Is $1 million enough to retire right now? Inflation, healthcare, and lifestyle choices directly impact this vital question.

In this article, we’ll analyze whether $1 million is enough to retire, take a look at how much a $1 million annuity would earn in lifetime guaranteed income and let you be the judge.

Summary

- The adequacy of a $1 million retirement fund heavily depends on personal factors such as desired lifestyle, healthcare costs, inflation, and additional income streams like Social Security.

- Asset allocation, maximizing contributions to retirement accounts, and leveraging tax-advantaged accounts like Roth IRAs, Traditional IRAs, and HSAs are crucial strategies to maximize retirement savings.

- Proper estate planning and implementing tax-efficient withdrawal strategies are pivotal in preserving retirement funds and minimizing tax liabilities to protect one’s legacy for future generations.

Need help choosing the best annuity for your unique situation? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!).

Strategies for Generating Lifetime Retirement Income

To generate a steady income stream after retirement, annuities can be an effective financial product. Designed to provide fixed payments for life or a specified period, they can offer a viable strategy for those with a substantial retirement fund, and are easy to calculate.

First, let’s look at the annual income a $1 million annuity will provide so you can decide whether that’s enough to retire.

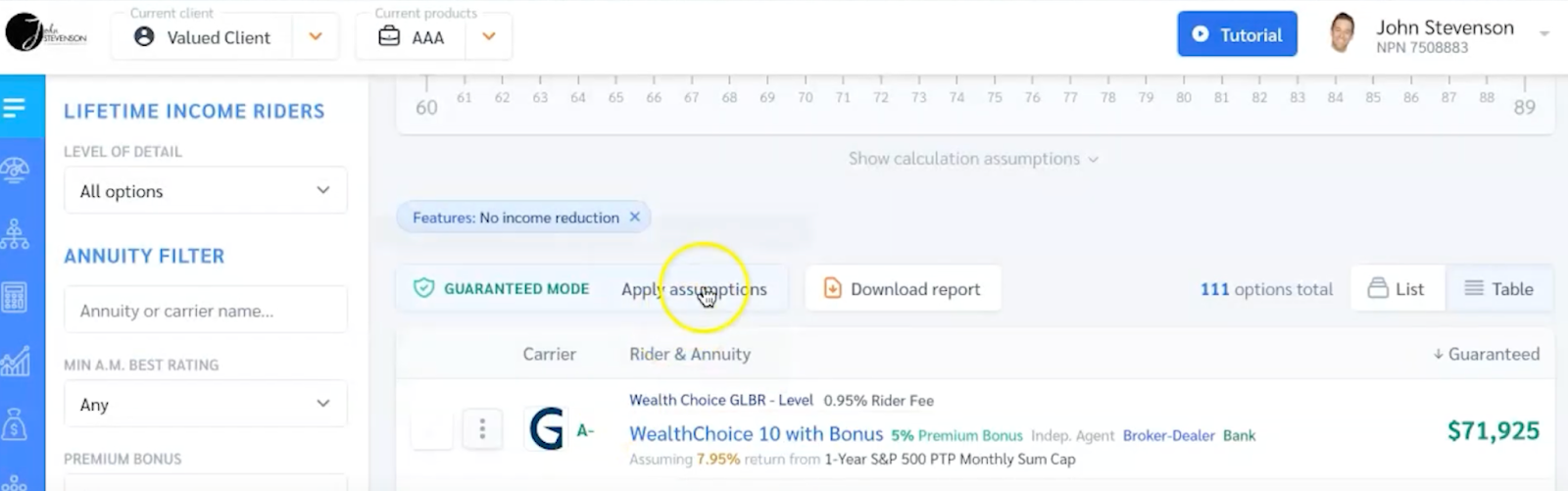

While annuities valued at $300,000 might pay out up to $36,000 annually, and a $500,000 annuity could pay anywhere between $34,800 and $55,200, an immediate annuity valued at $1 million could potentially yield a yearly income of $71,925, which is roughly $6,000 per month, as seen here:

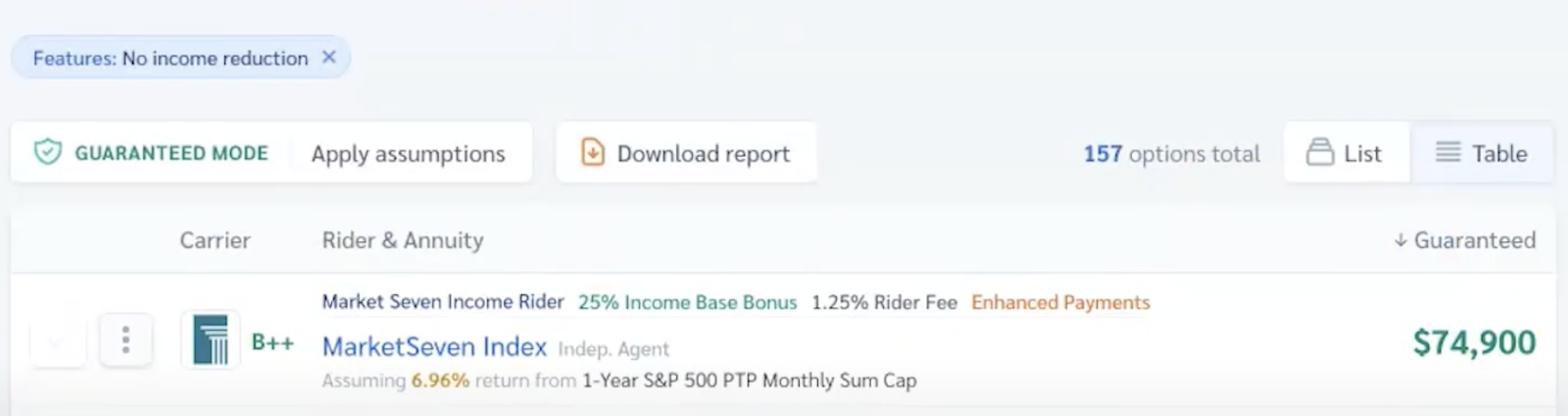

If you waited 1 year, this jumps up to $74,900 each year, as seen here:

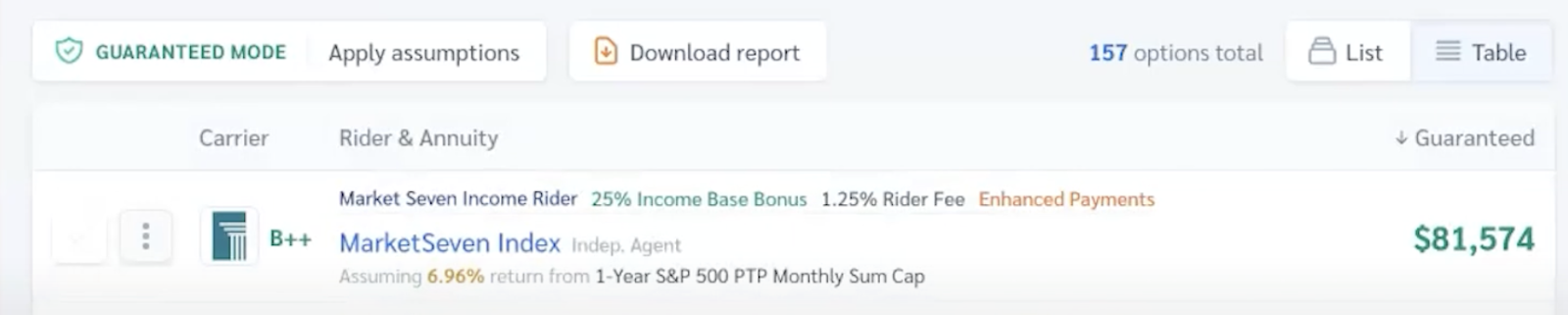

If you wait 2 years, this jumps up to $81,574, as seen here:

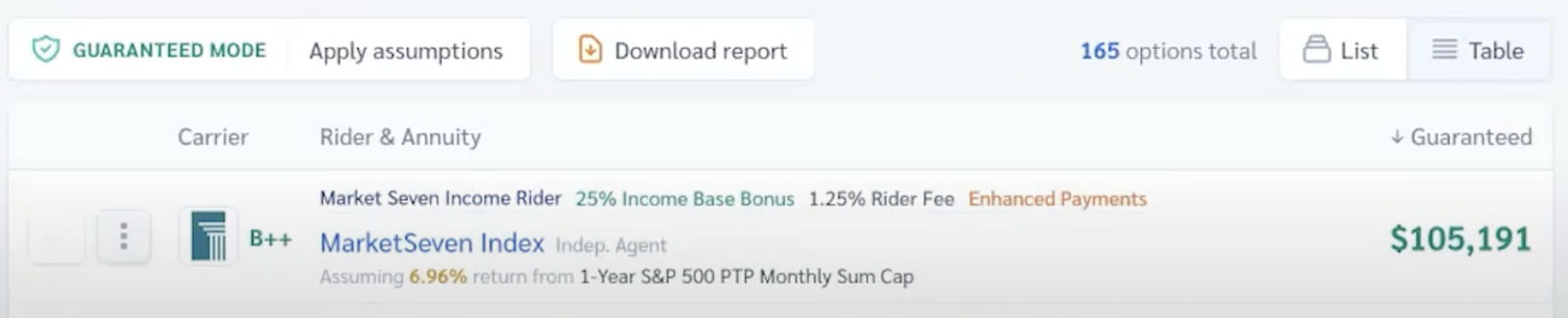

If you wait until age 65 because you have Medicare and you’re going to keep working until then, the yearly payout increases to $105,192, as seen here:

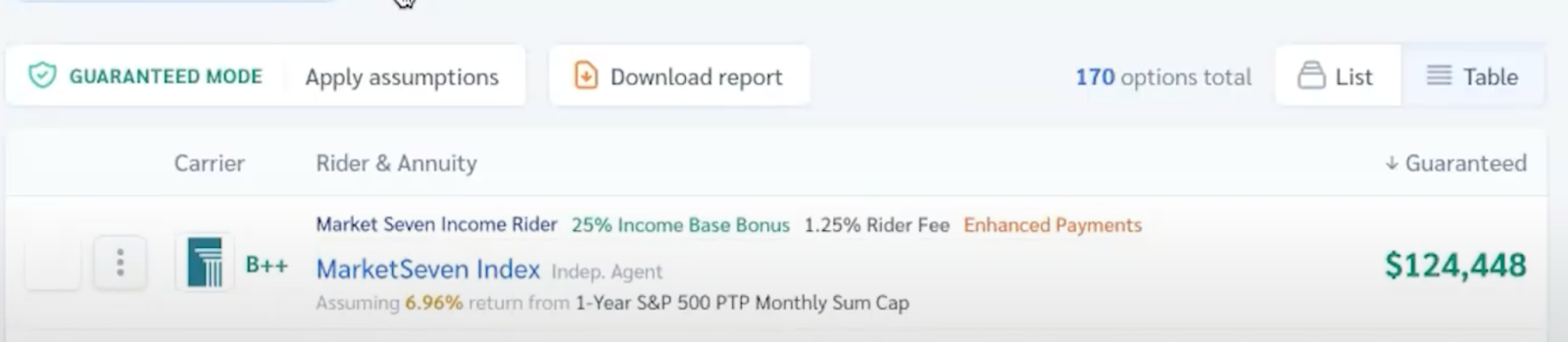

If you wait until age 67, the payout increases to $124,448:

As you can see, the longer you wait, the higher your payout can be.

The above data is based on a hypothetical scenario of a married couple, aged 60, living in Florida. The payouts will change depending on your age. To find out how much you could earn, click here to schedule a call, and I’ll be happy to show you what’s available.

Guaranteed Period Income Annuities can provide income for a fixed period and can be useful for bridging financial gaps until other retirement income sources begin.

Immediate Annuity Options for Instant Income

Among the various types of annuities, immediate annuities offer income soon after purchase. A Guaranteed Lifetime Income Annuity provides consistent payments for the rest of an individual’s life starting immediately after purchase.

Lifetime Mutual Income Annuities offer steady lifetime payments with the potential for additional dividend payments.

Companies like Gilico offer the highest immediate payout for annuities, with the highest annuity payout available being 72,000 USD annually or 6,000 USD monthly.

Top Deferred Annuity Choices for Future Income

Alternatively, deferred income annuities are designed for growing funds now to secure higher payouts in the future.

They offer a variety of guarantee periods, such as three, five, or seven years, and provide options for renewing into new guarantee periods or beginning annuity payments without surrender charges after the initial period.

Companies like Equitrust offer a higher payout if the annuity is deferred for a year. If the annuity is deferred until the individual is 65 or 67, Equitrust offers an annual payout of $105,000 USD or $124,000 USD, respectively.

Evaluating the Adequacy of a Million Dollars for Retirement

While $1 million is frequently cited as a target amount for retirement savings, its adequacy is contingent on individual variables. To ensure a comfortable retirement, it is often advised to strive to save as much as possible rather than focus on a specific figure.

Theoretical evaluations suggest that $1 million could suffice, considering life expectancy and market performance factors. However, the actual amount required is influenced by variables like retirement lifestyle, market conditions, and the impact of inflation on savings.

Accurately estimating future spending needs is crucial, encompassing everyday expenses and potential unexpected costs such as healthcare or emergencies.

Furthermore, establishing a clear timeline for retirement allows for proper financial preparation and maximizes investment potential, underpinning a tailored retirement strategy that considers future performance.

Understanding Your Retirement Lifestyle Goals

Defining your desired retirement lifestyle goals is a pivotal step in planning your financial needs for retirement. The amount needed to retire comfortably hinges on the lifestyle you hope to maintain during your golden years. Here are some examples:

- A modest lifestyle will require less savings

- A comfortable lifestyle will require average savings

- A luxurious retirement will likely demand more than average savings

Therefore, assessing whether $1 million is sufficient for retirement significantly depends on your specific retirement lifestyle goals.

The Role of Inflation in Eroding Your Nest Egg

Inflation is a key player in retirement planning, with its subtle yet steady erosion of your purchasing power over time.

This is particularly apparent in healthcare, where retiree costs have been rising at about one-and-a-half to two times the rate of general inflation, posing a specific challenge for retirement planning.

Consequently, due to inflation, annual healthcare costs for a healthy 65-year-old couple could increase by nearly 6% each year in retirement.

Retirement Income Streams Beyond Savings

Beyond retirement savings, alternative income streams such as Social Security and part-time work are essential in supplementing retirement funds.

Social Security income is a vital supplemental income stream, complementing the approximately $72,000 per year that can be sustained from a $1 million immediate annuity during retirement years.

Additionally, part-time work represents another source of income for retirees seeking to supplement their retirement funds further.

Maximizing Your Retirement Account’s Potential

When it comes to maximizing the potential of your retirement account, there are a few key strategies to consider:

- Make the most of your contributions, especially by leveraging any catch-up contributions available for those over 50.

- Invest in a 401(k) with pre-tax dollars.

- Use a Health Savings Account for tax-advantaged growth of funds earmarked for healthcare costs.

These strategies are essential for maximizing retirement savings.

Starting retirement contributions early in your career enables the power of compounding, which is heightened by participating in employer 401(k) match programs.

Adjusting investment aggressiveness and managing the risk-reward trade-off in retirement plans are also important considerations that vary according to individual career stages and retirement goals.

Unique retirement plan options, such as Solo 401(k)s, SEP IRAs, and SIMPLE IRAs, can be tailored to fit the specific financial and retirement objectives of self-employed individuals.

Asset Allocation for Sustained Growth

A diversified portfolio with a mix of investments can help manage risk and aim for sustained growth over time. Here are some key points to consider:

- Include a mix of stocks, bonds, and other investments in your portfolio.

- Keeping an allocation to stocks in the early years of retirement can help counteract the risk of depleting retirement savings too quickly.

- Regularly review and rebalance your portfolio to align with your investment goals and risk tolerance.

By balancing your retirement portfolios with stocks, bonds, and cash investments, you can produce a steady income stream while seeking growth and preserving capital.

Making the Most of Roth IRAs and Traditional IRAs

Another strategy to maximize your retirement savings involves taking advantage of Roth IRAs and Traditional IRAs. These types of retirement accounts offer unique tax benefits conducive to financial security in retirement.

Roth IRAs allow for tax-free growth and tax-free withdrawals after age 59½, which benefits those expecting to be in a higher tax bracket in retirement.

On the other hand, Traditional IRAs offer the advantage of tax-deferred growth, where contributions may be tax-deductible, and withdrawals are taxed as income after age 59½.

Tailoring Your Investment Advisory Approach

As you plan for retirement, customizing your investment strategy is essential.

Constructing a tailored investment strategy for retirement necessitates a comprehensive financial evaluation that should include:

- Tax analysis

- Portfolio review

- Investment management

- Retirement planning

- Budget creation

- Insurance analysis

- Estate planning

- College funding

- Charitable giving

It’s also crucial to strike an optimal balance between risk and return, fitting individual age and retirement timeline, supported by diversification to mitigate potential risks.

Professional guidance in financial planning is critical for effectively navigating the intricacies of tax laws and retirement planning, which can help optimize the tax efficiency of retirement savings.

High Net Worth Individuals vs. Average Savers

The investment strategies for high-net-worth individuals and average savers differ significantly. For high-net-worth individuals, it is important to:

- Seek advisors with expertise in managing complex assets

- Look for advisors who act as fiduciaries to prioritize clients’ best interests

- Utilize specialized advisory services for managing risk and optimizing tax outcomes

These strategies are necessary due to high-net-worth individuals’ complex wealth management needs.

Retirement planning for high-net-worth individuals may require distinct investment strategies and a deeper focus on tax considerations compared to average savers.

High-net-worth individuals are recommended to utilize strategies like maintaining an appropriate mix of asset classes, using tax-advantaged accounts, and utilizing long-term capital gains for tax efficiency.

Need consultation on your retirement situation? Schedule a call with a trusted advisor.

Practical Tips for Saving Money and Cutting Expenses

While having a substantial nest egg is crucial, managing expenses and saving money effectively can significantly enhance the longevity of your retirement savings. Utilizing a personal finance site can aid in this process.

Here are some practical ways to enhance savings:

- Track spending patterns and understand where you spend money

- Create a detailed budget to pinpoint unnecessary expenses

- Develop a plan to reduce expenses

Paying off high-interest debts, such as credit card balances, can significantly reduce the amount of interest paid, liberating funds for retirement contributions.

Reducing financial strain from debt can contribute to a more secure and stable retirement by allowing more money to be diverted into savings.

Frugal Living Without Sacrificing Quality of Life

Embracing frugal living strategies can significantly contribute to your financial stability during retirement. Here are some ways to practice frugal living:

- Create a budget to manage spending and identify opportunities to increase retirement savings.

- Choose an appropriate living situation, like downsizing or relocating, to reduce housing costs.

- Reduce transportation costs by selling a second vehicle or choosing a more fuel-efficient option.

These frugal living strategies can lead to substantial savings and help you achieve financial stability in retirement.

Eating at home, planning meals, and shopping at low-cost stores helps maintain a frugal diet without sacrificing nutrition or enjoyment.

Adopting frugal lifestyles, such as opting for cost-effective alternatives, using discounts, and prioritizing spending on experiences over material possessions, can contribute to wise spending without compromising the quality of life.

Taking Advantage of Retail Investments

In addition to saving, retail investments can provide opportunities for additional income and financial growth. Retail investors have the autonomy to tailor their investment portfolios, allowing them to engage with and direct their investments personally.

Smaller investments by retail investors can tap into opportunities with small companies, possibly benefiting from the small firm effect where these companies can realize higher growth rates than larger firms.

Planning Ahead: Estate Planning and Tax Efficiency

Estate planning and tax efficiency play pivotal roles in retirement planning, ensuring the protection of one’s legacy for the next generation.

Proper estate planning is pivotal in effectively managing the transfer of assets to beneficiaries, which is a key aspect of preserving one’s wealth for retirement and beyond.

Considering tax implications during the estate planning process is crucial to ensure that wealth is preserved and passed on according to one’s wishes without unnecessary tax burdens.

Strategies for Minimizing Taxes on Retirement Income

To maximize wealth preservation and minimize tax liabilities on retirement income, various strategies can be employed. Some of these strategies include:

- Utilizing Tax-Free Retirement Accounts (TFRAs) which are designed to grow wealth with fewer restrictions than traditional retirement accounts

- Evaluating the tax implications of retirement investment options

- Implementing strategic withdrawals to minimize tax liabilities

By implementing these strategies, individuals can potentially achieve significant tax savings on their retirement income.

Roth IRA conversions and careful management of required minimum distributions (RMDs) are key strategies for minimizing tax liabilities on retirement income.

Health savings accounts offer tax deductions for contributions and tax-free withdrawals for medical expenses, aiding in tax efficiency for retirees.

Conclusion

The adequacy of $1 million for retirement in 2024 is determined by many factors. These range from your lifestyle goals to the impact of inflation, the potential for additional income streams, and the efficiency of your retirement planning strategies.

Maximizing your retirement account’s potential, generating lifetime retirement income, tailoring your investment advisory approach, saving money, cutting expenses, and planning ahead with estate planning and tax efficiency all contribute to a comfortable and financially secure retirement.

Booking a call with an annuity expert can provide personalized guidance on annuity strategies and help you make informed decisions about your retirement income.

I can help you:

- Determine the best solution for your unique circumstances

- Navigate and make crucial decisions during your financial journey

- Find the best annuities for your unique situation

By clicking here to schedule a call, I can take a look at how much a $1 million annuity could pay you each month in guaranteed lifetime income and help you assess whether this would be enough for you to have a comfortable retirement.