If you’re planning for retirement, annuity payments can play a big role in shaping your long-term financial security. These payments offer a reliable income stream, often for life, giving you peace of mind when paychecks stop coming in.

Over 20 years, more than 1 in 4 adults over 50 will lose 75% or more of their wealth, and most adults over 70 will face at least one serious financial setback. Planning with annuities can help buffer against these risks by providing consistent income regardless of life’s financial surprises.

Understanding how to calculate annuity payments empowers you to make smarter decisions, whether you’re planning for your future or reviewing your current strategy.

What Is an Annuity and How Does It Work?

An annuity is a financial product that converts a lump sum of money into a series of payments. Insurance companies typically offer annuities to individuals who want steady income, especially after they retire. There are two main categories: fixed and variable annuities.

Fixed annuities offer predictable payments, making them ideal for stability and simplicity. Variable annuities are tied to the performance of investments like mutual funds, which can potentially grow faster but come with more risk. Both types can be used to ensure you don’t outlive your savings.

Annuities work by accumulating funds during the investment phase and then distributing those funds during the payout phase. Depending on the structure you choose, you can begin receiving payments right away or at a later time.

There are lots of annuity options available. To get help with choosing the right annuity and to calculate and the present and future annuity value, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!).

Types of Annuities

Choosing the right annuity starts with understanding the various types available. Each serves a different purpose and comes with its own set of benefits and drawbacks.

- Immediate annuities start paying out almost immediately after you make a lump-sum payment. They’re ideal if you’re already retired or about to retire and need income right away.

- Deferred annuities will begin distributing payments at a later date. This type gives your money more time to grow and can be helpful for long-term retirement planning.

- Fixed annuities provide guaranteed payments based on a fixed interest rate. They’re a go-to option for anyone seeking low-risk, consistent income.

- Variable annuities allow you to invest in different sub-accounts, similar to mutual funds. Your payment amount varies based on investment performance, offering the potential for growth along with risk.

Each type of annuity serves different financial goals, and the best fit depends on your timeline, risk tolerance, and income needs.

Key Factors That Affect Annuity Payments

Several factors influence how much you’ll receive from your annuity. Knowing what affects your payout can help you estimate income more accurately and avoid surprises.

- Principal amount: The initial investment directly impacts how much you can expect in return.

- Interest rate: The rate used to grow your annuity during accumulation affects future payouts.

- Payout frequency: Monthly, quarterly, or annual payouts can alter the total income received.

- Duration of payments: Lifetime payouts typically offer smaller monthly amounts compared to a fixed number of years.

- Annuity type: Whether you choose immediate or deferred annuities changes how and when your income starts.

Your individual choices around these variables will shape your overall income, so it’s important to consider each one carefully.

How To Calculate Annuity Payments Manually

Here’s the general formula for calculating annuity payments:

P = [r*PV] / [1 – (1 + r)^-n]

Where:

- P = payment

- PV = present value or lump sum

- r = interest rate per period

n = total number of payments

For example, if you invested $300,000 at a 4% annual interest rate for 20 years with annual payments, you could calculate your annual income using this formula.

While the math is straightforward, it can be tedious and error-prone.

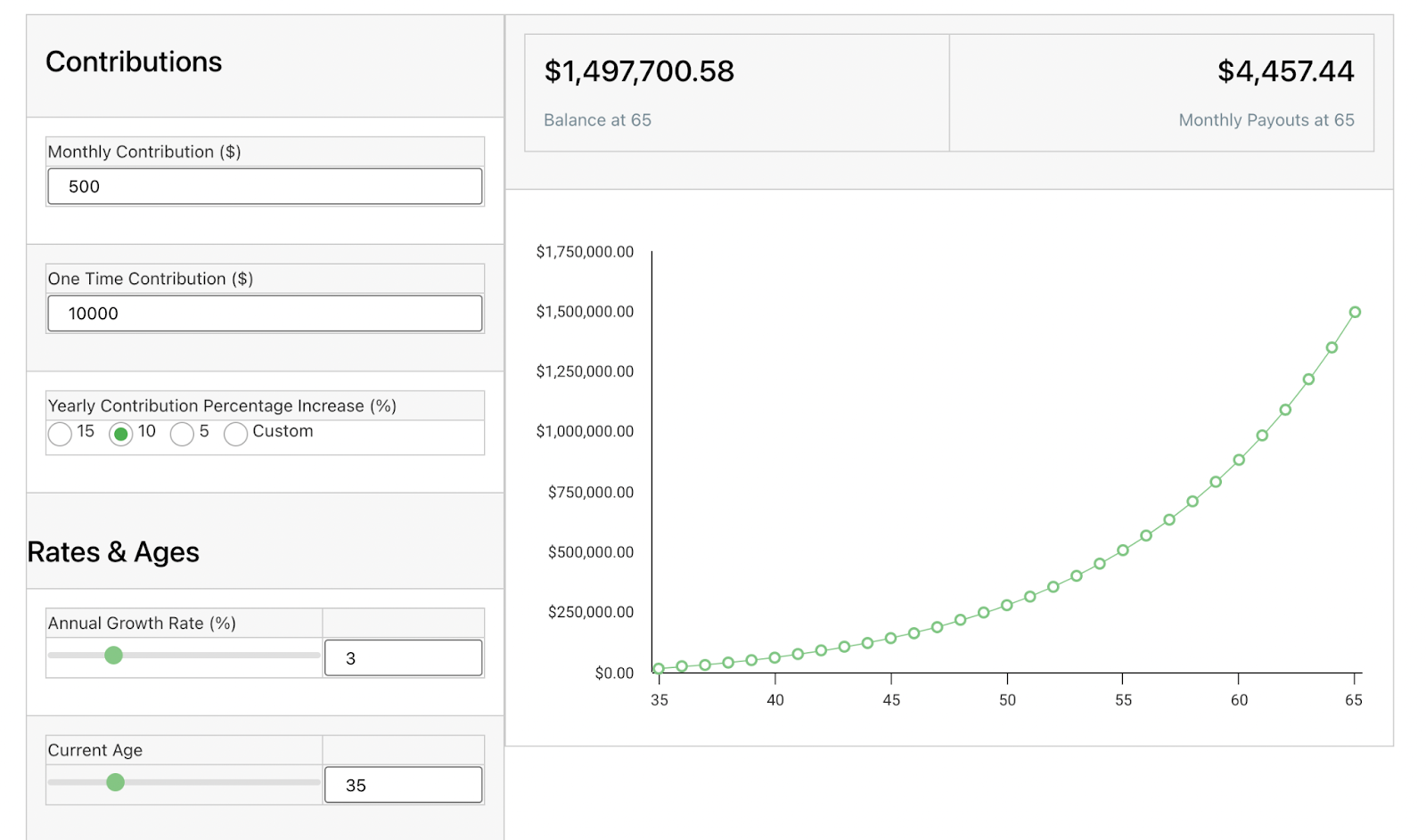

Instead, you can simplify the process using online annuity calculators. These tools allow you to plug in your investment amount, expected interest rate, and payout duration to instantly view your estimated income.

If your annuity includes additional features like an income rider, your payout can change. An income rider calculator lets you estimate how much more income you might receive with this rider added.

Calculate Annuity Payouts for Different Investment Amounts

How much you invest upfront significantly affects your payout. A larger initial investment will result in higher recurring payments. Whether you’re working with a $300,000, a $500,000, or a one-million-dollar annuity, your monthly income will scale based on the size of that investment, the terms of the contract, and the interest rate you lock in.

Alongside investment size, it’s essential to factor in longevity. Planning for a longer retirement means you may want to opt for lifetime payments, even if the monthly amount is slightly lower.

Benefits of Annuities

Annuities come with a range of benefits, especially for individuals looking for financial stability in retirement.

- Guaranteed income: You receive predictable payments that can last for a set period or for life.

- Tax deferral: Earnings grow tax-deferred, which means you won’t pay taxes until you start withdrawing funds.

- Market volatility protection: Fixed annuities and some indexed annuities protect your money from market downturns.

- Retirement planning support: Annuities supplement other retirement income sources like Social Security or pensions.

- Peace of mind: A steady stream of income can ease anxiety around outliving your savings.

These features make annuities a useful financial tool when structured to meet your needs and lifestyle.

Common Mistakes To Avoid When You Calculate An Annuity Payment

Understanding how to calculate annuity payments is one thing, but avoiding pitfalls with whichever annuity you pick is just as important.

- Ignoring fees: Administrative or rider fees can reduce your overall income, so factor them in.

- Forgetting taxes: Annuity income may be taxable. Failing to plan for taxes can shrink your actual take-home amount.

- Assuming constant interest rates: Markets change, and relying on fixed returns can lead to incorrect projections.

- Underestimating life expectancy: Choosing a payout term that’s too short may leave you without income in later years.

Being aware of these common errors helps you plan more accurately and ensures your annuity meets your expectations.

If you want to build a secure retirement income stream, learning how to calculate annuity payments is a decisive first step. Investing $300,000 or $1 million becomes clearer with tools like annuity calculators and income rider estimates to guide your decisions. With the right strategy, annuities can provide the reliable income and peace of mind you need for the years ahead.

Conclusion

With this comprehensive guide, you’re now equipped with the knowledge and tools to understand different types of annuities, calculate annuity payments accurately, and make informed decisions about your financial future.

As you embark on your retirement planning journey, remember to consider liquidity options, payout options, and tax implications to ensure you’re making the best choice for your unique circumstances.

If you need advice on how to handle your annuity needs and to calculate the present and future annuity value, watch this short video to see how I can help you do this (at no cost to you!).