Wondering about retirement? It looks surprisingly different depending on where you are in the U.S. The amount you need to save and the age you can actually retire can change a lot from one state to another. This is mainly because of factors like the local cost of living, which affects how far your money goes. State tax policies and your access to retirement benefits also play a huge role in shaping your financial future. Ultimately, where you live can have a big say in what your golden years look like.

Key Findings

- 63% of Americans say high costs of living prevents them from saving more for retirement.

- 14% of Americans have withdrawn money from their retirement savings in the past 12 months to cover everyday living expenses.

- 20% of baby boomers don’t have any retirement savings.

- 25% of Americans are not confident in their understanding of retirement planning.

- 42% of women feel anxiety around retirement planning, compared to just 23% of men.

- 37% of people are cutting back on travel/vacations and dining out to save for retirement.

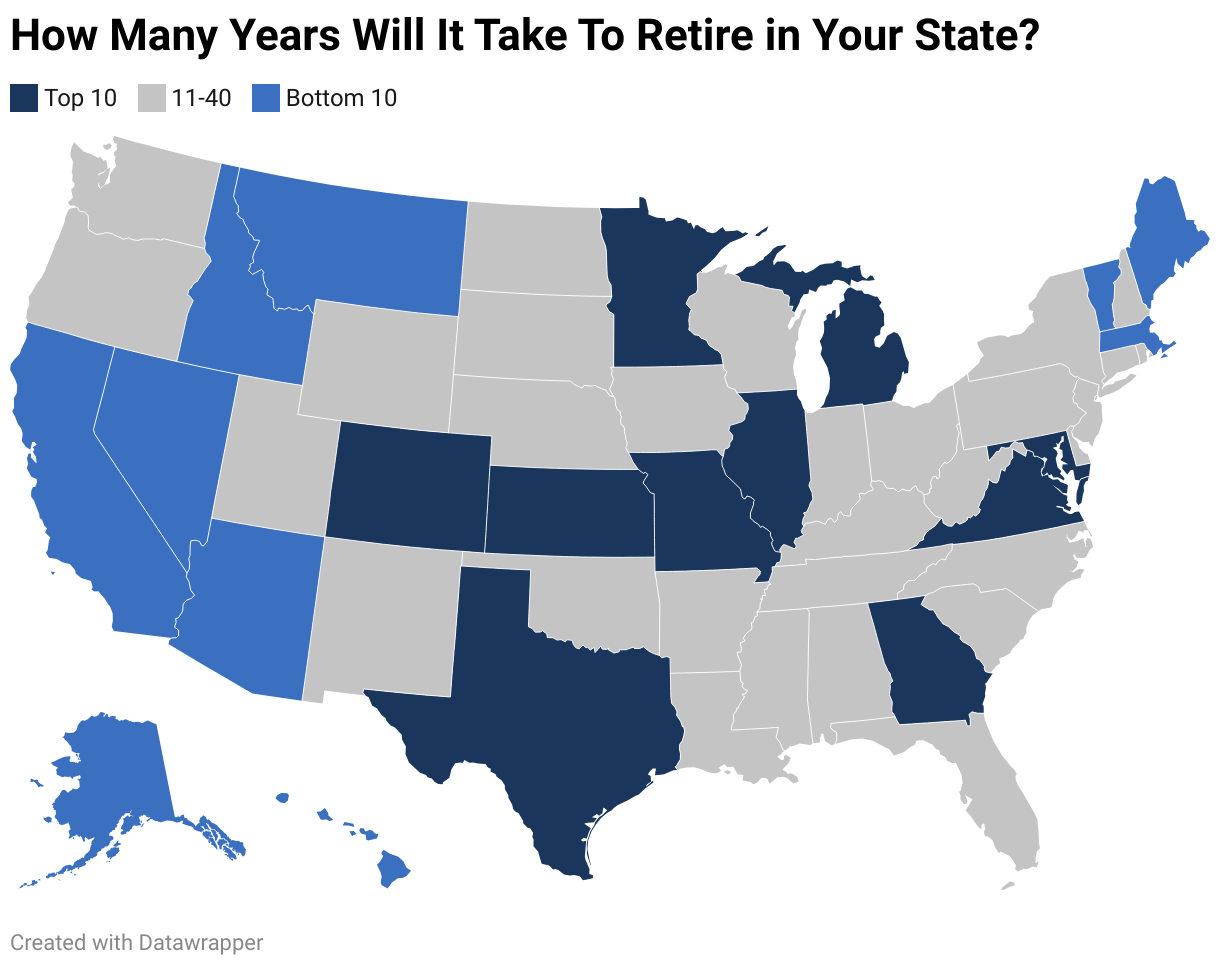

Top 10 Fastest States For Retirement

We determined the best and worst states to retire based on wage data and average annual expenses. Average wages were calculated using Bureau of Labor Statistics (BLS) data from May 2024.

Retirement goal amounts and average annual expenses were pulled from GoBankingRates. The number of years to retire was calculated by dividing retirement goal amounts by the difference between average wages and average expenses.

Illinois

Illinois offers retirees a winning combination of financial advantages and vibrant amenities. According to our analysis the average resident needs $873,646 to comfortably retire. Given the state’s competitive wages and relatively low cost of living it takes 26 years to retire.

Minnesota

Along with abundant natural beauty and outdoor opportunities, living in Minnesota offers significant benefits for retirees. With average annual wages of $68,880 and modest yearly expenses of $35,911, the typical Minnesota resident can expect to retire in 26 years.

Georgia

Georgia offers retirees a standout combination of financial comfort and affordability. Average annual expenses are relatively low at $34,180, and residents earn about $64,210 per year. In this welcoming fiscal environment, Georgia residents can be financially ready for retirement in 27 years.

Michigan

Michigan is an attractive retirement destination thanks to its moderately lower cost of living. Facing annual expenses of only $34,540, Michigan residents can be ready to retire in 29 years, and retirees are able to enjoy a more relaxed lifestyle without draining their savings.

Virginia

While annual expenses in Virginia are moderately higher, this is more than offset by a highly competitive average wage of $72,060. While Virginians need more money to retire than people in other states, high pay means the typical resident can be ready for retirement in 29 years.

Texas

Along with the benefit of no state income tax, retirees in Texas can enjoy low annual expenses of $35,094. Together, these factors make Texas an especially attractive state for stretching retirement dollars while enjoying a comfortable lifestyle. With average yearly wages of $63,660, Texans can comfortably retire in 29 years.

Kansas

Kansas stands out for retirees thanks to its notably low cost of living, with average annual expenses totaling $33,031. This allows families to stretch their income while working and prepare for retirement. Thanks to these low expenses, the average Kansas resident can retire in 29 years.

Missouri

Missouri’s relatively low cost of living makes it a haven for retirees on a budget. With average annual expenses of $33,594, residents can save more efficiently during their working years and prepare themselves for a comfortable retirement. While wages in Missouri aren’t as competitive as other states, residents can retire in 30 years thanks to low annual expenses.

Maryland

Maryland’s average annual wage of $76,130 reflects its diversified economy and educated workforce, and enables residents to comfortably save for retirement during their working years. Despite Maryland’s relatively high living costs, residents can typically retire in 31 years.

Colorado

Colorado boasts four national parks, including the iconic Rocky Mountain National Park, and numerous state parks.Colorado is a paradise for active retirees. With a higher than average wage of $71,960.00 Colorado offers a great opportunity to save and invest in retirement at 31 years.

Top 10 Slowest States For Retirement

Hawaii

Retiring in Hawaii is a dream for many, offering a unique blend of natural beauty and a relaxed island culture. However, the decision to spend your golden years in the Aloha State comes with a significant set of trade-offs, primarily centered around the high cost of living coming in at $76,828. The combination of wage and cost of living means you may never see retirement if you live and work on the Islands.

California

Retiring in California offers an unparalleled lifestyle with a vibrant culture and beautiful scenery, but it comes at a significant financial cost of around $57,195.While Social Security is exempt, other forms of retirement income are taxed at some of the highest rates in the country. Potentially keeping retirement 71 years away.

Massachusetts

Massachusetts has a rich blend of history, culture, and top-tier amenities, but these benefits come with a high price tag. Despite a strong wage opportunity at $83,050, the cost of living is some of the highest in the nation at $59,797. Bringing retirement timeline to 71 years.

Alaska

Alaska provides a unique experience for those seeking adventure and financial benefits, but it comes with significant challenges, particularly regarding the climate and cost of living. With a cost of living at $49,887, and wages at $72,810, these factors mean retirement could be up to 56 years in the making

Vermont

Vermont offers a peaceful, scenic lifestyle with a strong sense of community, but it comes with significant financial and weather-related challenges. Vermont is not considered tax-friendly for retirees. With a relatively high cost of living at $45,500, this means a timeline of 55 years to retirement.

Maine

Maine offers a unique coastal lifestyle with four distinct seasons, but it’s important to weigh the financial realities. Maine taxes most forms of retirement income, including withdrawals from 401(k)s and IRAs and property taxes are also significant. With the cost of living at $42,393, retirees are looking at 54 years to retirement.

Arizona

Arizona is a very popular choice, especially for those looking to escape cold winters there are some drawbacks to those warm benefits. While moderately tax-friendly. Social Security benefits are not taxed, but the cost of living has been steadily increasing for many years sitting at $42,083 meaning it could take up to 48 years for retirement.

Nevada

Nevada is a popular choice, largely due to its significant tax advantages, there is no state income tax, which means your Social Security benefits, withdrawals from 401(k)s and IRAs, and pensions are not taxed at the state level. There is also no inheritance or estate tax. However the cost of living at $42,083 means retirement could be 47 years away.

Idaho

Idaho has become increasingly popular, offering a blend of outdoor adventure and a more relaxed pace of life. With a lower than average wage of $58,440 and a steady increase in the cost of living in more urban areas at $37,706, these factors mean retirement could be 47 years in the making.

Montana

Montana, “The Last Best Place,” appeals to those seeking wide-open spaces and a rugged, natural lifestyle. With no statewide sales tax your dollar can go further, but the combination of wage $58,160 and cost of living $39,468 can stretch retirement up to 46 years.

State Taxes and Retirement: The Top 5 and Bottom 5 U.S. States for Retirement and Taxes

As Americans plan for their golden years in a challenging economic climate, a new analysis reveals a stark financial divide across the country, underscoring a critical truth: where you live in retirement can be as important as how much you’ve saved. A state’s tax code can either preserve a nest egg or drain it with astonishing speed.

This comprehensive review of state income, property, sales, and estate taxes identifies the best and worst states for retirees, highlighting a landscape of both tax havens offering financial freedom and tax traps that can devastate a fixed income.

For those planning their future, here are the top 5 retirement tax havens and the 5 biggest tax traps in the nation for 2025.

The Top 5 States for Retirement Tax Benefits

These states offer a powerful combination of low taxes and financial freedom, allowing retirees to keep more of their hard-earned money.

- Wyoming: The nation’s gold standard for tax-conscious retirees. It boasts no state income tax, meaning all retirement income is tax-free. This is coupled with some of the lowest property and sales tax rates in the country.

- Nevada: A winning hand for retirees. The Silver State has no income tax and no estate or inheritance taxes. Its low property tax rates provide significant relief, making it a top destination.

- Florida: The classic retirement paradise for a reason. The Sunshine State’s powerful combination of no state income tax and no estate tax provides a massive financial advantage for its millions of senior residents.

- Alaska: The Last Frontier of low taxes. Alaska has no state income tax and no statewide sales tax. As a unique bonus, it even pays residents an annual dividend from its oil wealth fund.

- South Dakota: A hidden gem on the plains. South Dakota offers a potent mix of no income tax, low sales taxes, and a favorable property tax environment, providing retirees with complete financial peace of mind.

The 5 Worst States for Retirement and Taxes

On the other side of the financial spectrum, retirees in these five states face a much harsher reality, with policies that can take a significant bite out of a fixed income.

- Nebraska: This state delivers a one-two punch with taxes on most retirement income, including 401(k) and pension distributions, and some of the highest property tax rates in the nation.

- California: The Golden State’s high cost of living is matched by its steep tax rates. While Social Security is exempt, its high income tax rates apply to all other retirement income, and its top-tier sales taxes diminish purchasing power.

- Connecticut: Retirees face a costly web of taxes here, including taxes on Social Security for many residents, high income taxes on other retirement funds, and notoriously steep property taxes.

- Minnesota: The tax landscape can feel frigid for retirees. It’s one of the few states that taxes Social Security benefits on top of high income tax rates for pensions and 401(k) withdrawals.

- Rhode Island: This small state packs a big tax bite. It taxes most forms of retirement income, including Social Security for many, and couples that with high property and sales taxes.

Financial experts urge prospective retirees to look beyond climate and lifestyle and perform a detailed “tax x-ray” of their top destinations before making a final decision that could impact their finances for decades to come.

Barriers to Retirement Savings in the U.S.

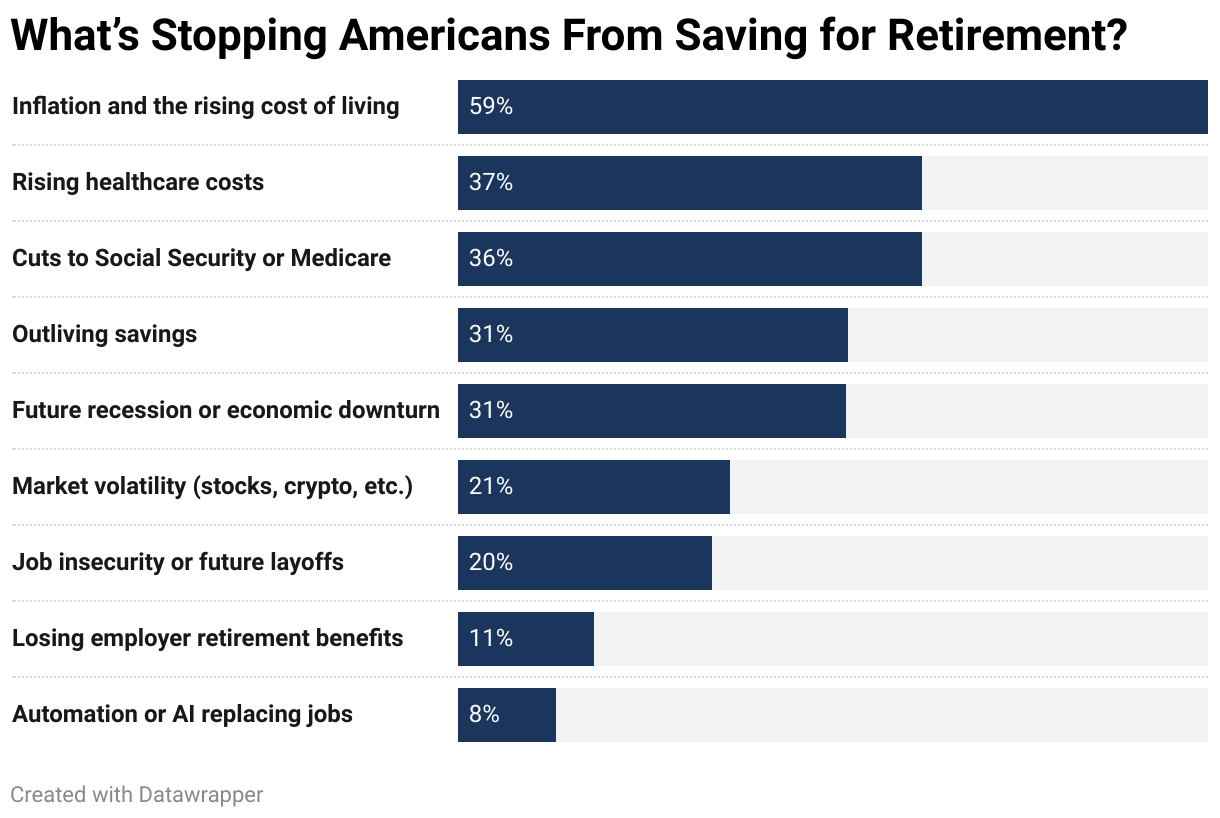

The persistently high cost of living is creating a two-front battle for Americans trying to secure their financial future. Not only is it hindering their ability to save, but it’s also forcing many to deplete the nest eggs they already have. In our survey of 1,000 Americans it was revealed that 63% say today’s high costs of living have prevented them from saving more for retirement.

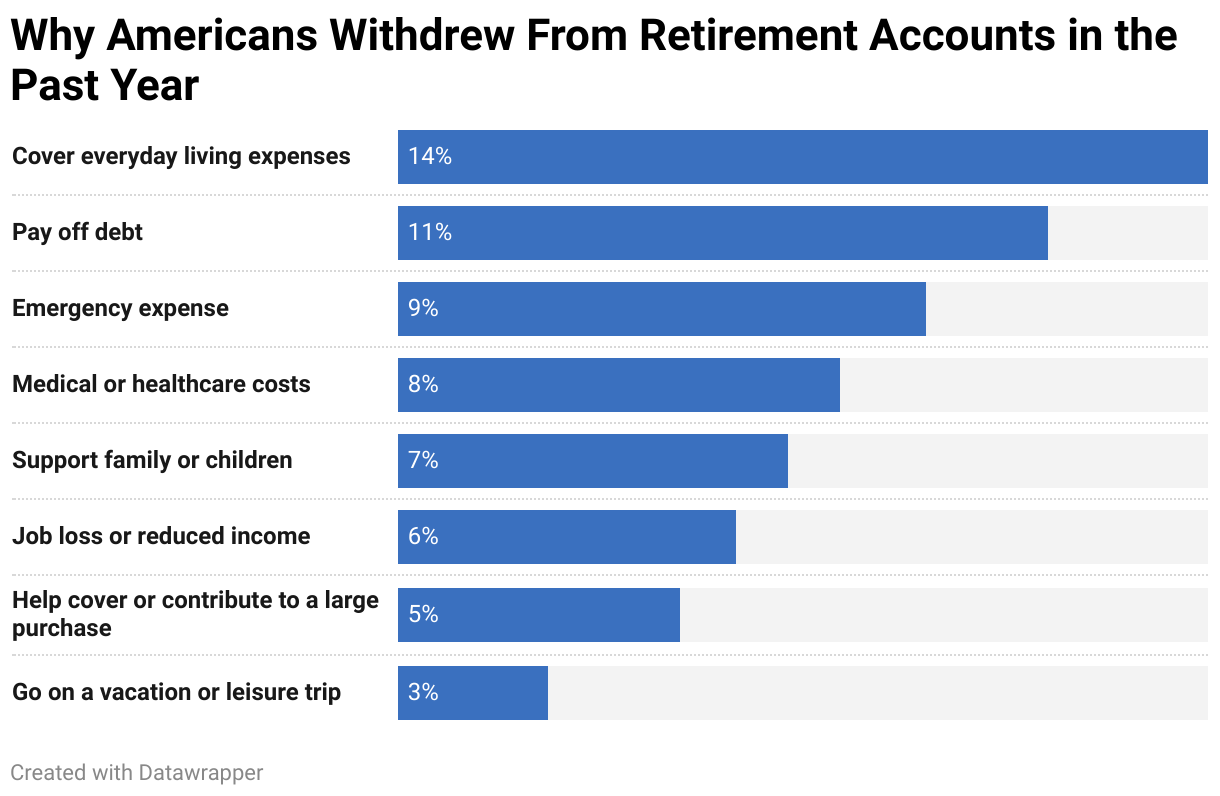

At the same time, the relentless financial pressure has pushed 14% of Americans to take the drastic step of withdrawing from their retirement accounts in the past year, using the funds to cover fundamental day-to-day expenses rather than major emergencies.

Financial strain is forcing the youngest generation of American workers to sacrifice their future savings, a new study finds. A startling 24% of Gen Z is forced to stop or pause contributions to their retirement and savings accounts to cope with today’s high cost of living. While a majority of Gen Z (58%) and half of Millennials (50%) are managing to contribute as usual, the data highlights a significant and growing portion of young adults being derailed from their long-term financial goals.

Not-So-Golden Years: Who’s Falling Behind?

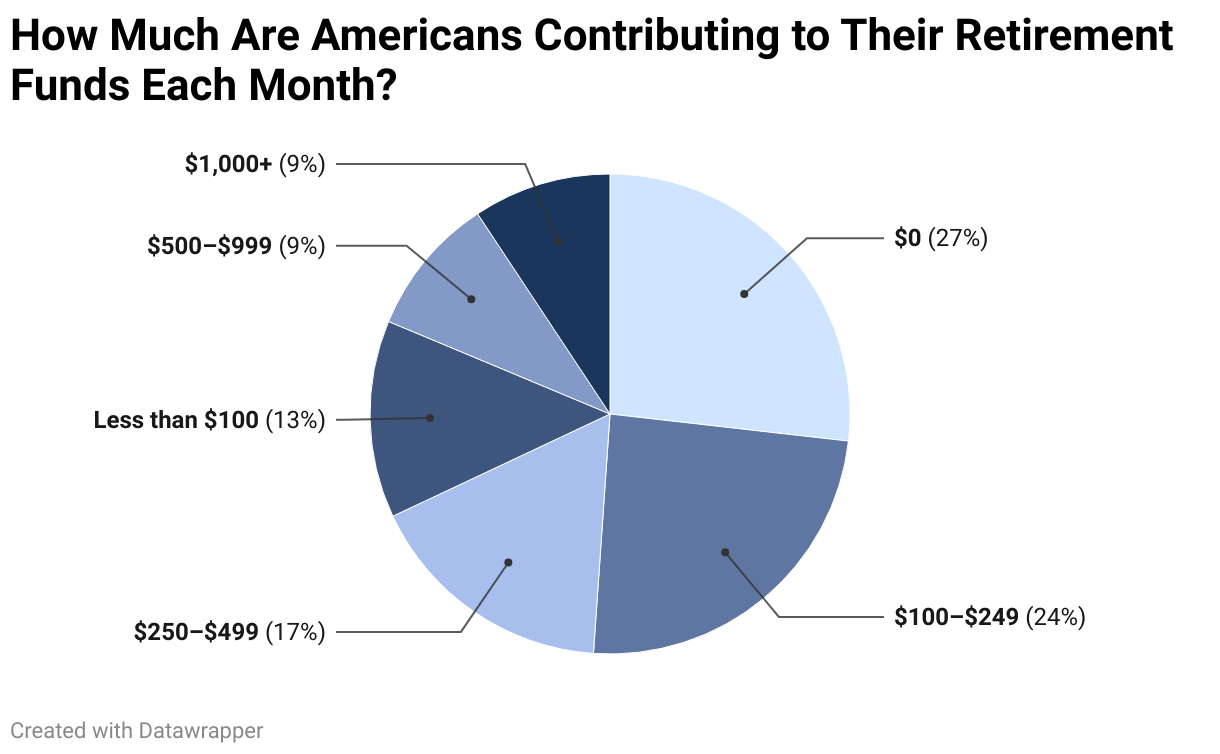

How Americans are saving for retirement is largely a story told by their generation, with each facing unique circumstances that shape their financial journey. Overall findings indicate that 30% of Americans’ target retirement savings are under $500,000.

- Gen Z (Ages 12-27): This generation is surprisingly engaged with retirement planning, starting to save at a median age of 20. Despite their early start, their savings are modest, with an estimated median of $31,000 in household retirement accounts. They are often juggling competing financial priorities, such as paying off debt and saving for major life events, with 41% reporting that they are just trying to cover basic living expenses.

- Millennials (Ages 28-43): Often called the “sandwich generation,” many Millennials are caught between the financial pressures of raising children and caring for aging parents. This, combined with the burden of student loan debt, has significantly hampered their ability to save. Despite starting to save at a median age of 26, their median household retirement savings stand at $65,000. A staggering 59% report that debt is interfering with their ability to save for retirement.

- Gen X (Ages 44-59): As the first generation to primarily rely on 401(k)s instead of traditional pensions, Gen X faces a significant retirement savings gap. They began saving later, at a median age of 30, and have a median of $107,000 in household retirement savings. Many are not confident in their ability to achieve a comfortable retirement, with 45% reporting that their savings are behind schedule.

- Baby Boomers (Ages 60-68): Now in or nearing retirement, this generation’s savings vary widely. They started saving for retirement at a median age of 35 and have a median of $270,000 in household retirement accounts. While some are well-prepared, a concerning 20% of Baby Boomers have no retirement savings at all. Many are facing a shortfall, with 39% expecting to retire at age 70 or older, or not at all.

Saving for Retirement: A Tale of Two Genders

A significant retirement savings gap exists between men and women, with men generally accumulating more savings. This disparity stems from a combination of economic, social, and behavioral factors that compound over a lifetime, leaving women at a financial disadvantage in their later years.

The most prominent is the gender pay gap. Women, on average, earn less than men for comparable work. This lower income directly translates to less disposable income available for retirement contributions.

Another major factor is career interruptions. Women are more likely than men to take time out of the workforce or reduce their hours to care for children or other family members.

In our study, 23% of women do not contribute to retirement savings, compared to only 14% of men; this directly reflects the issues of lower pay and career breaks.” (Adding a semicolon or rephrasing slightly makes the relationship clearer). Or, “In our study, the fact that 23% of women do not contribute to retirement savings, compared to only 14% of men, directly reflects the issues of lower pay and career breaks.

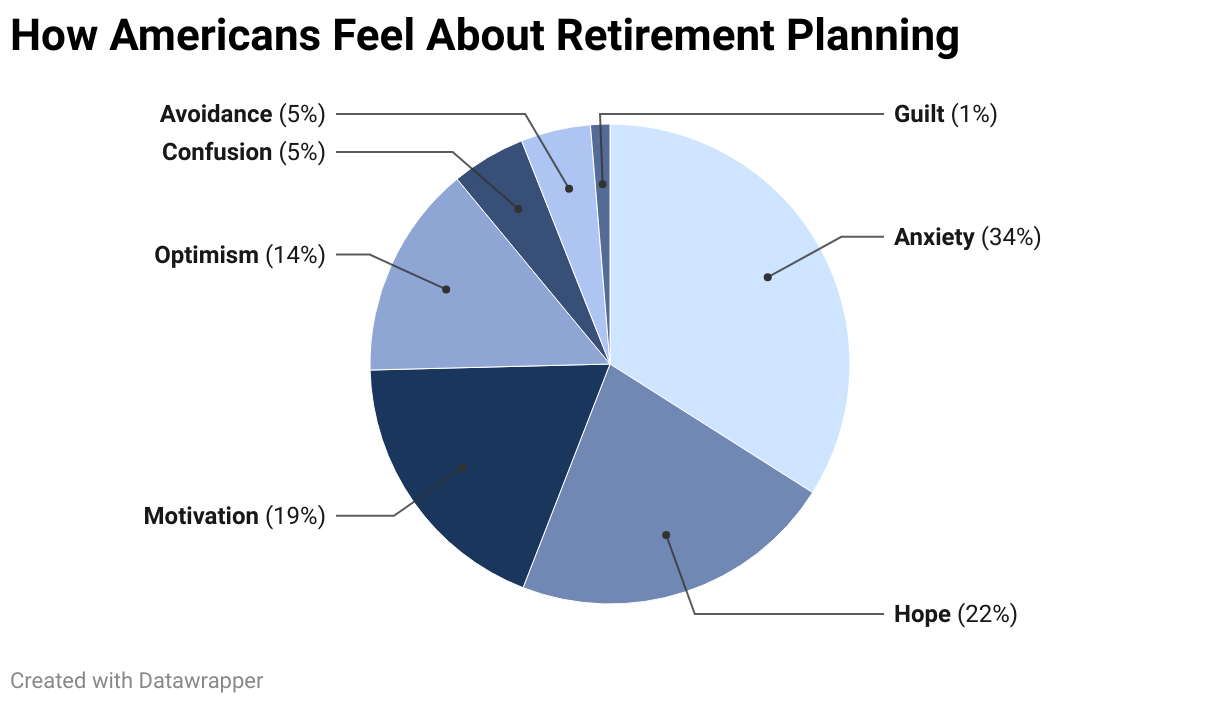

Retirement Woes and Sleepless Nights

The dream of a secure retirement is being overshadowed by a growing and often unspoken crisis: a significant decline in mental well-being. Financial experts and mental health professionals are sounding the alarm that the immense pressure of retirement planning is evolving from a simple financial exercise into a major source of chronic stress, anxiety, and even depression.

In our study of 1000 Americans 34% experienced anxiety when thinking of their retirement plans while 42% of women felt greater anxiety compared to 23% of men.

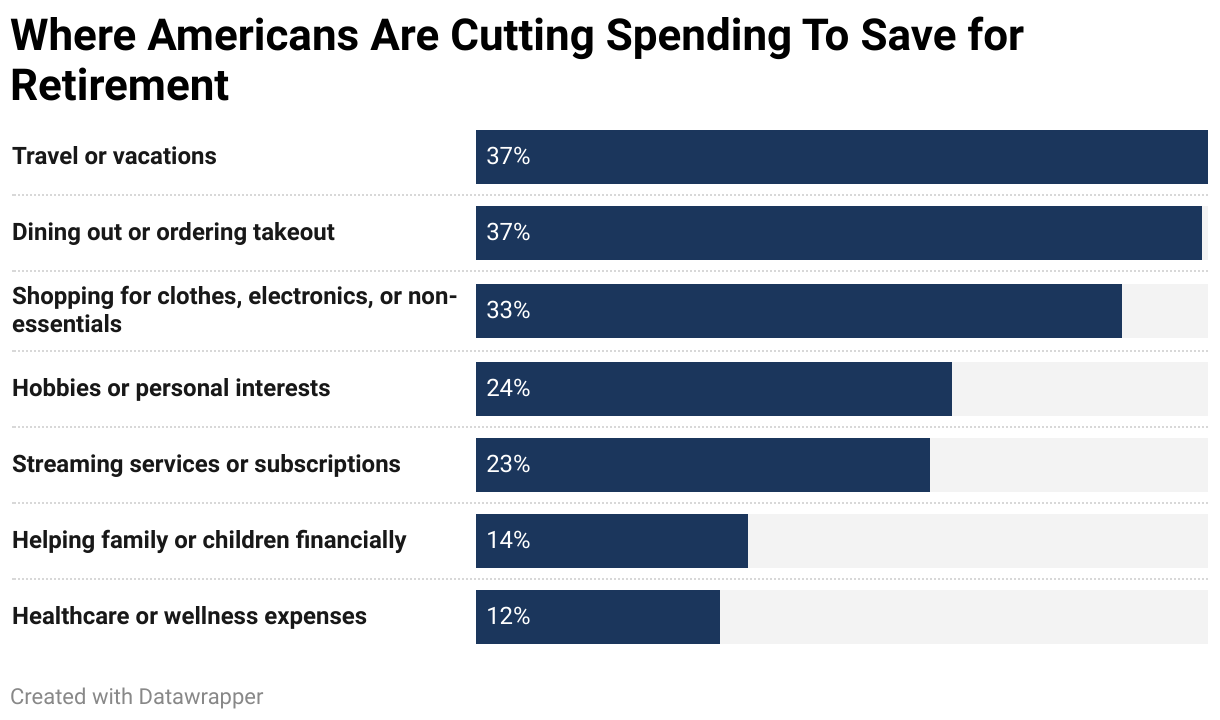

The Retirement Diet: Trim the Budget, Feed the 401(K)

In the relentless pursuit of a secure retirement, a growing number of Americans are making profound sacrifices, trading present-day joys and milestones for the promise of future financial stability.

A new analysis of household spending and saving habits reveals a trend: from delaying homeownership and parenthood to forgoing vacations and even necessary healthcare. According to our study 37% of Americans are cutting travel/vacations and dining out in order to meet their retirement needs.

Taking on extra work and adding a side hustle to life is becoming more and more important 46% of Americans are doing more and taking on extra work or side hustles to meet their financial needs.

The “Forever Work” Fear: Millions Believe They Will Never Retire

Perhaps the most startling trend is the growing sentiment among a significant portion of the population that they will never be able to fully retire. The report highlights that a striking 20% of all Americans believe they’ll be working into their seventies.

Additionally, concerns about the viability of retirement appear to affect younger Americans more commonly, as one in four working Americans under the age of 50 now believe they will likely have to work for the rest of their lives.

Rising housing, healthcare, and daily living costs make it difficult for many to put away enough money, even when they work consistently. Combined with uncertainty about Social Security and investment market volatility, it’s no surprise that a large portion of Americans doubt they’ll ever feel financially secure enough to stop working.

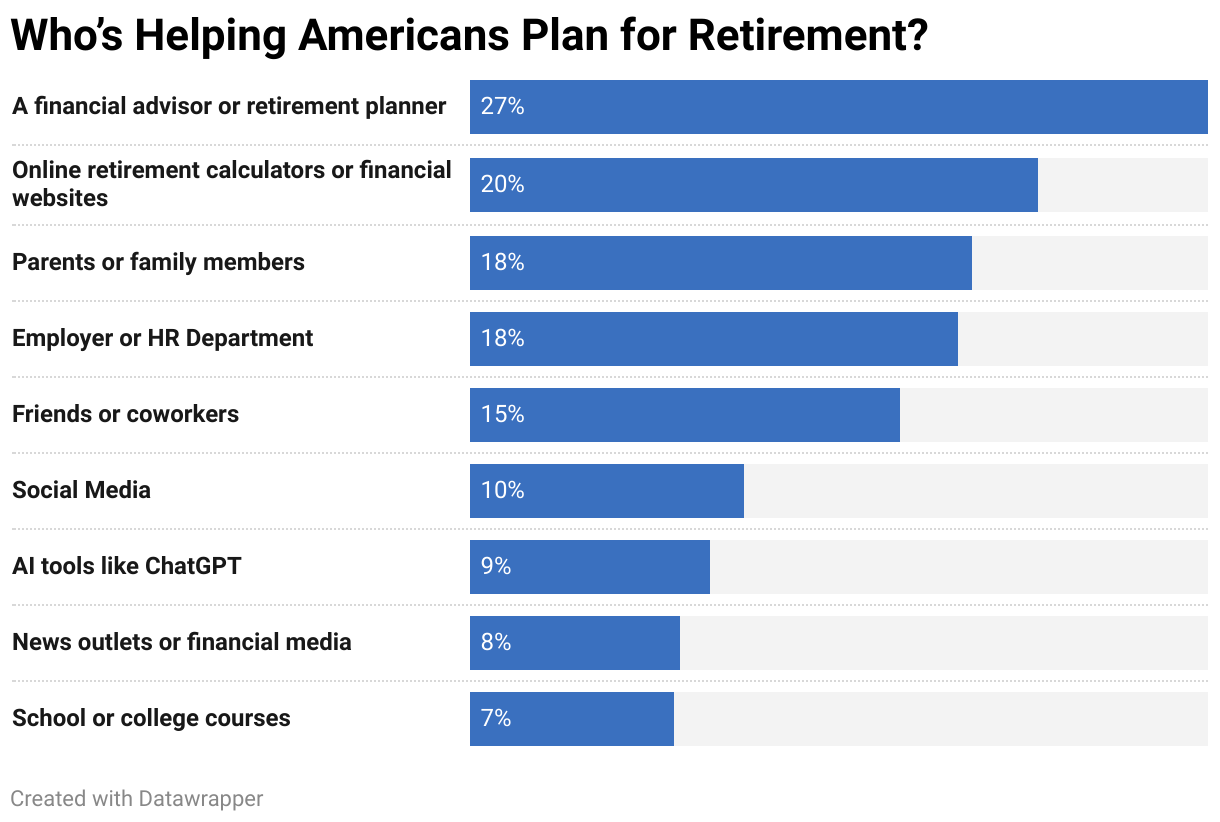

Faking It ‘Til You Make It (To Retirement)

Retirement planning is still a hypothetical concept for many Americans. In fact, 83% currently have no concrete retirement plans worked out. Additionally, 25% say they are not confident in their understanding of retirement planning, with 10% saying they haven’t given retirement any thought at all.

For those feeling overwhelmed, there are a variety of resources that can help, ranging from financial advisors and retirement planners who provide tailored strategies, to employer-sponsored programs that often include free planning tools and education. Online retirement calculators and robo-advisors also give people an accessible way to model different scenarios and track progress.

For many retirees, annuities are an attractive option because they provide a reliable stream of income, often guaranteed for life, which helps reduce the risk of outliving one’s savings. They offer peace of mind by converting a lump sum into predictable monthly payments and can serve as a supplement to Social Security or pension benefits.

Beyond financial stability, annuities can also include features like spousal continuation or inflation protection, making them a flexible tool for tailoring retirement security to personal needs.

When evaluating options, annuity calculator tools are especially useful—they allow individuals to quickly compare quotes, project monthly payouts, and adjust for variables such as age, gender, and payout duration. For example, a $300k annuity might provide a steady but modest income stream, enough to cover essentials or supplement other savings.

In contrast, a $500k annuity would generate significantly higher monthly payments, offering more room for discretionary spending, travel, or healthcare costs. The choice between them often comes down to lifestyle goals and financial confidence in retirement, with calculators providing a clear, personalized picture of what each option delivers.

Retirement planning may feel daunting, but understanding the challenges, exploring your options, and seeking professional guidance can make the journey far less uncertain. With the right mix of strategies and support, Americans can turn worry into confidence and create a retirement plan that fits both their needs and dreams.

Methodology

To understand the issues facing those wanting to retire and those close to retirement we surveyed 1,000 adults across the country. Participants answered a series of questions about their experiences with retirement in their respective lives. Responses were analyzed by demographic groups to identify trends and disparities.

To calculate how many years an individual needs to work before reaching retirement, we used the following formula:

Years to Retire = Retirement Goal ÷ Annual Savings Potential

- The Retirement Goal is based on the estimated cost of retirement in a specific state, taking into account local living expenses and life expectancy.

- Annual Savings Potential is calculated by subtracting average expenses from the average wage, and then adding the individual’s self-reported monthly savings (multiplied by 12).

Annual Savings Potential = (Average Wage – Average Expenses) + (Monthly Savings × 12)

This method provides a straightforward estimate of how long it might take someone to save enough for retirement, based on their financial situation and where they live.

Fair use policy

Users are welcome to use the analyses and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. However, when referencing or citing this article, please ensure proper attribution. Direct linking to this article is permissible and encouraged to provide readers with access to the primary source.

For commercial use or publication purposes — including but not limited to media outlets, websites, and promotional materials — please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.