Most Retirees Fear a Tax Surprise, But Few Have Done Anything About It

Americans spend decades saving for retirement, tracking their 401(k)s, monitoring the market, and calculating how much they’ll need to stop working. What most do not calculate, however, is how much of that money will get taxed by the IRS once it’s pulled out.

A March 2026 national survey from John Stevenson reveals that 32.8% of U.S. adults (approaching or already in retirement) have no tax plan for their retirement income. Among Baby Boomers, the group with the least amount of prep time, that figure rises to 36.3%. Only 14.1% of all respondents have a written plan.

New, broader, research shows that over half of Americans say the complexity of the federal tax system bothers them a lot. People understand that retirement income gets taxed, the distance between awareness and action is large. The data tells a story of widespread concern paired with minimal preparation, where the Americans who stand to lose the most from a surprise tax bill are the ones least equipped to prevent it.

Key Findings

- 32.8% of near-retirees have no retirement tax plan. Among Baby Boomers, that rises to 36.3%.

- 58.9% of those earning under $25K have never heard of required minimum distributions (RMDs).

- Nearly 40% of Gen X is entering retirement without meaningful tax preparation.

- 53% of retirees earning under $25K say even a tax bill under $1,000 would feel like a financial crisis.

- 26.6% of retirees wish they had contributed to a Roth account instead of a traditional one, their top regret.

- 27.4% of retirees are skeptical it is even legally possible to cut their retirement tax bill in half.

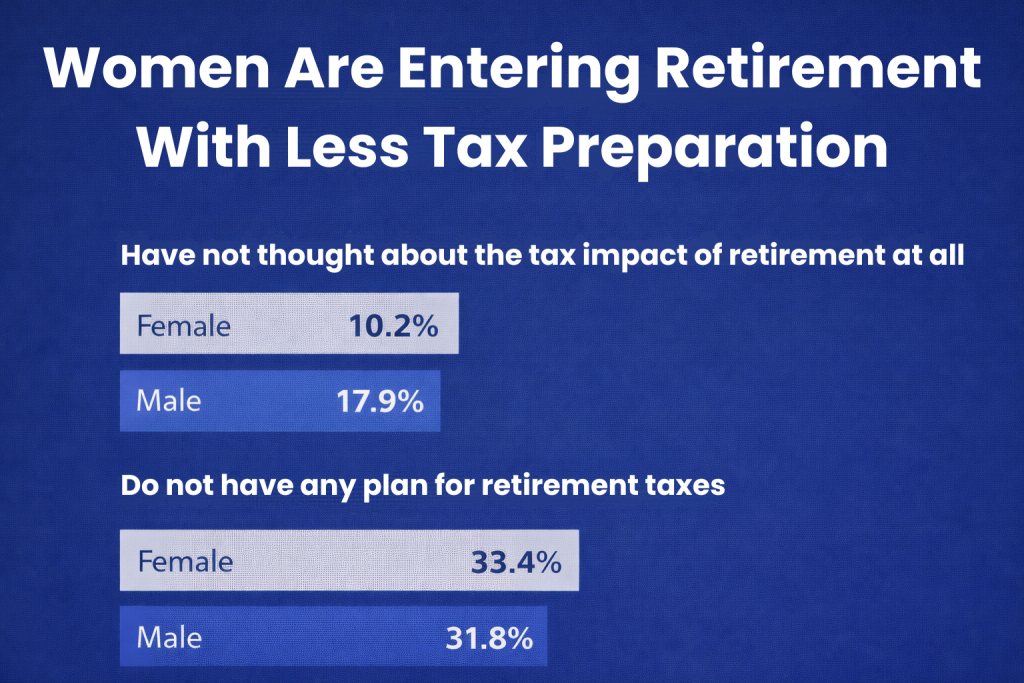

- 17.9% of women say they have not thought about the tax impact of retirement at all, compared to 10.2% of men.

The RMD Rule That Millions Have Never Heard Of

Required minimum distributions are one of the most consequential rules in retirement taxation. Starting at age 73, the IRS requires retirees to withdraw a minimum amount from traditional retirement accounts each year, and to pay income tax on every dollar. Miss the deadline, and the penalty is steep.

Yet 58.9% of Americans earning under $25K say RMDs were news to them. Among those with a high school diploma as their highest education, 51.5% had never heard of the rule. Compare that to earners in the $100K to $249K range, where only 15.4% were unaware. Education level is the strongest predictor of RMD awareness. The tax rule that forces people to take, and pay taxes on, their own retirement savings is still invisible to millions of the people it affects most.

Gen X Is Running Out of Time to Get Its Tax Strategy Together

Gen X is now crossing the retirement threshold, but their readiness remains at a standstill. 23.3% say they are not very confident in their retirement tax approach. Another 16.3% say they have not thought about taxes at all. Combined, nearly 40% of Gen X respondents are entering retirement without meaningful tax preparation.

This generation sits at an inflection point. Many are old enough to have built significant retirement savings but young enough that a few strategic moves could still lower their lifetime tax bill. A Roth conversion, for example, lets you move money from a traditional IRA into a Roth IRA, pay taxes on it now at a known rate, and withdraw it tax-free later. Withdrawal sequencing means choosing which accounts to pull from first, such as drawing down taxable accounts in early retirement and letting tax-advantaged accounts grow longer.

Both strategies work best with time, and Gen X still has some. The data suggests most are not using it. For a generation that has weathered the dot-com crash, the 2008 recession, and pandemic-era volatility, the tax side of retirement planning is an unfinished chapter.

Small Tax Bills Hit the Hardest Where Incomes Are Lowest

53% of those earning under $25K say a retirement tax bill of less than $1,000 would feel like a serious financial crisis. Among those earning $100K to $249K, that figure drops to 9.2%. The gap illustrates a structural problem: the tax system does not scale its emotional or financial impact evenly.

A $500 tax bill hits differently when your only income is Social Security and a small pension. For someone earning $200K with multiple accounts and an advisor, a $5,000 surprise is manageable. For a retiree living on $20K a year, $500 means choosing between groceries and a medical bill. These lower-income retirees are also the ones most likely to owe taxes they did not expect, on Social Security, IRA withdrawals, pensions, and part-time work. And they are the least likely to have professional help seeing those bills before they arrive.

The Biggest Retirement Tax Regret: Not Going Roth Sooner

26.6% of respondents say their top retirement tax regret is not contributing to a Roth account instead of a traditional one. Another 24.9% wish they had worked with a tax-focused financial advisor earlier. These two regrets together point to a single missed opportunity: tax-efficient planning done early enough to matter.

Roth accounts allow retirees to withdraw money tax-free in retirement, but contributions are made with after-tax dollars. The trade-off makes the most sense when someone is in a lower tax bracket during their working years, a situation that applies to many younger workers and mid-career earners. The catch is that most people do not think about retirement taxes until they are already in or near retirement, by which point the Roth advantage has shrunk. Financial literacy programs and employer-sponsored education have begun to emphasize Roth options more aggressively, but the survey data shows the message is still arriving too late for many.

A Quarter of Retirees Do Not Believe Legal Tax Savings Are Real

When told they could legally reduce their retirement tax bill by half through better planning, 27.4% of respondents said they would be skeptical if it is even possible. Among Baby Boomers, that skepticism rate is 28.1%. Among women, 29.4%.

The strategies behind these savings are well-documented. Roth conversions, strategic withdrawal sequencing, Social Security timing coordination, and charitable giving strategies are all legal, widely used, and available through qualified advisors.

The gap is not in the availability of tools, but in belief. A significant share of retirees do not think the opportunity exists, so they never seek it out. That skepticism creates a self-fulfilling outcome: people who do not believe in tax savings do not pursue them, and their tax bills stay exactly where they feared.

Women Are Entering Retirement With Less Tax Preparation Despite Needing It More

17.9% of women say they have not thought about the tax impact of retirement at all, compared to 10.2% of men. Women are also more likely to report having no retirement tax plan (33.4% vs. 31.8%) and more likely to say they cannot afford professional help.

Women, on average, live longer than men in retirement. That means more years of withdrawals, more RMD cycles, more exposure to shifting tax brackets, and more opportunities for a surprise bill. The combination of longer retirements and less preparation creates a compounding risk. Organizations like AARP and the Women’s Institute for a Secure Retirement have flagged this disparity for years, yet the survey data shows the gap persists. Closing it will require more than awareness. It will require accessible, affordable tax planning targeted at the populations most affected.

Summary / Takeaway

The Retirement Tax Surprise Index paints a picture that is more nuanced than simple financial illiteracy. Most Americans sense that taxes will matter in retirement. Many worry about it. But worry without knowledge, and knowledge without a plan, leaves millions of retirees exposed to bills they did not see coming.

The widest gaps fall along predictable lines: income, education, gender, and generation. The people closest to retirement are often the least prepared for its tax consequences. The people with the fewest financial resources feel the greatest pain from the smallest surprises.

What the data makes clear is that retirement tax planning is not a niche concern for the wealthy. It is a basic financial need that most Americans are not meeting. The retirees who fare best will not be those who saved the most. They will be those who understand what happens to their money after they stop working.

Methodology

To understand how Americans approach retirement tax planning, we surveyed 1,000 adults across the country who are near or currently in retirement. Participants answered a series of questions about their awareness of retirement tax rules, their level of preparation, their confidence in their tax strategies, and their emotional and financial readiness for potential tax surprises. Responses were analyzed by demographic groups, including age, gender, household income, education level, and ethnicity, to identify trends and disparities.

Fair Use Policy

Users are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.