Are you wondering how much money you should invest in an index annuity? The answer depends primarily on how much income you need (or would like) in retirement.

This article provides some helpful tips on what you need to consider when investing in an index annuity to help you determine what would be the right investment amount for you.

Summary

- Investment in an index annuity should be tailored to individual financial goals. Considerations should include immediate or deferred income needs and the impact of income riders like Guaranteed Lifetime Withdrawal Benefits (GLWBs), which may require a higher initial investment.

- Time plays a vital role in index annuities, impacting investment strategy and compounding interest benefits, with long-term horizons typically leading to more aggressive investment choices and potentially higher returns.

- Understanding the fees, costs, and performance factors of index annuities is crucial, including insurance company charges, surrender periods, participation rates, and caps on earnings, all of which influence the potential growth of the investment.

- Income annuities generally require higher minimum investments compared to other annuity types. It’s important to shop around to find a company that can accommodate your investment needs for income annuities.

Need help choosing the best index annuity for your unique situation? Have questions about getting an index annuity? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

Determining Your Index Annuity Investment

Investing in an index annuity requires careful consideration, as it should align with your individual financial goals and personal needs. The desire for retirement income and principal protection significantly influences the amount you invest in an index annuity.

Sounds simple, right?

However, the process involves more than just selecting an arbitrary figure.

You need to consider the funds needed to cover essential living expenses during retirement and weigh the potential growth against direct market investments. This delicate balance allows you to tailor your initial investment to your needs, maximizing the benefits of your index annuity.

Tailoring Your Initial Investment

The choice between immediate or deferred income plays a pivotal role in this tailoring process. So, what are these choices, and how do they affect your investment?

Immediate income provides funds right away, while deferring income up to 10 years can grow the retirement paycheck as the deferred annuity investment accumulates interest. Income annuities often require higher initial investments compared to other annuity types.

For those opting for joint income with a spouse, the tailoring process considers both parties and aims to provide a stable income stream in retirement.

But what happens when you add an income rider to the same income mix?

Impact of Income Riders on Investment Amount

An income rider, like a Guaranteed Lifetime Withdrawal Benefit (GLWB), adds another layer of complexity to your index annuity investment.

Attaching an income rider to your index annuity may require a higher initial investment compared to a standalone annuity. Similarly, income annuities generally come with substantially higher minimum investments, so it’s important to shop around to find a company that can accommodate your investment needs.

This adjustment is crucial to secure the same level of guaranteed lifetime income and significantly influences your overall strategy for securing retirement income. Now, how does this translate into concrete numbers? Let’s delve into investment benchmarks for desired annual income.

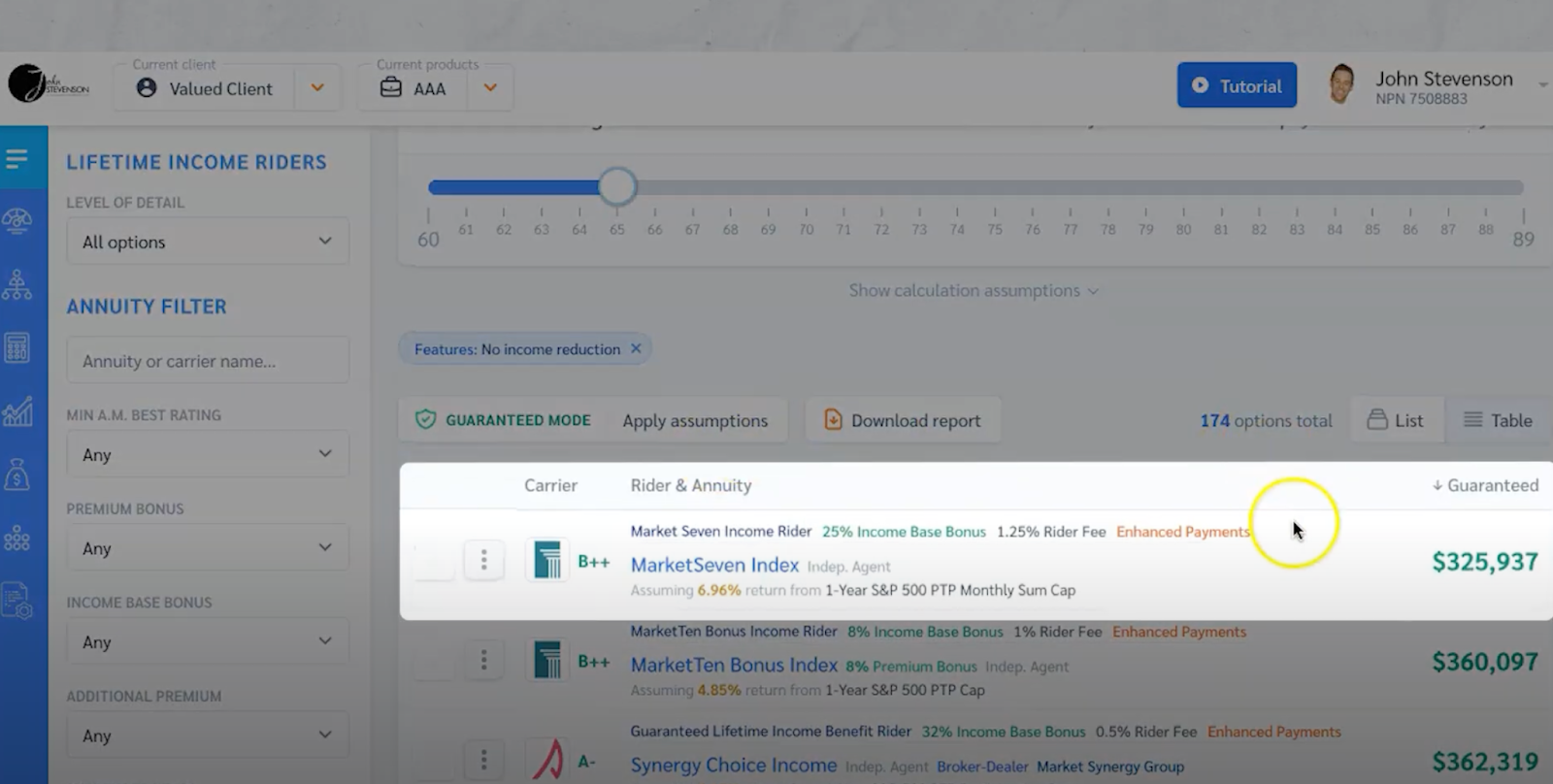

Example Scenario

Let’s look at an example index annuity for someone aged 65 who wants an immediate income. If someone in this scenario needs an additional $40,000 per year, an index annuity investment of $325,937 would be required, as seen here:

Of course, this number can vary depending on your age and other factors. So it’s always best to schedule a call with an annuity expert to see how much you need to invest in an index annuity to reach your income needs.

Now let’s explore the role of time in index annuity investments.

The Role of Time in Index Annuity Investments

Time is a significant factor in index annuity investments. The investment time horizon, or the planned duration of holding an investment, is crucial in determining the growth potential and income stream size in index annuities. But how does this work?

A longer investment horizon utilizes the benefits of compounding interest, significantly enhancing the growth of the annuity investment over time. With a long-term investment horizon, investors can choose more aggressive investment options, as they do not require immediate access to their funds.

Income annuities are often considered for long-term investment strategies due to their higher minimum investment requirements.

However, the assumed five-year sitting period before withdrawal is a specific time frame that influences the investment strategy and amount for an index annuity.

Let’s delve deeper into this by discussing short-term vs. long-term goals.

Short-Term vs. Long-Term Goals

Short-term investment horizons often lead to more conservative investment choices to ensure funds are readily available when needed. However, investments with a long-term horizon, such as retirement savings, can tolerate higher levels of risk with the expectation of higher returns over time.

Income annuities are typically chosen for long-term goals due to their higher initial investment requirements.

Medium-term investment horizons balance risk and return by diversifying investment choices between aggressive and conservative assets.

Now, how do you maximize joint income over time?

Maximizing Joint Income Over Time

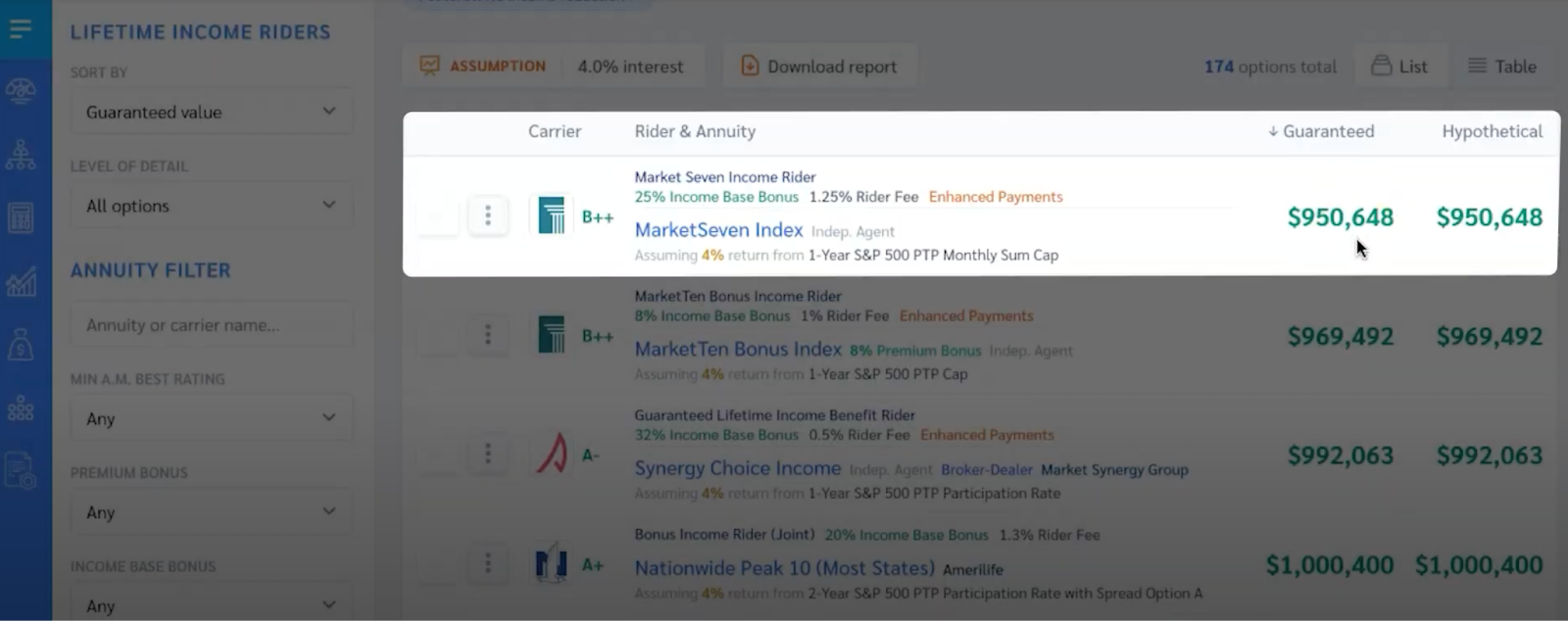

Guaranteed lifetime withdrawal benefits, or guaranteed income, supplement income riders by providing a ‘retirement paycheck’ that grows each year if the income is deferred.

Income annuities can be a viable option for providing stable joint income streams in retirement. For a married couple both aged 60, an investment of $950,000 is necessary to guarantee a yearly income of $100,000, demonstrating the application of income riders in a joint income context.

With a clear understanding of time’s role in index annuity investments, let’s move on to how index annuities fit into retirement planning strategies.

Index Annuities and Retirement Planning Strategies

Indexed annuities are an essential piece in the retirement planning puzzle.

When incorporated into retirement portfolios, these fixed indexed annuities, especially fixed index annuity products like Fixed Indexed Annuities (FIAs) and Registered Index-Linked Annuities (RILAs), optimize risk-reward outcomes and can re-evaluate the effectiveness of traditional portfolio mixes.

A diversified retirement portfolio can also include income annuities to provide stable income streams.

By considering an indexed annuity, investors can further diversify their retirement strategy.

A well-constructed retirement portfolio that includes index annuities and possibly a deferred annuity should have cash reserves and be allocated across assets according to goals and risk tolerance.

Index annuities offer tax-deferred growth, allowing earnings to accumulate without immediate tax implication, making them an attractive option compared to alternatives like certificates of deposit.

Let’s delve into how annuities align with retirement savings goals.

Aligning Annuities with Retirement Savings Goals

Due to record-low interest rates, retirees and near-retirees cannot depend on certificates of deposit and U.S. Treasuries for risk-free income. This makes annuities a viable option to strengthen retirement savings.

Income annuities can help achieve retirement savings goals by providing stable income streams.

Savings annuities provide tax-deferred growth, complementing other retirement plans such as 401(k)s, IRAs, and mutual funds. But how do fixed index annuities compare to variable annuities?

Evaluating Fixed Index Annuities vs. Variable Annuities

Fixed index annuities have returns linked to market performance but offer more predictable and compounded returns compared to a variable annuity, which has returned fully reliant on market fluctuations.

Income annuities typically have higher minimum investment requirements compared to other annuity types.

Both variable and indexed annuities tend to incur higher fees than simpler annuity products, reflecting their complexity, management of investment choices, and any additional customized options or riders chosen by the investor.

Now that we understand how index annuities fit into retirement planning, let’s examine their fees and costs.

Understanding Fees and Costs Associated with Index Annuities

Income annuities often require higher initial investments, impacting overall fees and costs. Insurance companies may charge mortality expenses ranging from 0.5% to 1.5% annually to compensate for the risk they take with annuity contracts, impacting the value of the annuity.

The spread or margin is deducted from the index’s return before the participation rate is applied, which can significantly influence the annuity’s returns. But what about surrender periods and fees? Let’s decode these terms next.

Decoding Surrender Periods and Fees

Surrender periods and fees can be perceived as the fine print in the annuity contract. Understanding these terms is crucial to avoid penalties and to avoid losing money when withdrawing funds from an annuity before the surrender period ends.

Income annuities often have higher initial investments, resulting in higher surrender charges if funds are withdrawn early.

Here are some key points to know about surrender periods and fees:

- Surrender periods in index annuities can range in length, but typical durations are five, seven, or ten years.

- Surrender charges may start around 10% and decrease annually.

- Surrender charges are imposed when funds are withdrawn before the surrender period ends, which is often six to eight years.

Understanding these terms will help you make informed decisions about your annuity.

Insurance companies use surrender charges to recover the costs of commissions paid on annuity contracts during the surrender period. Now, how do insurance companies make money?

Insurance Company Charges and How They Make Money

Understanding how insurance companies make money can provide a clearer picture of the costs associated with index and fixed annuities themselves.

Insurance companies generate profits by employing an interest rate spread method. In this method, they pay themselves and cover expenses before paying interest to policyholders. Income annuities often require higher initial investments, increasing insurance company charges.

An advisor may receive commissions ranging from 2.5% to 7% for selling indexed annuities, costs that are ultimately passed on to the consumer if the contract is surrendered early.

Surrender charges, which typically last 5 to 10 years, allow insurance companies to recoup the upfront commission costs if the policyholder withdraws funds early.

After covering general overhead and profits, insurance carriers pay commissions to representatives and use the remaining yield to purchase options for hedging, providing the potential returns tied to indices for policyholders. Now, let’s explore the factors influencing index annuity performance.

Index Annuity Performance Factors

Considered a form of market insurance, Fixed Index Annuities (FIAs) provide future income while offering a balance of risk and potential returns. Income annuities often require higher initial investments, impacting the potential returns.

Index annuities provide protection from market losses with a minimum rate of return guaranteed, even during stock index declines. However, caps are implemented in index annuities to limit the maximum return participants can achieve, directly influencing the investment’s upside potential.

Let’s delve deeper into this by discussing participation rates and your returns.

Participation Rates and Your Returns

Participation rates play a significant role in determining your returns from an index annuity. A participation rate represents the proportion of an index’s gain credited to the annuity. If the index gains, a 75% participation rate means 75% of that gain is credited to the annuity holder.

Income annuities often have higher initial investments, influencing participation rates.

The portion of market index gain credited to an annuity through participation rates can range from 25% up to 100%. Most contracts initially offer participation rates between 80-90%.

However, a higher participation rate can potentially increase returns from the index’s growth, limits are often in place due to cap rates or spreads.

Now, what about caps on earnings?

Caps on Earnings: What You Need to Know

Caps on earnings serve as the upper limit on the interest that an index annuity can accrue in a given period, thus affecting the potential returns of the annuity. Income annuities often have higher initial investments, which can impact the earnings caps.

Earnings caps in indexed annuities can significantly reduce the amount credited to the account, limiting it to a specified percentage regardless of the full index gain.

Earnings caps limit the amount of index gains credited to the annuity holder, such as capping the credited gain to 7% even if the index itself rises 12%. If an annuity has a cap rate of 6% and the index returns 8%, an annuity with a 100% participation rate would only be credited 6% due to the cap.

Conclusion

As we’ve seen, determining the right investment amount in an index annuity depends on individual financial goals, your personal finance needs, and the desired retirement income.

Booking a call with an annuity expert can provide personalized guidance on annuity strategies and help you make informed decisions about your retirement income.

I can help you:

- Determine the best solution for your unique circumstances

- Navigate and make crucial decisions during your financial journey

- Find the best annuities for your unique situation

By clicking here to schedule a call, I can take a look at specific annuity options and strategize on how to minimize surrender charges.