If you’re wondering how to compare different types of annuities, it’s essential to consider how each fits your financial goals.

This guide will outline the key features of fixed, variable, indexed, immediate, and deferred annuities, helping you make a clear and informed choice.

Summary

- Annuities are categorized into five main types: fixed, variable, indexed, immediate, and deferred, each serving distinct financial goals.

- Income riders enhance the security of annuities by providing guaranteed income streams and are crucial for retirees concerned about longevity risk.

- Consulting a financial planner is advisable to navigate the complexities of annuities and ensure alignment with individual financial goals.

Need help choosing the best annuity for your unique situation? Have questions about getting an annuity? If so, it’s best to speak with an annuity specialist. Watch this short video to see how I can help you do this (at no cost to you!)

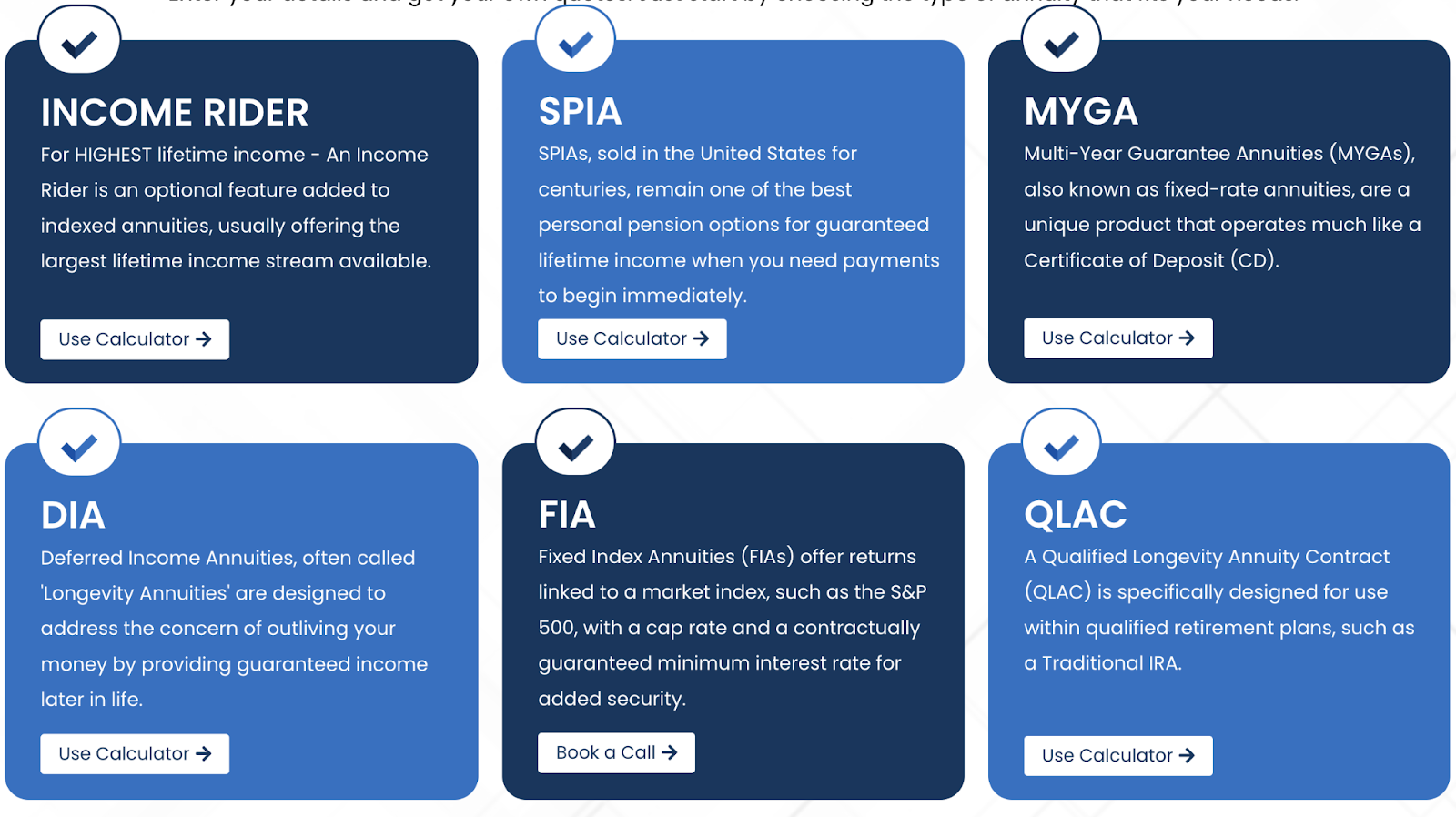

Tip: See how much an annuity could pay you using our annuity calculator.

With the annuity calculator you can enter your details and get your own quotes. Just start by choosing the type of annuity that fits your needs.

What Types of Annuities Are There?

There are five basic types of annuities. These include fixed, variable, indexed, immediate, and deferred. Each type caters to distinct financial objectives, balancing the need for growth and income provision.

Whether you seek principal protection, higher returns, or immediate payouts, knowing the specifics of each type can help you make an informed choice.

Fixed Annuities

A fixed annuity can be a valuable addition to a retirement strategy. However, locking in a fixed rate now could mean missing out on higher interest rates in the future.

Despite this, fixed annuities remain a popular choice for those prioritizing security and guaranteed income.

Indexed Annuities

Indexed annuities combine features of both fixed and variable annuities, offering a guaranteed minimum interest rate along with the potential for higher returns based on a market index.

This blend provides a moderate risk profile, appealing to those who want growth potential without the full exposure to market volatility that variable annuities entail, including fixed index annuities.

Indexed annuities balance safety and growth. Features such as a floor limit investment loss and a buffer protect your principal from market downturns while allowing you to benefit from market upswings.

This makes indexed annuities an attractive option for those looking to hedge against inflation while maintaining some level of security.

Immediate Annuities

Immediate annuities begin making payments right after you make a lump-sum premium payment. This type of annuity is perfect for those who need a guaranteed income stream right away, such as individuals who have just retired and are looking to replace their paycheck with a steady income.

Converting a lump sum into regular payments, an immediate annuity ensures financial stability and peace of mind.

The primary benefit of immediate annuities is the assurance of a guaranteed income stream for life. This can be particularly beneficial for retirees concerned about outliving their savings, offering a reliable source of funds to cover daily expenses.

Deferred Annuities

Deferred annuities accumulate funds over time, with payouts starting at a future date, allowing contributions to grow on a tax deferred basis until payments begin.

A deferred annuity is ideal for long-term retirement planning, providing a way to build a substantial nest egg that will generate income in the future.

Deferred annuities come in both fixed and variable forms, each offering different levels of risk and return. Whether you prefer the stability of fixed returns or the potential for higher gains through market investments, deferred annuities offer flexibility to match your financial goals.

Comparing Growth and Income Options

Annuities are categorized based on when payments start and how they are invested, which determines their suitability for growth or income.

During the accumulation phase, your contributions grow tax-deferred, and during the distribution phase, you receive regular payments. Understanding the growth and income options available can help you choose the right annuity to meet your retirement needs.

Income riders are optional features in deferred annuities that ensure a steady income stream for life. These riders add a growing benefit base that can potentially increase future income from the annuity.

Enhancing annuities with income riders secures guaranteed lifetime income, ensuring long-term financial stability.

Annuities for Growth

Variable annuities allow investments in sub-accounts linked to market performance, offering potential growth that can outpace inflation. Allocating funds across different sub-accounts allows investors to achieve higher returns tied to market performance.

This makes a variable annuity suitable for those willing to take on more risk in exchange for greater growth potential.

Indexed annuities also offer growth potential by linking returns to a specific market index. While they provide some level of protection against market downturns, the potential for growth is still tied to market performance.

This blend of safety and market participation makes indexed annuities and registered index linked annuities a balanced choice for growth-oriented investors.

Guaranteed Growth Annuities

Multi-Year Guaranteed Annuities (MYGAs) offer fixed interest rates that exceed those of traditional CDs, providing stability in returns. These annuities guarantee a specific interest rate over multiple years, offering a predictable income stream.

This stability makes MYGAs an attractive option for conservative investors looking for guaranteed growth.

MYGAs offer higher returns compared to traditional savings options like CDs, without exposing your principal to market risks. This makes them a reliable choice for those seeking steady, guaranteed growth in their retirement portfolio.

Guaranteed Income Annuities

Single Premium Immediate Annuities (SPIAs) provide guaranteed income starting soon after the premium is paid, making them ideal for immediate financial needs. SPIAs start payouts immediately, ensuring a constant income stream to cover essential expenses. This makes them a suitable option for retirees who need income right away.

Deferred Income Annuities (DIAs), on the other hand, allow for a single premium payment with income payouts beginning at a future date. This flexibility caters to long-term income planning, providing a reliable source of funds when needed.

Both SPIAs and DIAs offer guaranteed income, tailored to meet different timing needs.

The Role of Income Riders

Income riders can provide guaranteed minimum income, ensuring financial stability regardless of market fluctuations. These additional features attached to income annuity enhance income security during retirement, making them an essential consideration for those looking to mitigate longevity risk.

Understanding the role of income riders enables more informed decisions about annuity choices.

Highest Guaranteed Lifetime Payout

Income riders, such as the Guaranteed Lifetime Withdrawal Benefit, ensure a minimum annual withdrawal amount for the lifetime of the annuitant. This feature provides the highest guaranteed lifetime payout for annuities, offering peace of mind for retirees.

When attached to a Fixed Indexed Annuity, income riders can guarantee a higher income compared to other options.

The assurance of a guaranteed lifetime payout makes income riders an attractive addition to annuities, particularly for those concerned about outliving their savings. This security can significantly enhance the quality of retirement life.

Market Protection and Growth

Fixed Indexed Annuities (FIAs) combine the safety of fixed annuities with the growth potential linked to stock market indexes. Attaching income riders to FIAs enhances income generation opportunities while ensuring market protection.

This combination provides additional security and growth, balancing risk and reward.

Income riders on FIAs offer predictable income streams, ensuring financial stability despite market fluctuations. This makes them a compelling choice for those seeking a blend of safety and growth in their retirement portfolio.

Additional Costs and Considerations

Using income riders usually incurs additional fees that may reduce the overall value of the annuity. These fees, typically ranging from 0.25% to 1.5% of the contract value annually, can significantly impact the income payouts from the annuity.

Analyzing the costs and benefits associated with income riders is crucial before adding them to your annuity.

While income riders provide enhanced security and potential benefits, the associated costs must be carefully considered to ensure they align with your financial goals. Making an informed decision requires a thorough understanding of these additional expenses.

Special Features and Benefits

Annuities often come with unique features and benefits that cater to various financial planning needs, allowing for customized income solutions. Understanding these special features can help you tailor your annuity to better meet your specific retirement goals.

Qualified Longevity Annuity Contract (QLAC)

Purchasing a Qualified Longevity Annuity Contract (QLAC) allows individuals to defer required minimum distributions (RMDs) from retirement accounts until age 85. This deferral provides flexibility and longevity protection, ensuring that you have a reliable income stream later in life.

With a QLAC, you can defer up to $200,000 of qualified money until age 85, providing a significant benefit for long-term retirement planning. This makes QLACs a valuable tool for those looking to manage their RMDs and extend their retirement income.

Period Certain Options

Period certain options guarantee income payments for a set duration, ensuring financial support for beneficiaries even if the annuitant passes away. These options are particularly beneficial for non-spousal beneficiaries, providing a reliable income stream for a specified period.

Guaranteeing payments for a fixed period, period certain options protect beneficiaries from income loss, providing peace of mind and financial security. This feature makes annuities more versatile and supportive of broader financial planning needs.

Death Benefit Riders

Death benefit riders ensure that beneficiaries receive a predetermined sum from the annuity upon the annuitant’s passing. This can provide significant financial support and peace of mind, knowing that loved ones will be taken care of.

The specific amount paid to beneficiaries can vary based on the terms set in the annuity contract, ensuring that the initial investment or the highest value reached by the annuity is protected. Death benefit riders are thus a valuable addition for those seeking to secure their legacy.

Making an Informed Decision

Understanding your financial situation, risk tolerance, and income needs is crucial to selecting the right annuity. Assessing these factors helps narrow down options and choose an annuity that aligns with your retirement goals.

Consulting a financial advisor who specializes in annuities can provide personalized assistance with annuity decisions, helping you navigate complex products and make informed choices. This professional guidance ensures that you select the best annuity features and benefits to meet your specific needs.

Assessing Your Financial Goals

Knowing what you want and being realistic about your limits can help you narrow down your annuity options. Understanding your risk tolerance is essential to selecting the most suitable annuity.

Before exchanging or replacing your annuity, do a close comparison with your existing annuity, considering the benefits and drawbacks of each option. This thorough assessment ensures that you make the best choice for your financial future.

Consulting Financial Fiduciaries

Professional guidance can clarify complex annuity options and help align them with your individual needs. Annuity products can be intricate and often require specialized knowledge to navigate effectively.

Consulting knowledgeable financial fiduciaries is recommended to ensure you make informed decisions about annuities that align with your financial goals and risk tolerance.

When seeking advice, ensure your advisor or insurance broker is properly credentialed.

Conclusion

Annuities offer a versatile solution for securing retirement income, with various types catering to different financial needs. Understanding the differences between fixed, indexed, immediate, and deferred annuities is essential for tailoring your retirement plan.

Special features like income riders, QLACs, period certain options, and death benefit riders can further enhance the benefits and security of your annuity investments.

Making an informed decision about annuities involves assessing your financial goals, understanding the associated costs, and consulting with financial professionals.

By doing so, you can ensure a stable and predictable income stream for your retirement, providing peace of mind and financial security for the long term.

Need help with finding the best annuity?

Click here to schedule a call with me.

On the call, I can help you:

- Determine what type of annuity is best for you

- Find the highest paying annuities for your unique situation

- Answer any other questions you may have