Have you ever considered how to make your money work for you in the long term, especially after retirement?

Annuities can be the answer to your financial planning needs, providing a steady stream of income to support your golden years.

In this blog post, we’ll dive into the annuity formula, its applications, and the pros and cons of annuities as an investment option.

To see an example of how to calculate the present and future value of annuities, watch this video here:

Summary

If you’re short on time, here are the main points of the article:

- The annuity formula is used to calculate the present and future value of regular payments.

- Annuities offer potential tax advantages, additional income, and passive income for attaining personal financial goals.

- Consider both benefits & drawbacks before investing in an annuity as a retirement or financial goal option.

There are lots of annuity options available. To get help with choosing the right annuity and to calculate the present and future annuity value, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!).

Understanding the Annuity Formula

Annuity Definition and Importance

An annuity is a fixed income paid out over a specified period of time, such as monthly or quarterly.

The annuity formula is used to calculate the present value of these periodic payments, which is the amount of money required to be paid today to fund a series of future annuity payments.

This calculation is essential in various financial planning scenarios, such as retirement income, loan payments, or any other circumstances where regular cash outflows occur over time.

Investing in annuities offers several advantages, such as providing additional income to complement pension or Social Security, potential tax advantages, and generating passive income.

Being familiar with the annuity formula and the differences among various types of annuities and payment methods is crucial in making the right choice for your financial goals.

How do I calculate the value of annuities?

Calculating the present and future value of annuities can be complicated because of all the different options available. But don’t worry, it doesn’t have to confusing.

The best way to calculate the present and future value of an annuity is to use software to do all the hard work for you.

And this is exactly what I do with my clients.

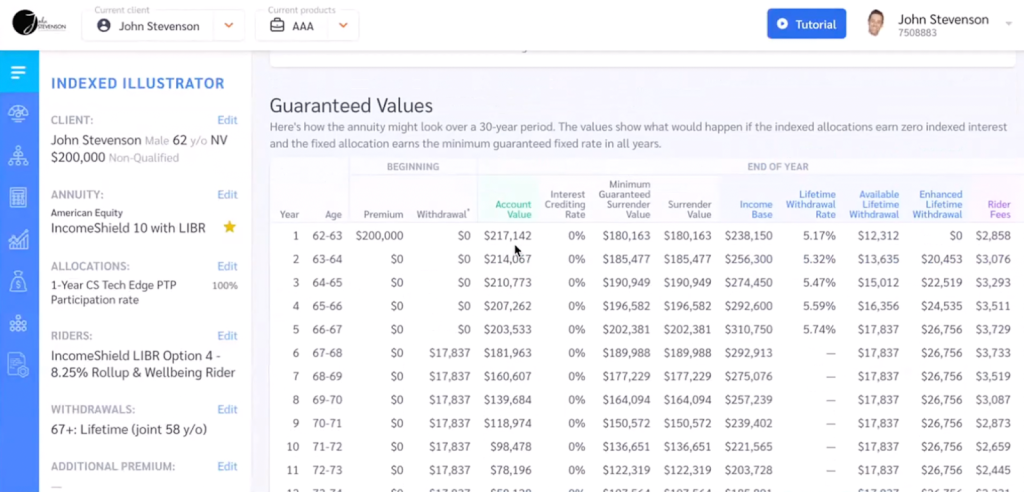

Here’s an example of how annuity software will help you calculate the value of an annuity over time:

Using annuity software, I can enter your information and show you in real-time how the present and future value of your annuity will change over the years.

Furthermore, because I do this every day for clients, I can explain what all the numbers mean and answer any questions you might have.

Watch this video to learn more about how this works so I can calculate the annuity formulas for you (at no cost to you!).

These annuity formulas can be applied in various practical situations, such as retirement planning and loan amortization.

By understanding the basic value of an annuity formula, individuals and financial planners can make informed decisions when selecting and managing annuities as part of their financial portfolios.

Practical Examples of Annuity Formula Applications

The annuity formula can be applied in various practical situations, such as retirement planning, saving for college, and mortgage or loan payments.

Knowing how to use the annuity formula can help individuals make better financial decisions and achieve their long-term financial goals.

Retirement Planning

Retirement planning is the process of determining the amount of funds necessary to sustain a comfortable lifestyle during retirement.

By utilizing the annuity formula, individuals can ascertain the amount they need to set aside for retirement income and calculate the value of their annuity at retirement.

For example, an individual may use the annuity formula to determine how much they need to save each month to ensure a specific income during their retirement years.

This can help them create a comprehensive retirement plan that takes into account their financial needs, goals, and investment strategies.

Loan Amortization

Loan amortization is the process of fulfilling a loan obligation by making periodic payments over a specified period of time.

These payments are composed of principal and interest components, and as the loan is repaid, the amount of principal decreases while the amount of interest decreases.

The annuity formula can be used to calculate the present and future value of loan payments, helping individuals determine the appropriate loan terms and repayment schedules to fit their financial needs.

By understanding how the annuity formula is used in loan amortization, borrowers can make informed decisions about their loan terms and ensure that their debt obligations are manageable and affordable.

Annuity Calculator Tools and Their Reliability

While the annuity formula is a valuable tool for calculating the present and future values of annuities, many individuals opt to use online annuity calculators.

These calculators can provide a reasonable approximation of the present value of annuity payments, but the actual value of an ordinary amount may differ due to unique variables considered by secondary market buyers.

Online Annuity Calculators

These calculators use the time value of money formula to estimate the present value of annuity payments, taking into account factors such as payment amount, interest rate, and the number of periods.

It’s important to note that the results provided by online annuity calculators are estimates and should be taken as such.

While these tools can give a good indication of the present value of annuity payments, they may not account for all variables and factors that can influence the actual value of the annuity.

Limitations and Considerations

When using online annuity calculators, it’s essential to know their limitations and the factors to consider when interpreting the results.

The accuracy of the results, the assumptions made by the calculator, and the complexity of the annuity product being calculated may all be among the limitations and considerations to be taken into account when using these tools.

Additionally, it’s crucial to consider factors such as changes in interest rates, inflation, and other variables that can have an impact on the value of annuities.

By taking these factors into account, individuals can make more informed decisions about their annuity investments and better plan for their future financial needs.

Advantages and Disadvantages of Annuities

Annuities can be a valuable investment option for individuals looking to secure a steady retirement income or achieve specific financial goals.

However, it’s essential to weigh the advantages and disadvantages of annuities before investing in them.

Benefits of Annuities

Annuities offer several advantages, such as guaranteed income, tax-deferred growth, and the potential for growth and protection of income that can last throughout one’s lifetime.

Guaranteed income ensures that individuals will receive a steady income stream for as long as necessary, providing financial security during retirement or other periods of reduced income.

The benefit of tax-deferred growth allows individuals to save a considerable amount of money while deferring the payment of taxes on their invested capital until withdrawal.

This enables faster growth of funds and a greater retention of them, which can be especially beneficial for long-term financial planning.

Drawbacks of Annuities

Despite their benefits, annuities also come with several disadvantages, including high fees, lack of liquidity, and limited control. High fees can significantly reduce the overall return on investment, making annuities a potentially costly investment option.

Lack of liquidity refers to the inability to readily convert annuities into cash, which can be a problem if the annuitant requires access to funds in an urgent manner.

Limited control implies that annuities are not readily manageable or supervised, which can be an issue for individuals who want to ensure that their funds are being invested in an appropriate manner.

Conclusion

Annuities can be a valuable financial planning tool for individuals looking to secure a steady income during retirement or achieve specific financial goals.

By understanding the annuity formula, its applications, and the advantages and disadvantages of annuities, individuals can make informed decisions about their investments and financial planning strategies.

Frequently Asked Questions

How much does a $500000 annuity pay per month?

A $500,000 annuity can provide you with a steady stream of income every month. Purchasing this annuity at age 60 and beginning to receive payments immediately would in some situations yield around $2,400 per month for the remainder of your life.

However, every annuity company offers different rates depending on your unique situation. So it’s best to speak to an annuity specialist to calculate how much an annuity will pay you each month.

An annuity can be a great way to supplement your retirement income and ensure that you have a steady source of income for the rest of your life. It can also provide you with information.

How much does a $1,000,000 annuity pay per month?

For a $1,000,000 annuity purchased at age 60, you can expect to receive monthly payments of roughly $5,083 per month in some situations. However, every insurance company offers different annuity rates. That’s why it’s a good idea to speak to an annuity specialist to calculate the value for you.