Securing the best annuity rates in 2024 is the key to a prosperous retirement.

With this expert guide on how to secure the best annuity rates in 2024, you’ll discover the top strategies for navigating the annuity market and locking in favorable rates, ensuring a steady income stream when you need it most.

Summary

- The highest annuity rates are always changing. If you’d like to see the best annuity rates right now, use our annuity calculator or click here to schedule a call and we can walk you through them.

- Understanding different types of annuities, such as fixed, variable, and fixed index annuities, and their rates is essential in aligning one’s retirement strategy with their financial goals and risk tolerance.

- Strategic timing can influence securing the best annuity rates, as rates often reflect changing economic conditions. A larger initial investment can lead to more substantial payouts.

- Guaranteed lifetime annuities offer financial security by providing a steady income for life, which can be enhanced with income riders while deferring payouts can lead to increased income due to tax-deferred compounding.

Need help choosing the best annuity for your unique situation? Have questions about getting an annuity? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

The highest annuity rates based on types and terms

An annuity contract is essentially an agreement with an insurance company, designed to provide you with regular payouts for life.

Fixed annuities offer a guaranteed rate of return over a set period, which translates into a stable payment amount throughout the term of the contract. These fixed annuity rates are the bedrock of your financial predictability, shielding you from the unpredictable tides of market volatility.

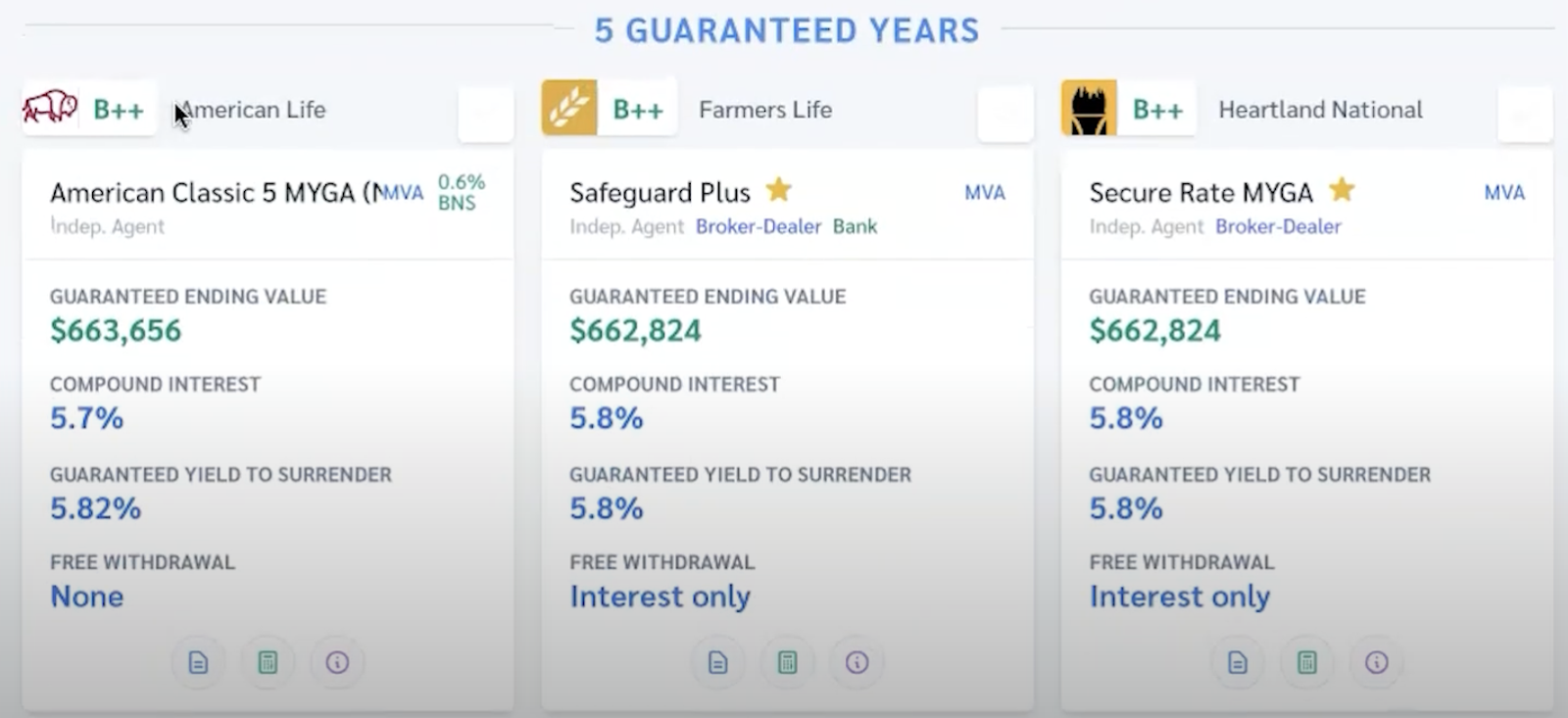

Here’s a screenshot of the top fixed MYGA annuity rates for 5 years (at the time of writing this article) with a $500K annuity.

To see the latest rates, click here to schedule a call.

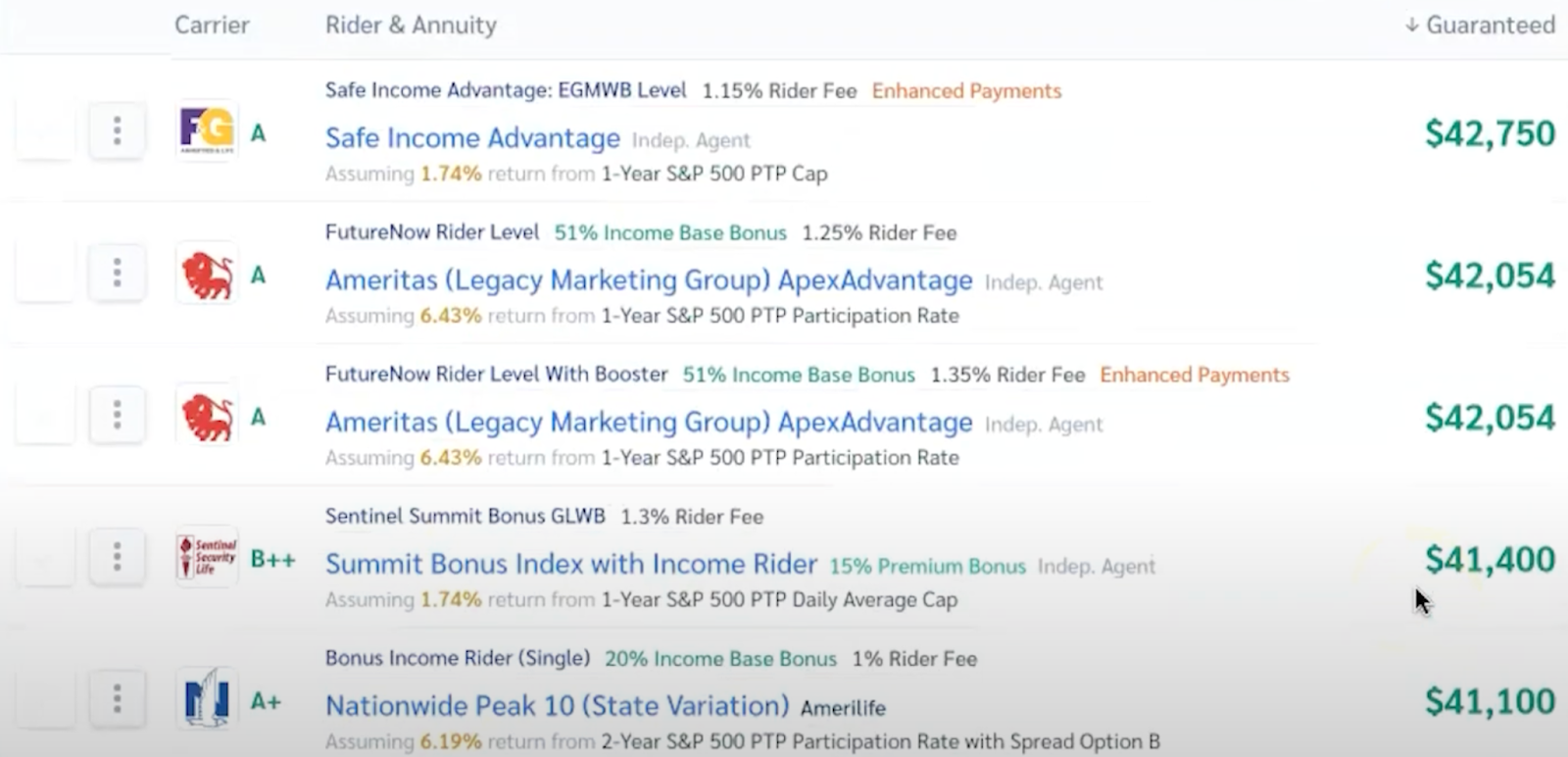

If you’re looking for the highest income rates, let’s look at index annuities with income riders.

Right now, a $500K index annuity with an income rider will provide an annual payout of $42,750/year for life, as of the writing of this article:

To see the latest rates, click here to schedule a call.

Each type of annuity has a distinct impact on annuity rates. To align your retirement strategy with your financial goals and risk tolerance, it’s vital to compare these rates. The goal of securing the best annuity rates begins with a clear understanding of these fundamental distinctions.

Maximizing Returns on Fixed Annuities

Obtaining the best fixed annuity rates requires a mix of wise timing and strategic investing. In the current climate, where the best 5-year fixed annuity rates are at a historical peak of 6.15%, the potential for a prosperous retirement income is substantial.

The key to maximizing returns on fixed annuities lies not only in the allure of these rates but also in leveraging the right investment strategies.

The Impact of the Investment Amount

The adage ‘the more you put in, the more you get out’ resonates profoundly with fixed annuities. A larger initial investment can significantly enhance the payout benefits, resulting in a more sizable and predictable income stream during the payout phase.

This is because fixed annuities purchased with heftier investments are likely to provide more predictable and potentially higher returns than those funded with modest sums.

The size of your investment not only affects your guaranteed income stream but is also a determining factor in the annuity rates you are offered.

Timing Your Annuity Purchase

However, the timing of your investment is as critical as the amount you invest. As economic conditions ebb and flow, so do annuity rates, often reflecting changes in prevailing interest rates.

Hence, timing your annuity purchase during a period of rising interest rates can lock in a more lucrative income for the future.

This strategic timing can lead to better long-term outcomes for annuity income, as current rates are at historical highs, providing a ripe opportunity for securing better returns.

To learn how to find the best fixed annuity rates, click here to schedule a call.

Ensuring Lifetime Income with Guaranteed Annuities

In the face of life’s uncertainties, guaranteed lifetime annuities serve as a pillar of financial security, offering an income that lasts as long as the annuity owner lives. The allure of a guaranteed income stream, impervious to the tempests of economic downturns, is a beacon of stability for many retirees.

Furthermore, joint and survivor annuities extend this financial lifeline to a surviving spouse, ensuring that the tides of change do not erode the remaining partner’s financial foundation.

Evaluating Income Riders

Annuities can be adorned with various options to enhance their value. Income riders, such as guaranteed lifetime withdrawal benefits (GLWBs), offer a secure income stream for life, unaffected by market conditions.

These enhancements provide a steady and reliable source of income. These riders influence the initial fixed annuity rates, reflecting the additional benefits they offer, and play a significant role in shaping the final fixed income of annuity products.

It’s crucial to evaluate these options, as they may slightly adjust the initial annuity rates but provide invaluable financial stability and peace of mind.

Strategic Annuity Deferral for Enhanced Returns

Postponing annuity payments can be compared to aging a fine wine–it increases its value over time. Deferred fixed annuities are crafted for long-term financial planning, affording your savings the luxury of tax-deferred growth and positioning you for a more bountiful future payout.

By delaying the payout phase, your funds have more time to compound, leading to increased income and a stronger return on the investment when you start to withdraw income.

The Power of Tax-Deferred Growth

The tax-deferred growth within deferred annuities is a potent force in wealth accumulation. Earnings within the annuity grow without the immediate drag of taxes, only becoming subject to taxation upon withdrawal.

For high earners who have maxed out other tax-deferred options, this can be a strategic maneuver to continue building wealth without the immediate tax bite.

When funds are withdrawn, they are taxed at the ordinary income tax rate, but until then, the compounding occurs on a tax-deferred basis, amplifying the growth potential of the investment.

Fine-Tuning Your Annuity Strategy

For successful retirement planning, it’s necessary to recalibrate your strategy regularly.

The process involves:

- Regular review and adjustment to align with evolving financial goals and market conditions

- Securing competitive annuity rates that bolster long-term financial security

- Ensuring a comfortable standard of living throughout retirement

Comparing annuity rates from various providers is a vital step in this process, as it can lead to maximized returns and achieving financial goals.

Click here to watch a short video to see how I can do this all for you (at no cost to you!).

Reviewing Annuity Contracts Regularly

It is crucial to ensure that the annuity remains aligned with your financial goals and adapts to the changing of interest rates.

This annual review can reveal whether older annuities are underperforming due to shifts in interest rates, thus providing opportunities to adjust your course for optimal performance.

Annuity Companies: Choosing Your Provider

Choosing the best annuity company is a crucial step in your journey toward retirement security. The provider’s financial stability is essential to ensure they can fulfill long-term payment obligations and provide financial peace of mind.

Companies like ANICO, Heartland National, and Nassau offer a range of annuity products with varying benefits and minimum investment requirements, which can cater to individual needs and preferences.

Additionally, customer service is an integral aspect to consider, as it can greatly influence the overall satisfaction with the annuity provider.

Comparing Annuity Providers

When comparing annuity providers, it’s vital to balance the costs and benefits of each company’s annuity products.

This assessment must account for the potential impact of mortality and expense (M&E) charges on variable annuity contracts, as these can reflect either enhanced benefits or superior investment performance.

Consulting With a Trusted Advisor

Booking a call with a trusted advisor who specializes in annuities can help you find & compare the best annuities for your unique situation.

Click here to schedule a call with me.

By navigating the different types of annuities, maximizing returns through investment and timing, ensuring lifetime income with guaranteed options, and deferring for tax advantages, you can have a secure and comfortable retirement.