In this article, you’ll learn how to compare Multi-Year Guaranteed Annuity (MYGA) rates and find the best MYGA annuity for your situation.

Summary

- MYGA (Multi-Year Guaranteed Annuity) rates are fixed, shielded from market volatility, and influenced by prevailing interest rates, term length, and the insurer’s credit rating.

- When MYGA annuities are compared to other fixed annuities (such as fixed indexed annuities), they offer stable growth and are typically more predictable, making them suitable for those seeking consistent retirement savings growth.

- When choosing a MYGA annuity, consider factors such as the guarantee period, interest rate, insurer’s financial strength, and withdrawal options to ensure an informed decision and maximize returns.

Need help choosing the best type of annuity for your unique situation? Have questions about getting an annuity? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

Understanding MYGA Annuity Rates

A MYGA (Multi-Year Guaranteed Annuity) is a financial product that combines the security of an insurance company with the predictability of fixed interest rates.

Here’s how multi year guaranteed annuities work:

- Make an initial premium payment.

- The insurance company will apply a fixed interest rate to your account throughout your chosen term.

- This agreement guarantees the growth of your investment at a fixed rate, ensuring consistent appreciation throughout the annuity term.

Moreover, the growth within a MYGA annuity enjoys tax deferral, which allows for tax deferred growth. This means that the interest accumulates without immediate tax implications, allowing your assets to benefit from compound interest.

Taxes are only paid when you start receiving distributions, further enhancing the growth potential of your investment.

What influences MYGA rates, and how do they stack up against fixed indexed annuities?

Let’s find out…

Factors Affecting MYGA Rates

MYGA rates are influenced by several factors, one of which is the prevailing interest rate environment. MYGA annuities offer a guaranteed interest rate for a specific duration, meaning they are less exposed to market risk compared to other investment options.

Nonetheless, current interest rates directly affect them.

Another factor influencing MYGA rates is the term length. MYGAs, being a type of deferred annuity, typically provide higher yields for longer term lengths compared to shorter ones.

Additionally, the credit rating of the insurance company can also affect MYGA rates; companies with a lower credit rating may offer higher rates to attract customers.

How MYGA Rates Compare to Fixed Indexed Annuities

In the realm of fixed interest rates, MYGAs distinctly differ from fixed indexed annuities. MYGAs provide a consistent fixed rate for a predetermined period, ensuring stable growth throughout the specified term, free from any fluctuations in rates.

On the other hand, traditional fixed indexed annuities offer a minimum guaranteed rate along with a fluctuating current rate that can change based on market conditions.

Thus, if you’re seeking a predictable and stable growth option for your retirement savings, MYGA annuities may be the preferred choice.

Need help finding the best MYGA annuity rate? Watch this short video to see how I can help you do this (at no cost to you!)

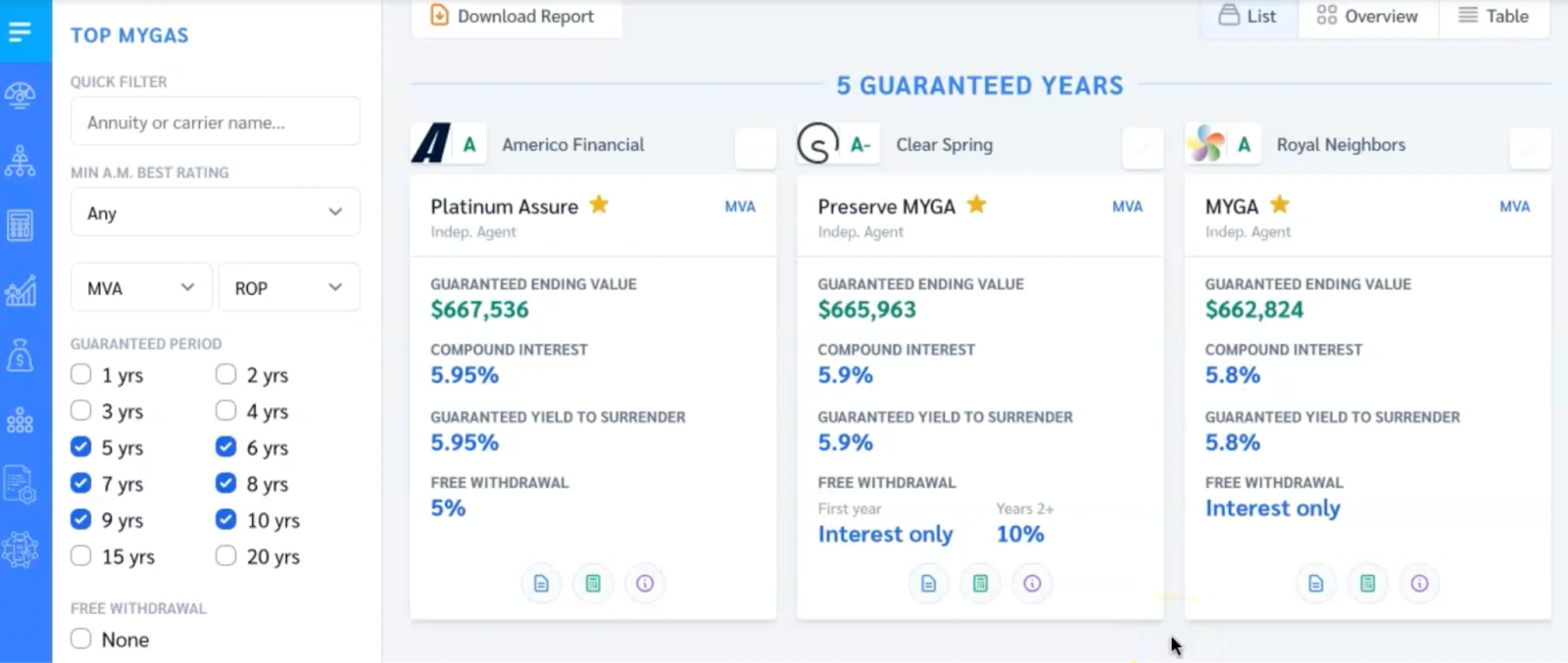

Top MYGA Annuity Providers and Their Rates

The MYGA marketplace features several prominent providers offering competitive rates.

As you can see, some of the top MYGA providers include:

- Americo Financial: currently offering the most competitive annuity rate at 5.95%

- Clear Spring: offering attractive fixed annuity rates in the 5 to 10 year range

- Royal Neighbors: also offering attractive fixed annuity rates in the 5 to 10 year range

However, these rates can change each month and can differ depending on how long you defer withdrawals. So it’s important to schedule a call to go through the latest and best rates specifically for your unique situation.

Before committing to invest, understanding the flexibility and withdrawal options these providers offer is vital. These factors can significantly impact your ability to access your funds and should, therefore, be considered carefully.

Need help finding the best MYGA annuity provider? Watch this short video to see how I can help you do this (at no cost to you!)

Comparing Flexibility and Withdrawal Options

Different MYGA providers offer varying levels of flexibility when it comes to withdrawals. Generally, MYGA annuities permit the withdrawal of a predetermined percentage of the accumulated funds during the annuity term without incurring penalties.

Certain contracts may also include provisions for emergency withdrawals.

Notably, MYGA annuities distinguish themselves from other fixed annuities by allowing for the withdrawal of the accumulated value at the conclusion of the annuity term without incurring surrender charges.

They often offer penalty-free withdrawal options, enabling annual withdrawals of up to 10% of the annuity’s value.

Evaluating MYGA Annuity Rates: What to Consider

When assessing MYGA rates, considering more than just potential returns is crucial. The financial stability of an insurer, while not directly impacting MYGA rates, is a crucial factor to consider, as it reflects the company’s claims paying ability and their ability to meet contractual obligations.

Another important aspect is customer service. The quality of an insurer’s customer service can greatly affect your experience as a policyholder. It ensures the provision of sufficient support and assistance in managing your retirement income, making it a key factor in your decision-making process.

Lastly, evaluating the annuity’s surrender charges is important. These are penalties imposed for premature withdrawal from a MYGA annuity before its maturity, usually enforced within the initial six to eight years.

Understanding these charges is key to assessing the comprehensive value and cost efficiency of the annuity.

Fixed Annuity vs. Fixed Indexed Annuity: Which is Right for You?

Your specific financial situation and goals should guide your decision between a fixed annuity and a fixed-indexed annuity.

A fixed indexed annuity is a tax-deferred, long-term savings vehicle. It aims to achieve higher growth potential than a fixed annuity by being linked to a stock market index, while maintaining lower risk and potential return compared to a variable annuity.

Both fixed annuities and fixed indexed annuities offer a secure approach to accumulating retirement funds in contrast to more unpredictable investments. They are designed to provide a consistent, lifelong monthly income, making them especially appealing to retirees in search of reliable cash flow.

Thus, the choice between the two will depend on your growth potential expectations and risk tolerance. If you’re seeking a predictable and stable return, a fixed annuity may be the better choice.

However, if you’re willing to take on a bit more risk for potentially higher returns, a fixed indexed annuity might be worth considering.

Need help comparing between fixed annuities and fixed indexed annuities? Watch this short video to see how I can help you do this (at no cost to you!)

Tips for Choosing the Best MYGA Annuity Rate

Doing your homework is crucial in finding the best MYGA rate. Conduct thorough research and gather the rates offered by leading providers. Online resources such as annuity.org can assist in finding current best guaranteed annuity rates across various companies.

When choosing a MYGA annuity, consider the following factors:

- Guarantee period length

- Interest rate offered

- Financial strength and reputation of the insurance company

- Withdrawal provisions, including features such as market value adjustment (MVA) and return of premium (ROP) that can affect fund access and the annuity’s flexibility.

Thoroughly reviewing these factors will help you make an informed decision.

Strategies to Maximize Your MYGA Annuity Returns

After selecting a MYGA annuity, the subsequent step is to put in place strategies for maximizing your returns. One such strategy is to consider longer-term MYGAs. These typically lead to higher yields compared to similar bank CDs, making them an attractive option for those looking for higher rates.

Another effective strategy is to diversify your portfolio. By spreading your investments across different types of assets, you can potentially enhance your MYGA annuity returns by mitigating volatility and potentially boosting long-term returns.

Monitoring interest rate trends can also be beneficial for maximizing MYGA annuity returns. A rise in interest rates can result in increased bond yields for insurance companies, ultimately benefiting annuity holders.

Navigating the MYGA Annuity Marketplace

While navigating the MYGA annuity marketplace might seem daunting, with proper guidance from an advisor, it becomes manageable.

They can provide assistance in navigating the marketplace, offering guidance on:

- investment amounts

- comparison shopping

- addressing inquiries

- facilitating the application process

Staying abreast of marketplace developments is also crucial. Here are some key points to consider:

- MYGA annuity rates undergo daily changes and may exhibit slight variations across different carriers.

- Economic and financial market conditions can significantly impact MYGA annuity rates.

- In a declining interest rate environment, MYGAs may present lower risks in comparison to other fixed annuities.

To learn how I can help you compare the best MYGA annuity rates currently available, watch this short video.

How to Purchase a MYGA Annuity

To purchase a MYGA annuity, you first need to:

- Enter into a contract with an insurance company. This may involve making a single premium payment or periodic payments.

- Submit a completed application kit provided by the issuing insurance company.

- Before finalizing your purchase, it’s advisable to have a discussion with your trusted advisor or insurance agent about the specific type of annuity, the related expenses, and the potential trade-offs of your decision.

Lastly, before finalizing your purchase, comparing MYGA annuity offers is necessary. You can do this by evaluating their guaranteed returns, interest structure, and payout options.

Conclusion

MYGA annuities offer a secure and predictable option for growing your retirement savings.

They provide a fixed interest rate for a specified term, offering competitive rates compared to bank CDs, tax-deferred growth, and a selection of term lengths, with most competitive rates typically found in the 5 to 10-year range.

Whether you’re a seasoned investor or a newcomer to the world of retirement savings, understanding and effectively navigating the MYGA annuity marketplace can significantly enhance your financial security.

Have more questions about annuities? Click here to book a free consultation.

In this consultation, I can provide personalized advice and strategies, guiding you to make informed decisions about annuities and optimize your retirement planning.

I can also compare all the annuities so you can see which one is best regardless of the commissions associated with the annuity.

During the consultation, you will:

- Be able to compare different annuity options

- Learn how to grow & protect your wealth in retirement

- Get all of your questions about annuities answered

I look forward to speaking with you soon!