixed annuities hold an evident advantage over variable annuities. They provide investors with a guaranteed interest rate, which ensures a consistent and predictable income stream for retirement.

In contrast, variable annuities present higher levels of risk as they are susceptible to market risk and may involve investment positions in volatile financial securities. Therefore, if you’re a conservative investor prioritizing stability and safety, fixed annuities would be a more suitable choice.

Fixed Annuities and Tax Advantages

Tax-deferred growth stands out as a key benefit of fixed annuities, which can also be referred to as a deferred annuity. This means the interest earned on your annuity remains untaxed until you choose to make a withdrawal. This allows your earnings to grow more rapidly than they would in a taxable investment.

However, it’s important to note that withdrawals from fixed annuities are subject to ordinary income tax. Early withdrawals before age 59½ may also incur a 10% penalty tax. It’s therefore crucial to plan your withdrawals wisely to ensure you maximize the tax benefits offered by fixed annuities.

Maximizing Growth with Multi-Year Guaranteed Annuities (MYGAs)

For those in pursuit of stability and predictability, Multi-Year Guaranteed Annuities (MYGAs) present an additional investment option. These are fixed deferred annuities that provide guaranteed returns over a specified duration, usually between 3 to 10 years.

While these annuities offer the benefit of tax-deferred growth and protection against market fluctuations, they also come with restricted liquidity. Early withdrawal before the end of the investment period may result in penalties.

The Appeal of Guaranteed Returns

Guaranteed returns serve as a major attraction for investors considering MYGAs. After depositing a lump sum of cash, you receive guaranteed interest rates for a specific period of time, akin to a certificate of deposit (CD) with a fixed interest rate.

MYGAs offer a fixed guaranteed return, making them suitable for conservative investors prioritizing stability and safety. This assurance of a guaranteed rate for a set term ensures investors a dependable and foreseeable return.

Selecting the Right Term for Your MYGA

To align your investment with your financial objectives and risk tolerance, it is vital to choose the appropriate term for your MYGA.

The term length of a MYGA influences the account’s growth potential by committing the funds for extended periods, providing more time for potential accumulation and growth.

However, it’s important to keep in mind that MYGA interest rates may fluctuate during the contract’s term, potentially impacting the growth of the account value. Hence, it’s crucial to consider your financial goals and risk tolerance while selecting the term for your MYGA.

Partnering with Top-Rated Insurance Companies

Selecting the right issuing insurance company is equally as important as the annuity itself for your fixed annuity investment. Partnering with top-rated insurance companies ensures safety, reliability, and competitive fixed annuity rates.

Insurance companies are rated by agencies such as:

- AM Best

- COMDEX

- Moody’s

- Standard and Poor’s

- Fitch

- Weiss

These ratings are based on factors such as financial performance, investment management, claims paying ability, history of financial strength, and customer satisfaction among others.

Crafting Your Retirement Plan with Fixed Annuities

Crafting a retirement plan with fixed annuities requires careful consideration of key factors such as:

- The guaranteed interest rate

- Tax-deferred earnings

- Reliable income stream

- Your personal financial objectives

- Your risk tolerance

Fixed annuities can offer a steady income stream that complements Social Security and other retirement income, playing a pivotal role in your retirement plan.

Risk tolerance plays a significant role in the selection of a fixed annuity. Fixed annuities are well-suited for individuals who are averse to risk due to their guaranteed interest rate. Those with lower risk tolerance, such as individuals nearing retirement, may find the assurance of this guarantee particularly attractive.

Schedule a Consultation for Personalized Rate Projections

Scheduling a consultation with a financial professional is advisable to ensure your fixed annuity is in line with your financial goals.

Personalized rate projections can provide precise and tailored information regarding the potential interest rates and returns on your annuity, helping you make well-informed decisions.

The consultation should cover aspects such as:

- Your financial objectives

- Your current financial situation

- Your investment preferences

- Your risk tolerance

- Any specific financial concerns

This ensures your personalized rate projections, including any market value adjustment, are tailored to your individual financial circumstances.

Conclusion

In summary, fixed annuities can be a valuable component of your retirement plan, providing a guaranteed income stream and offering the potential for tax-deferred growth.

Whether you choose a short-term, mid-term, or long-term annuity, pairing it with a top-rated insurance company and seeking the advice of a financial professional can ensure your investment aligns with your financial goals and risk tolerance.

Have more questions about annuities? Click here to book a free consultation.

In this consultation, I can provide personalized advice and strategies, guiding you to make informed decisions about annuities and optimize your retirement planning.

I can also compare all the annuities so you can see which one is best regardless of the commissions associated with the annuity.

During the consultation, you will:

- Be able to compare different annuity options

- Learn how to grow & protect your wealth in retirement

- Get all of your questions about annuities answered

I look forward to speaking with you soon!