For decades, the deal felt straightforward: pay into Social Security through every paycheck, then collect benefits in retirement tax-free.

That assumption is wearing thin. Retiree confidence in Social Security dropped to 60% in 2026, while 69% of retirees now express concern about federal changes to the retirement system. Anxiety about the program’s future has become a regular feature of American financial life. Yet a new survey by John Stevenson suggests the most pressing threat to retirement income isn’t a future cut. It’s a tax most Americans don’t know exists.

The survey of 1,000 U.S. adults near or in retirement, found that 53.3% of those earning under $25,000 a year believed Social Security benefits were always tax-free. They aren’t.

Up to 85% of benefits can be added to a retiree’s taxable income depending on their total income, then taxed at their normal income tax rate. The rule began in 1984 and expanded in 1993, with the income thresholds untouched ever since.

Key Findings

- 53.3% of Americans earning under $25K believed Social Security benefits were always tax-free, the highest of any income group.

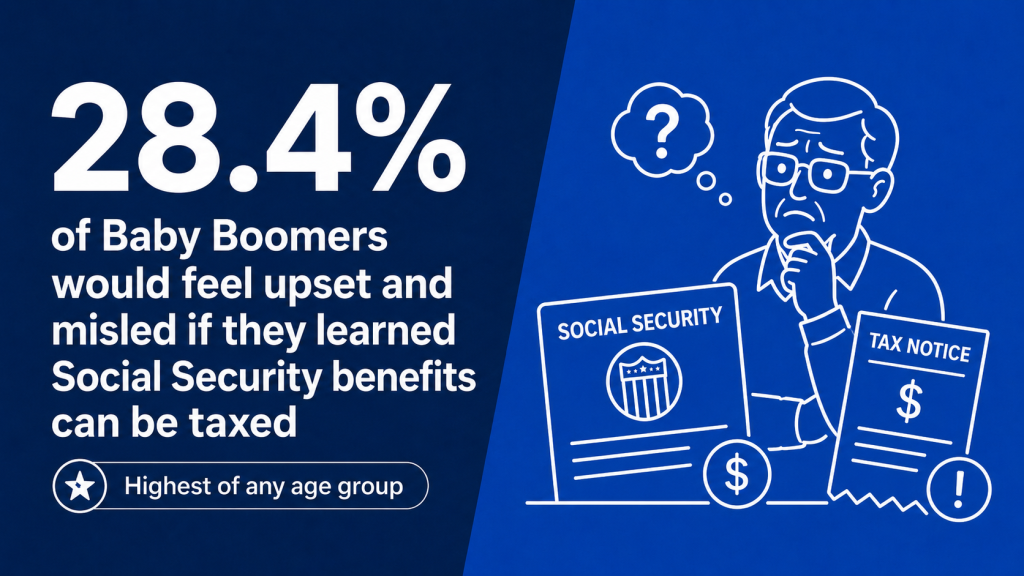

- 28.4% of Baby Boomers said they’d feel “upset and misled” upon learning Social Security can be taxed.

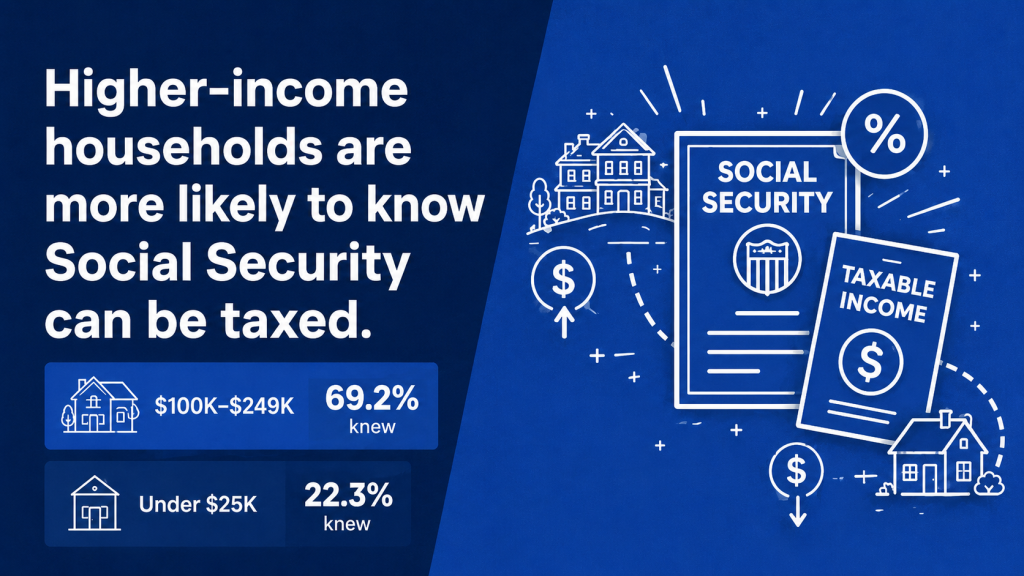

- 69.2% of households earning $100K–$249K knew benefits could be taxed federally, compared to just 22.3% of those earning under $25K.

- 81.8% of respondents said they don’t fully understand when Social Security becomes taxable.

- 69.9% said they don’t trust the government to keep Social Security rules stable through their retirement.

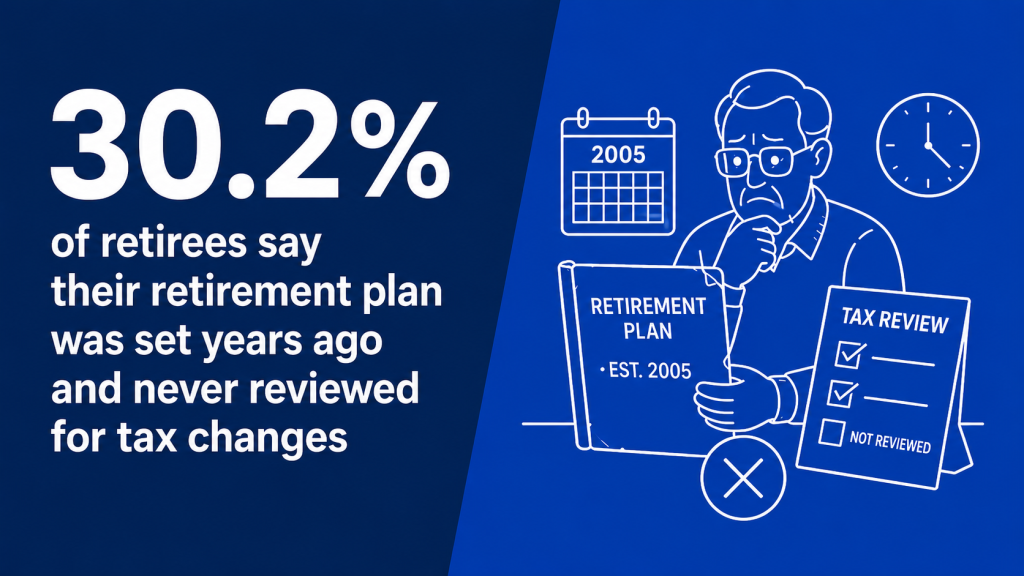

- 30.2% of retirees said their retirement plan was set years ago and has never been reviewed for tax law changes.

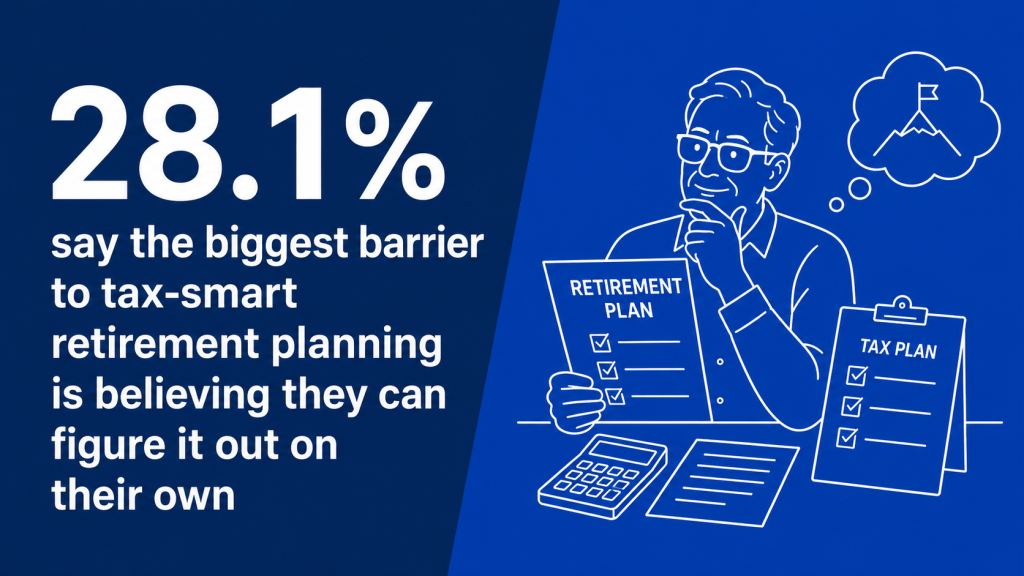

- 28.1% said the biggest barrier to tax-smart retirement planning is believing they can figure it out alone.

A Promise That Quietly Changed

For most of Social Security’s history, benefits were exempt from federal income tax. That changed in 1983, when Congress, acting on the Greenspan Commission’s recommendation, voted to tax benefits for higher-income retirees starting in 1984. The thresholds were set at $25,000 for single filers and $32,000 for married couples, and the commission estimated only about 10% of beneficiaries would ever owe.

Forty-two years later, that estimate looks almost quaint. Roughly half of all retirees now pay tax on their benefits, up from the 8-10% originally affected, an expansion that happened without any new law, any vote in Congress, or any headline announcing a tax increase.

The reason is mechanical. The income thresholds were never indexed to inflation. If Congress had indexed the $32,000 married-couple threshold to wage growth, it would exceed $96,000 today. Every year, normal cost-of-living adjustments to Social Security benefits push more retirees over a line that doesn’t move. The line that once applied to wealthy retirees now applies to people drawing modest pensions alongside their benefits.

Whether a retiree owes tax depends on a calculation called “combined income,” sometimes called provisional income. It’s the sum of their adjusted gross income, any tax-exempt interest, and half of their annual Social Security benefits. Cross over $25,000 as a single filer or $32,000 as a couple, and up to 50% of benefits become taxable. Cross over $34,000 single or $44,000 jointly, and that jumps to 85%. Those four numbers are the entire framework, and they haven’t budged since the Reagan and Clinton administrations.

The People Most Affected Know the Least

The survey’s sharpest divide is economic. 69.2% of households earning $100K–$249K already knew Social Security could be taxed. Among those earning under $25K, only 22.3% did.

The gap widens further by education: 72.3% of postgraduate professionals knew, compared with 18.9% of those without a high school diploma.

This is the inversion of how a fair retirement system would work. The Americans most reliant on Social Security as their primary income source when they retire are the least likely to know the IRS will take a cut.

For a 65-year-old living on the average benefit, the math is unforgiving. The average Social Security retirement benefit has risen to approximately $2,071 per month, or roughly $24,852 annually. That puts the average retiree just $148 below the single-filer threshold from benefits alone. A part-time job, a small pension, or a required minimum distribution from a 401(k) is often enough to push them across.

Required minimum distributions, or RMDs, are mandatory yearly withdrawals the IRS forces retirees to take from traditional 401(k) and IRA accounts starting at ages 73-75 spending on the year you were born. A retiree with $500,000 in a traditional IRA might face RMDs of $20,000 or more annually. That single requirement can push someone from owing nothing on their Social Security to having 85% of their benefits taxed in the same year.

Baby Boomers Feel Misled

28.4% of Baby Boomers said they’d feel upset and misled if they learned Social Security benefits can be taxed, the highest of any age group. Among respondents without a high school diploma, that figure climbed to 39.6%.

These respondents aren’t hypothetical retirees decades from now. They’re already collecting benefits. Many are already paying taxes on them and don’t know why. The frustration is partly financial, but it also comes from feeling that the rules of a system they paid into for 40 years shifted underneath them while they weren’t looking. For a typical middle-income retiree, taxation on Social Security benefits can add several thousand dollars to a yearly tax bill, money that wasn’t part of the original retirement projection.

Distrust extends well beyond Boomers. 69.9% of survey respondents said they don’t trust the government to keep Social Security rules stable through their retirement. Among Gen Z, 38.6% said they don’t trust it at all. Among the highest earners, those making over $250K, 60% said they don’t trust it much. That distrust isn’t unfounded. The Social Security trust fund is currently projected to be depleted by 2032, after which retirees would still receive benefits but at significantly reduced levels unless Congress acts. Skepticism about Social Security shows up across income brackets and across generations, making it one of the few financial concerns shared by nearly every demographic the survey measured.

Plans Frozen in Time

Tax law shifts constantly. Required minimum distribution ages have moved. Contribution limits have risen. In 2026, West Virginia became the 42nd state to eliminate state income tax on Social Security benefits, and the Trump administration’s “One, Big, Beautiful Bill” introduced a $6,000 tax deduction for eligible seniors 65 and older through 2028.

Yet 30.2% of retirees said their retirement plan was set years ago and has never been reviewed for tax changes. Among those earning under $25K, that figure climbs to 42.5%. The Americans least likely to have updated their plans are also the ones least likely to know the taxation rules exist.

The headline tax breaks of 2026 don’t change the underlying framework that determines whether benefits get taxed in the first place. The 50% taxation tier set in 1984 and the 85% tier added in 1993 both remain exactly as written. Retirees hearing political promises about “ending Social Security taxation” may believe the problem is solved when the underlying rules remain untouched.

The Tax Torpedo Almost Nobody Sees Coming

Once a retiree crosses the first taxation threshold, the system creates a punishing feedback loop financial planners call the “tax torpedo.” Every additional dollar of income from a part-time job, an IRA withdrawal, or interest on savings doesn’t just get taxed at the normal rate. It also pulls more Social Security benefits into taxable territory at the same time. The result is an effective tax rate that can hit 40% or higher for retirees who are nominally in a low tax bracket.

This is the mechanic that turns a small income increase into a disproportionately large tax bill. A retiree earning $30,000 who picks up a $5,000 freelance project might assume they’ll owe a few hundred dollars in extra tax. The actual number can be more than double that, because the additional income makes more of their Social Security benefits taxable too. Most retirees don’t see it coming because the formula is invisible until the return is filed.

The Confidence Trap

The most common reason Americans skip tax planning is confidence. 28.1% said the biggest barrier to tax-smart retirement planning is believing they can figure it out on their own. Among Gen Z, that spikes to 56.8%. Among postgraduate professionals, it’s 40.2%.

The irony is that the people most certain they can DIY their retirement taxes are often the ones with the most complex situations, with multiple income streams, IRAs, pensions, part-time work. The IRS itself publishes multi-page guides on Social Security taxation alone. The system is complicated by design, and overconfidence is what keeps people from asking for help until the bill arrives.

That overconfidence is also driving expensive decisions. 26.6% of Millennials said they’d claim Social Security earlier to lock in benefits if they learned taxes were a factor, the highest of any generation. Claiming at 62 instead of waiting until full retirement age, currently 67 for most workers, permanently reduces monthly benefits by roughly 30%. That reduction lasts the rest of a retiree’s life. The generation most reactive to tax risk may be making the choice most likely to increase their lifetime tax burden and shrink their lifetime income simultaneously.

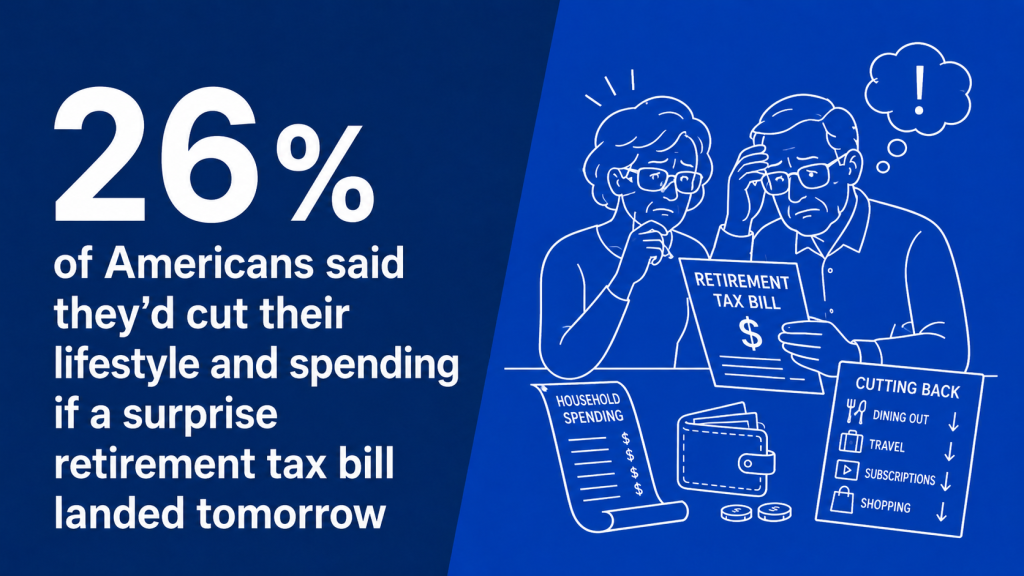

When Surprise Becomes Strategy

If a surprise retirement tax bill landed tomorrow, 26% of Americans said they’d cut their lifestyle and spending. Among those without a high school diploma, 35.8% said they’d “hope for the best and deal with it later.”

Tax planning, in other words, is becoming a luxury. The people with advisors plan ahead. The people without them adjust on impact, usually by spending less or claiming earlier. Neither is a good outcome for a system designed to provide stability in old age.

Modeling tax exposure ahead of time is what separates a smooth retirement from a reactive one. Annuity calculators and combined-income worksheets can help retirees see how different income sources will interact with Social Security, but only if they know to look. The Social Security Administration provides free benefit estimates online, yet 40.6% of Millennials and 37.7% of Gen X have never checked theirs.

Summary

Social Security was sold to generations of Americans as a guarantee. What the survey makes clear is that the guarantee comes with footnotes most people never read, footnotes written in 1984 and never revised. The rule has been hiding in plain sight for decades, catching more people every year as inflation pulls modest incomes into a tax bracket that was once reserved for the wealthy.

The retirement tax landscape is getting more layered and more dependent on individual literacy. The retirees who fare best won’t necessarily be the ones who saved the most. They’ll be the ones who understood the rules early enough to plan around them.

For everyone else, the most useful thing they can do this year is small. Pull up their Social Security estimate. Calculate their combined income. Find out whether the safety net they’re counting on comes with a bill attached.

Methodology

To understand how Americans approach Social Security taxation and retirement planning, we surveyed 1,000 adults near or in retirement across the country. Participants answered a series of questions about their understanding of Social Security tax rules, their reactions to learning benefits can be federally taxed, their trust in the program’s stability, and how they would adjust their retirement plans in response to a surprise tax bill. Responses were analyzed across age, gender, household income, education level, and ethnicity to identify trends and disparities. The sample skewed toward Gen X (n=486) and Baby Boomers (n=405), with smaller representation from Millennials and Gen Z.

Fair Use Policy

Users are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.