Born between 1997 and 2012, Gen Z has come of age in a world transformed by the internet and rocked by crisis after crisis. From 9/11 and the 2008 financial meltdown to COVID-19 and deepening political divides, this generation has faced near-constant upheaval while trying to build their lives and careers.

So, how are they coping amid soaring costs, and what does their money mindset look like? We surveyed 1,000 Gen Zers to uncover their biggest financial fears, boldest goals, and how they’re grappling with the growing pressure to stay afloat in today’s economy.

Key Findings

- 92% of Gen Z job seekers demand pay transparency, and 49% won’t apply if the salary is hidden

- 41% of Gen Z borrowed money for groceries or rent in the last year

- Nearly 50% say money stress is hurting their mental health — and 1 in 4 is losing sleep over it

- 85% believe the minimum wage should be at least $20/hour

- 1 in 5 Gen Zers overdraw their accounts to pay basic bills

- 45% still live with their parents due to financial instability

- 1 in 2 plan to start a side hustle this year

- 58% say Trump-era tariffs and job cuts are making their finances worse

- 37% couldn’t survive a month without a paycheck

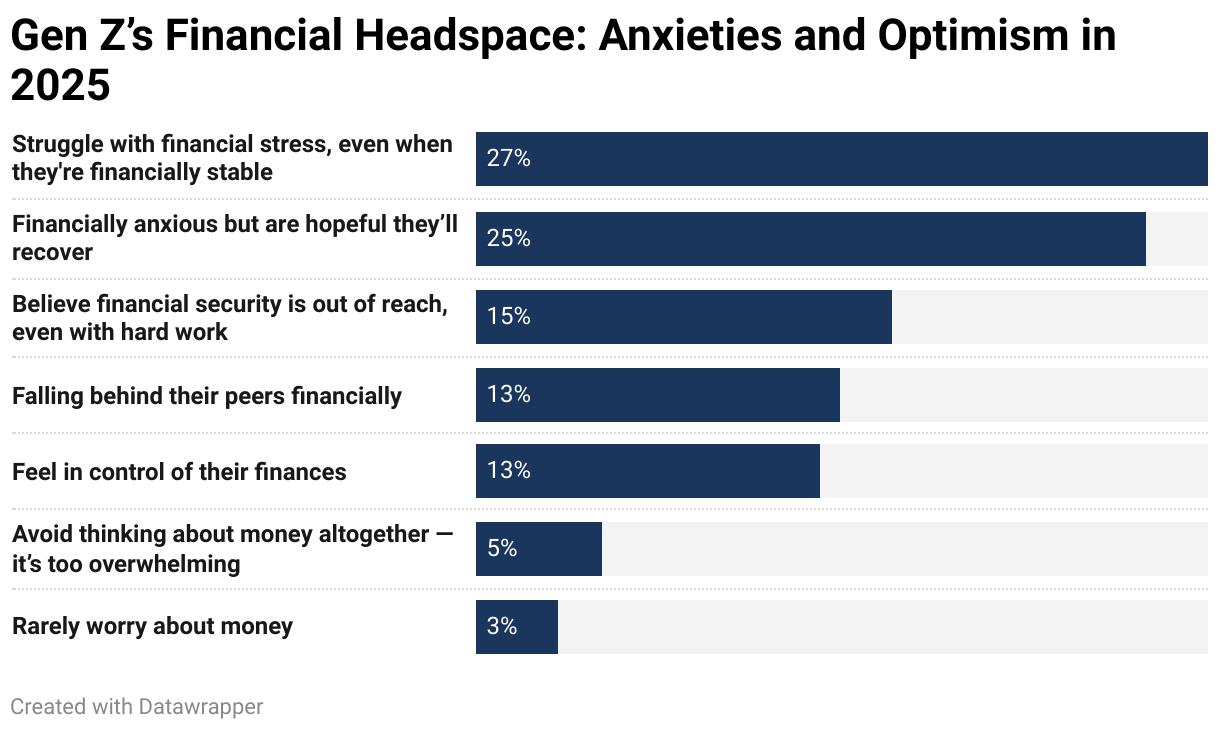

3 in 5 Gen Zers Doubt They’ll Reach Financial Stability

Money anxiety is the norm for Gen Z: 27% are stressed about finances, even if they’re relatively stable, while just 3% rarely worry.

With many crises to point to in their lifetime, this generation is carrying the emotional weight of an economy that rarely feels safe.

- 27% struggle with financial stress, even when they’re financially stable.

- 25% are financially anxious but are hopeful they’ll recover.

- 15% believe financial security is out of reach, even with hard work.

- 13% are falling behind their peers financially.

- Only 13% feel in control of their finances.

- 5% avoid thinking about money altogether — it’s too overwhelming.

- 3% rarely worry about money.

Women Bear a Heavier Burden

Gen Z women feel more financial anxiety than their male counterparts.

They’re 42% more likely than men to believe they’ll never be financially secure. They’re also twice as likely as men to feel overwhelmed by money.

Further widening the gap, men are 36% more likely than women to feel confident about their financial future.

The Toll on Mental Health

Financial stress isn’t just economic — it’s emotional, contributing to a mounting mental health burden. 3 in 5 (60%) say money is taking its toll. Here’s how it plays out:

Low-income earners face nearly double the mental health toll of their high-earning peers.

Among those earning under $50,000, 31% feel depressed or hopeless, and 38% are distracted by money daily — nearly twice the rate seen among those earning $150,000 or more.

While financial stress affects every income group, those living paycheck to paycheck carry the heaviest emotional burden.

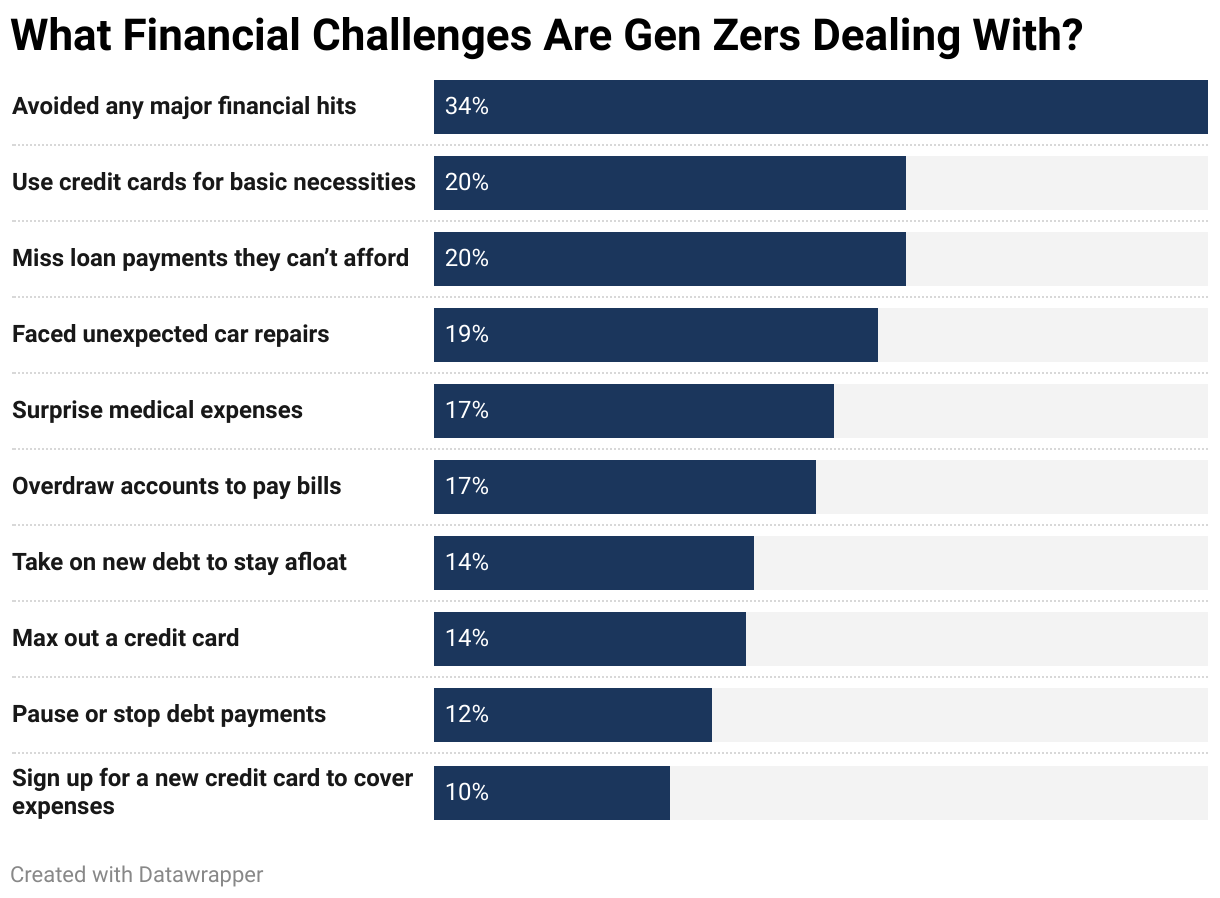

The Financial Challenges of Gen Z

Many Gen Zers (44%) are all too familiar with using credit cards to supplement their financial well–being. What older generations saw as red flags, they view as routine parts of financial life.

The reality is that just keeping up with bills means sacrificing long-term goals and quality of life.

Here’s what they have to give up:

Gen Z’s Financial Priorities: Saving Tops the List, But Reality Gets in the Way

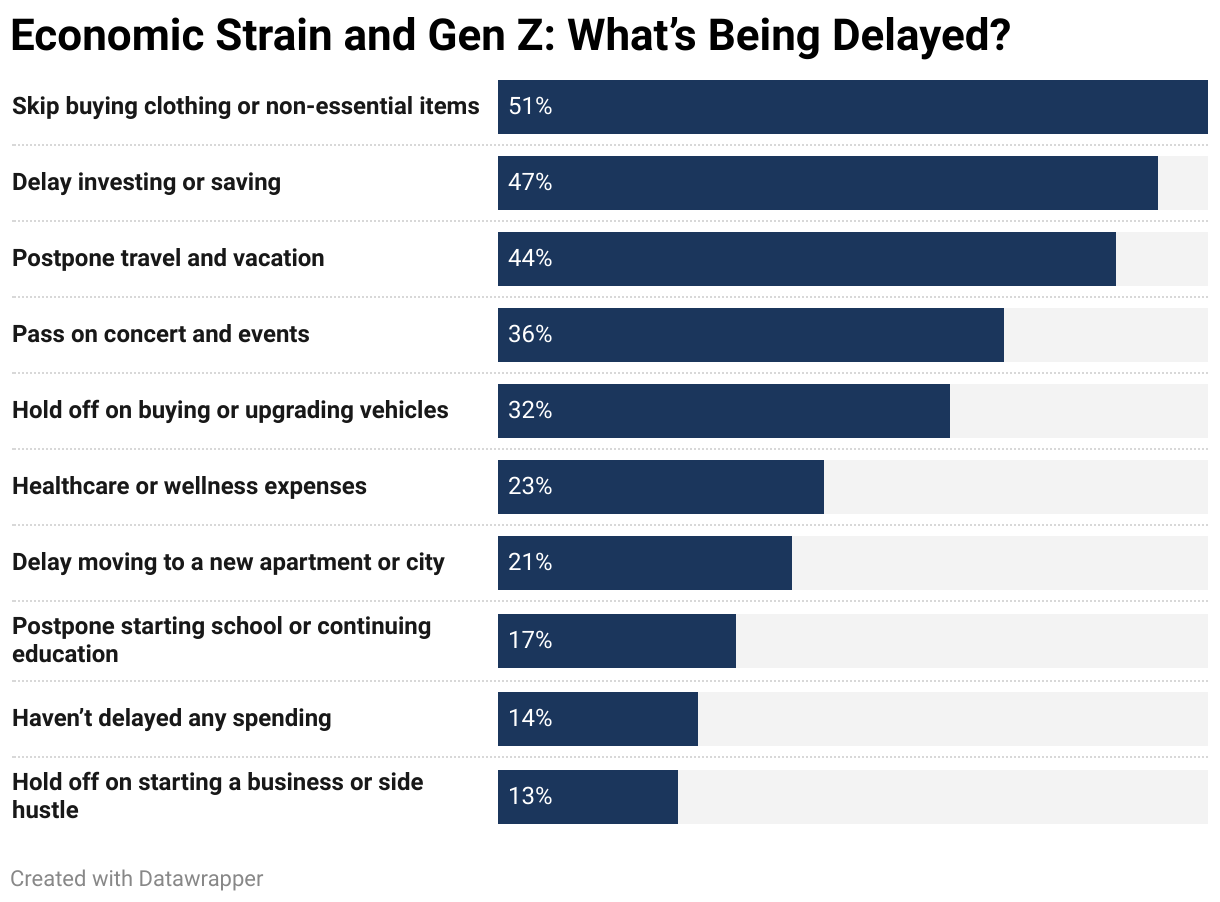

Like generations before them, Gen Z dreams of long-term stability and a secure retirement. But chasing those goals amid economic uncertainty, mounting debt, and rising costs threatens to derail even the most responsible plans.

Still, many are undeterred, forging ahead with positive financial steps:

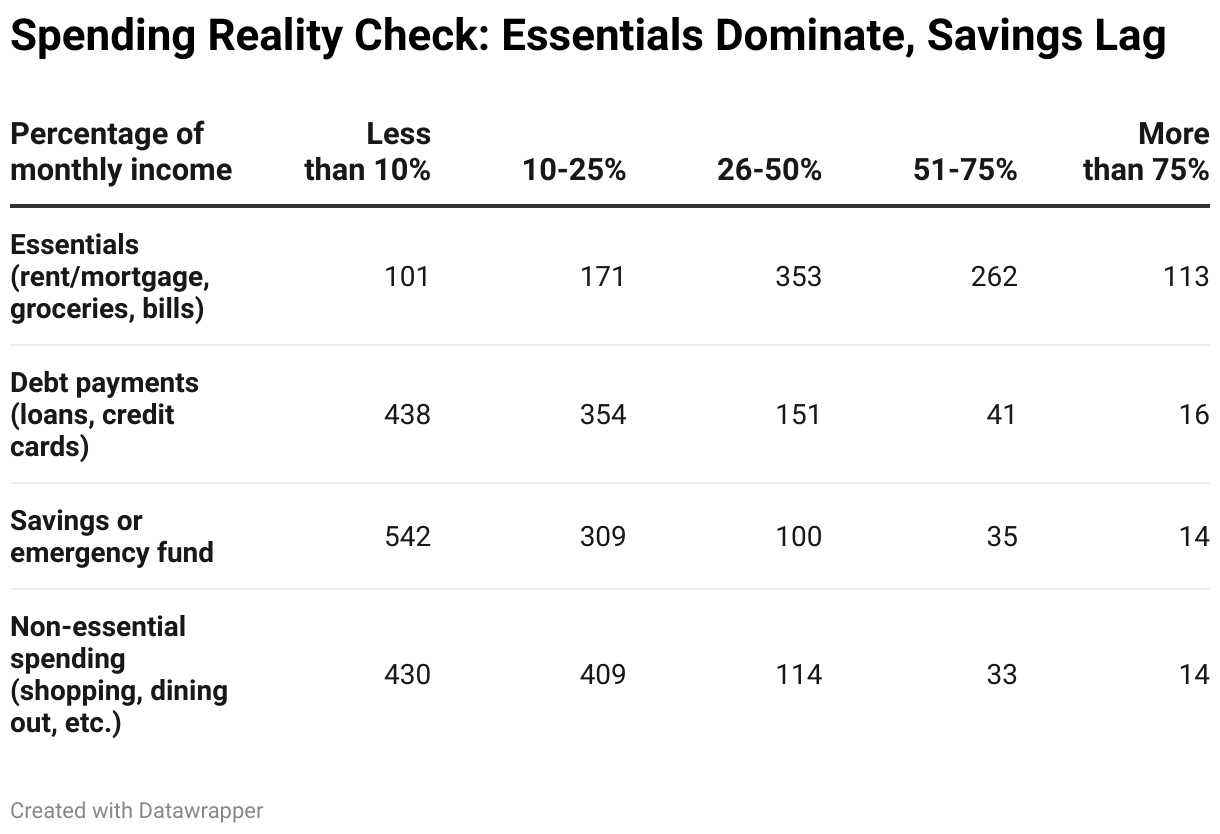

Debt Is Blocking Gen Z’s Saving Potential

More than half (54%) of Gen Zers save less than 10% of their income for emergencies — not because they don’t care, but because debt keeps getting in the way. Many aren’t drowning, but they’re swimming against the rapid current of student loans and credit card bills.

Here’s where that money goes each month:

Top monthly financial burdens include student loans, credit cards, car payments, mortgages, and personal loans.

Living on Loans: Gen Zers Struggling With Basic Living Expenses

41% of Gen Z have had to borrow money to cover their expenses, including essentials, like food.

Here’s where the money went for those who needed help:

With food prices projected to rise another 3.5% in 2025, most are already adapting — 80% say they’ve changed what they buy at the store to save money.

Meanwhile, just 13% haven’t changed their habits despite noticing price hikes, and an even smaller 7% haven’t noticed the rising costs at all.

Majority of Gen Z Are Fed Up With Trump’s Economic Playbook

58% of Gen Z say Trump’s economic policies are making their lives harder — and they’re not happy about it. Only 17% support his approach, while 1 in 5 remain indifferent.

A stagnant job market already has new graduates and entry-level workers struggling to gain career traction in their chosen fields. And government layoffs, surging prices, and budget cuts to academia and research are tightening the job market even further.

Money doesn’t change their minds — 61% of both low– and high-income earners are united in their frustration over Trump’s economic policies.

Tariffs Fuel Proactive Budget Shifts Among Gen Z

Gen Z isn’t just feeling frustrated about tariffs — they’re bracing for impact. Nearly one-quarter (23%) have already adjusted their finances to cushion against the fallout. 32% haven’t done anything, despite their concerns, while 16% believe tariffs won’t affect them whatsoever.

Every income level worries about tariffs, but income plays a role in how quickly they take action:

- 46% of those earning under $50,000 have already taken steps.

- 43% of those earning $50,000–$99,999 have done the same.

- 41% of those earning $100,000–$149,999 have adjusted their habits.

- 35% of those earning over $150,000 have made changes.

While lower-income Gen Zers are moving fastest to adjust, even the wealthiest are preparing for rough terrain. This broad sense of economic vigilance signals something deeper — financial survival instincts may be a defining trait of this generation, not just a side effect of income level.

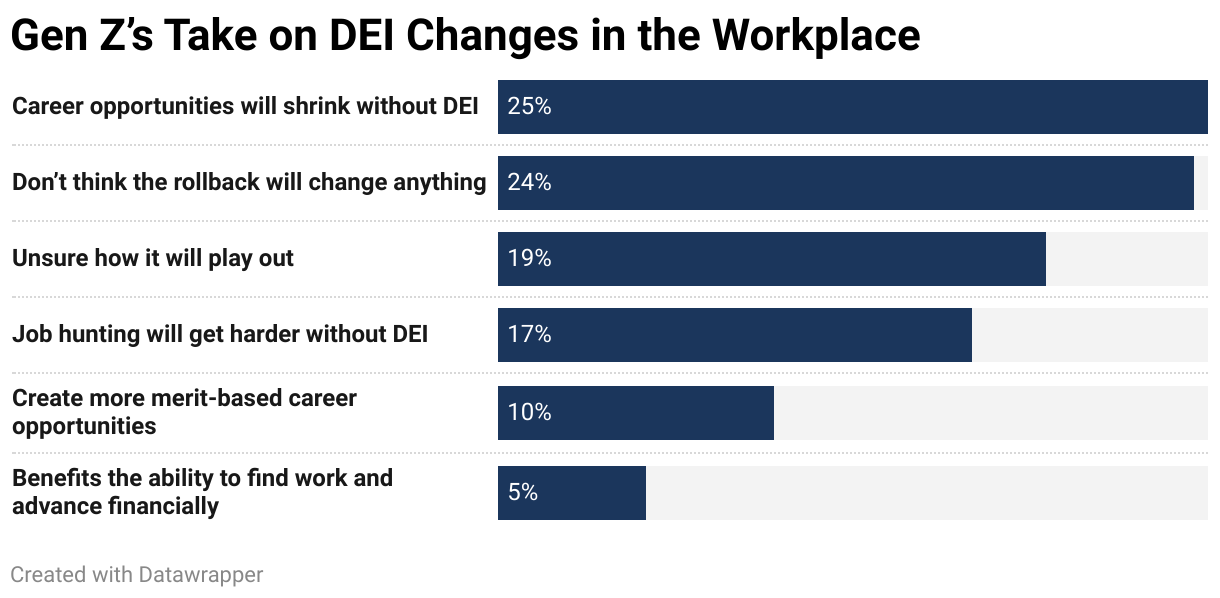

Diversity, Equity, and Inclusion Rollback Threatens Gen Z’s Career Opportunities

The Trump administration’s push to dismantle diversity, equity, and inclusion (DEI) programs is stirring unease. DEI efforts were designed to level the playing field for historically marginalized groups, but recent rollbacks, which extend beyond the public sector into the private workforce, are triggering concern among young workers about what lies ahead.

Gen Z is divided on the future of work as DEI programs disappear — some fear lost opportunity, others aren’t convinced it will matter.

Gen Z’s Gender Divide Telling Amid DEI Rollbacks

Women are 38% more likely than men to fear anti-DEI policies will hurt their job prospects.

Men are far more optimistic about the end of DEI: they’re 67% more likely than women to see it leading to more opportunity — and 60% more likely to say it won’t hurt their financial future.

These differences suggest that women feel more vulnerable to the loss of DEI protections — a reflection of the very gaps in opportunity those programs aim to close.

Many Gen Zers Feel Unprepared for Financial Emergencies

If a recession happens, young Americans could be the first to be out of a job. As the newest hires in many workplaces, younger employees often lack the seniority to weather large-scale layoffs.

If they lost their jobs today, 37% couldn’t even last a month. 30% could hold on for 3-6 months, and only 12% could survive beyond 6 months without any income.

According to the Bureau of Labor Statistics, 1 in 4 unemployed Americans are out of work for 27 weeks or longer. That’s over six months — far beyond what most Gen Zers are financially prepared for.

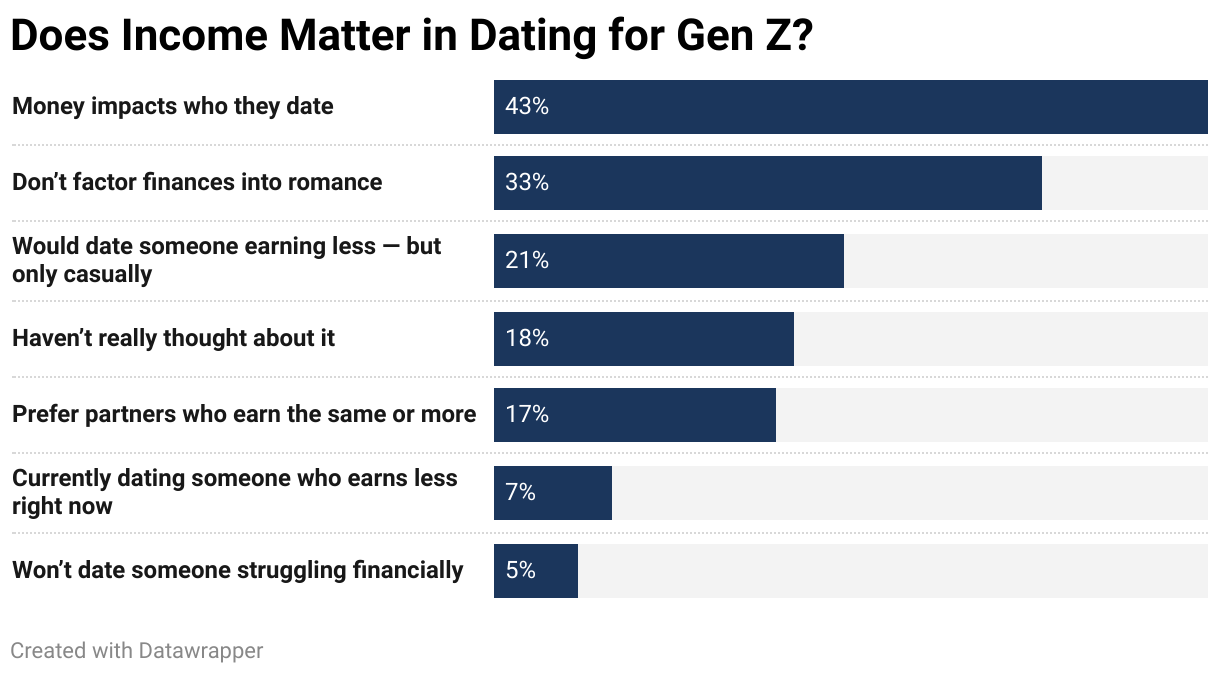

Financial Compatibility Matters in Gen Z Dating

But what about dating for financial gain? Gen Z is split: nearly half think it’s a smart move.

- 47% view entering a relationship for financial reasons as a savvy strategy.

- 40% see it as ethically questionable.

- 13% haven’t given it much thought.

1 in 10 are currently trying to find a more financially secure partner to help improve their own finances.

For nearly half of Gen Z, financial stability isn’t just a preference — it’s a prerequisite when it comes to dating:

When it comes to love and money, Gen Z’s views are not only nuanced, but they’re also deeply gendered. 40% of men say a partner’s finances don’t matter, compared to just 27% of women. Similarly, 23% of women prefer financially adept partners, while only 10% of men feel the same.

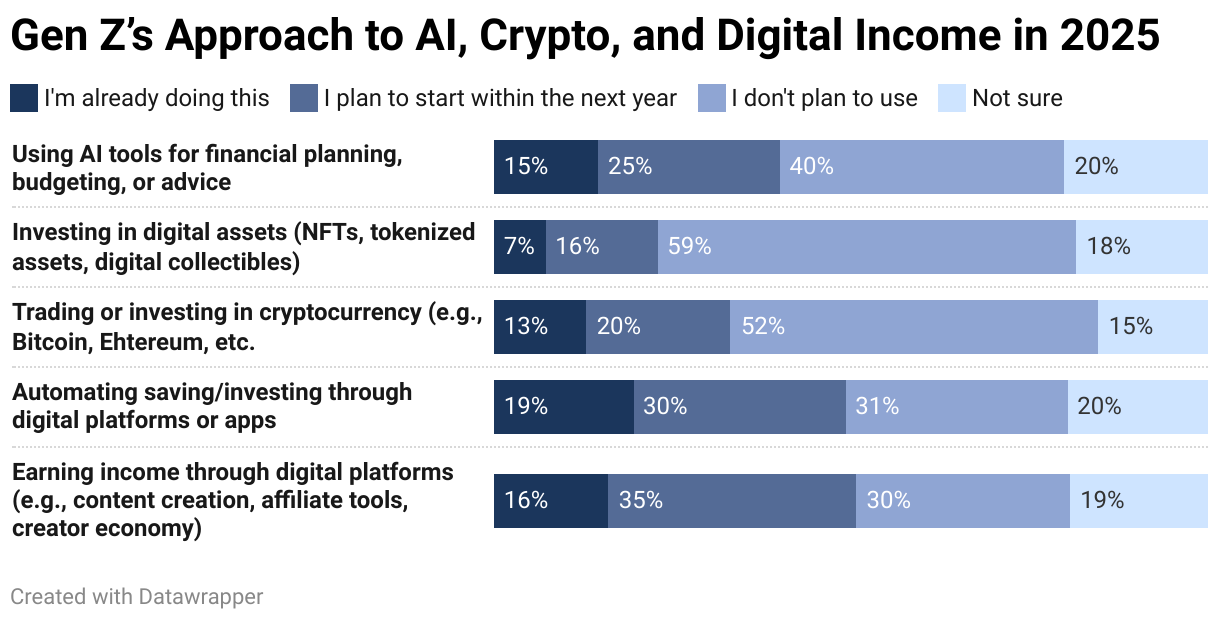

Gen Zers Making Use of Emerging Fintech for Extra Cash

More than half of Gen Z is tapping into or planning to explore online platforms to make money in the next year. Growing up online has shaped this generation into digital natives who are eager to use tech tools for budgeting, investing, and earning.

40% are embracing AI for budgeting — but most haven’t started yet. Just 15% are currently using AI tools to plan and manage their finances, while 25% say they plan to start soon.

Gen Z is also dabbling with trendier tech, like cryptocurrencies and non-fungible tokens (NFTs). 13% are already investing in crypto and an additional 20% plan to get started in the next year. This means crypto adoption is poised to jump 154% in the coming months.

Similarly, 7% have already invested in NFTs, and 15% plan to do so in the near future — more than doubling the number of investors among this demographic.

The takeaway? Gen Z is curious about innovation but careful about where they put their money. They’re cautious about volatile assets, but they’re transforming platforms like YouTube, Twitch, and OnlyFans into digital entrepreneurship lifelines.

The OnlyFans Economy: Gen Z’s Controversial Side Hustle

7% of Gen Zers have earned money through digital sex work platforms. Of these online sites, OnlyFans is arguably the most recognizable and controversial because it allows users to sell sexual content. Its peer-to-peer model allows users to earn quickly, which is especially attractive to those enduring financial strain.

Gen Z’s views on digital sex work reveal a generational divide between pragmatism and personal values:

More men (7%) have engaged in digital sex work than women (4%) — but women are more likely to legitimize it.

28% of women say platforms like OnlyFans are a valid way to earn income, compared to just 22% of men.

Surprisingly, support for digital sex work increases with income — not financial hardship.

Only 21% of those earning under $50,000 view it as legitimate, while that number jumps to 34% among those making between $100,000 and $149,000. Even among the highest earners ($150,000+), 26% express support.

This suggests the conversation around digital sex work may be less about economic survival — and more about changing views on labor, autonomy, and visibility in the digital age.

92% of Gen Z Job Seekers Want Pay Transparency

In a competitive, often unpredictable job market, 49% of job seekers refuse to apply for positions that don’t disclose pay upfront. Only 8% say salary transparency isn’t a priority; for the rest, it’s a dealbreaker.

Another 43% take a flexible stance — they prefer salary transparency but still apply to jobs that keep pay hidden. It’s a compromise that may reflect how tough the job market is, even as expectations rise.

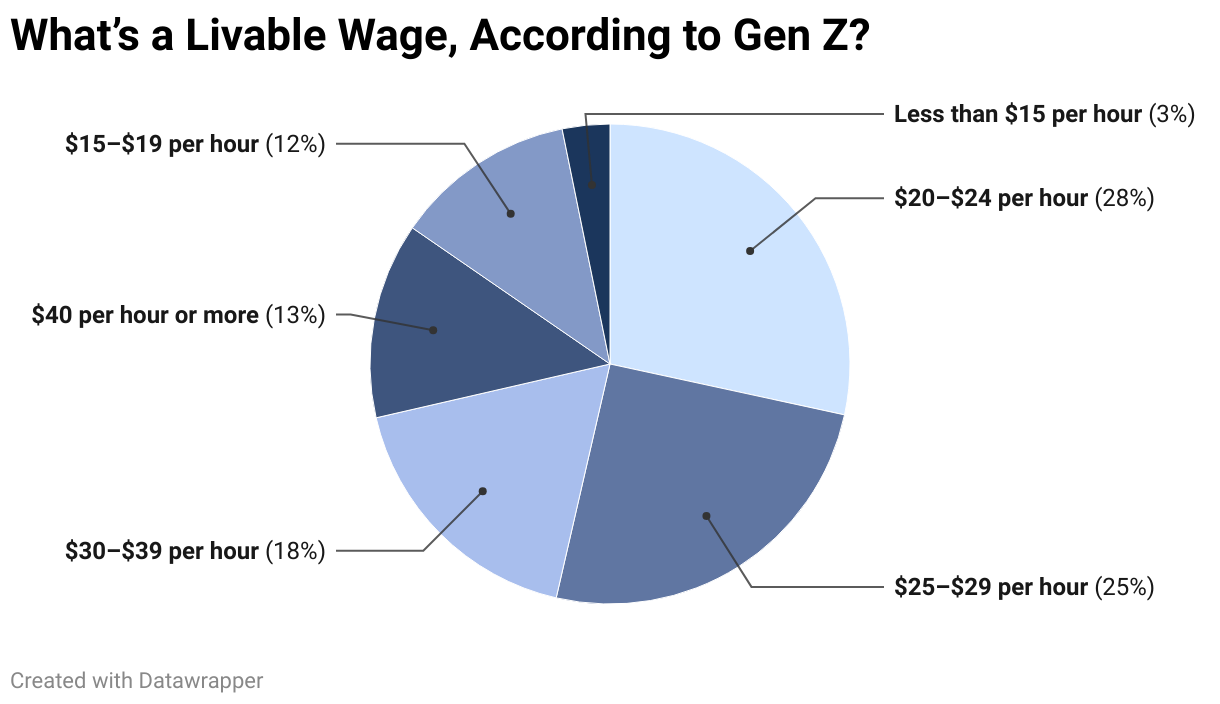

What Does Gen Z Consider a Living Wage?

25% of Gen Zers say that even $25 per hour isn’t a livable wage in the U.S., and an additional 31% believe it takes $30 per hour or more.

Ultimately, the disconnect between this belief and reality is massive, as this is far above what most U.S. states currently offer and the federal minimum. Even high-wage states like California and New York, with minimums between $15 and $19, still fall short.

Here’s what they consider to be a true living wage:

While pay expectations naturally vary by region, industry, or education level, this generation is united around one core belief: comfort shouldn’t come at the cost of survival.

More Than Half of Gen Zers Not Sold on the 40-Hour Workweek

Work-life balance is a top priority for this generation, and many believe full-time shouldn’t mean burnout. 52% say Americans should be able to live comfortably working fewer than 40 hours a week. An additional 8% take things even further, believing that people should be able to support themselves without working at all.

However, 41% accept working at least 40 hours per week as a necessary evil for a stable lifestyle.

Interestingly, those in higher income brackets are more likely to accept longer hours. Of top income earners, 35% believe a 40-49 hour work week is necessary to live well. Meanwhile, an equivalent number earning under $150,000 believe working 30-39 hours a week should be enough.

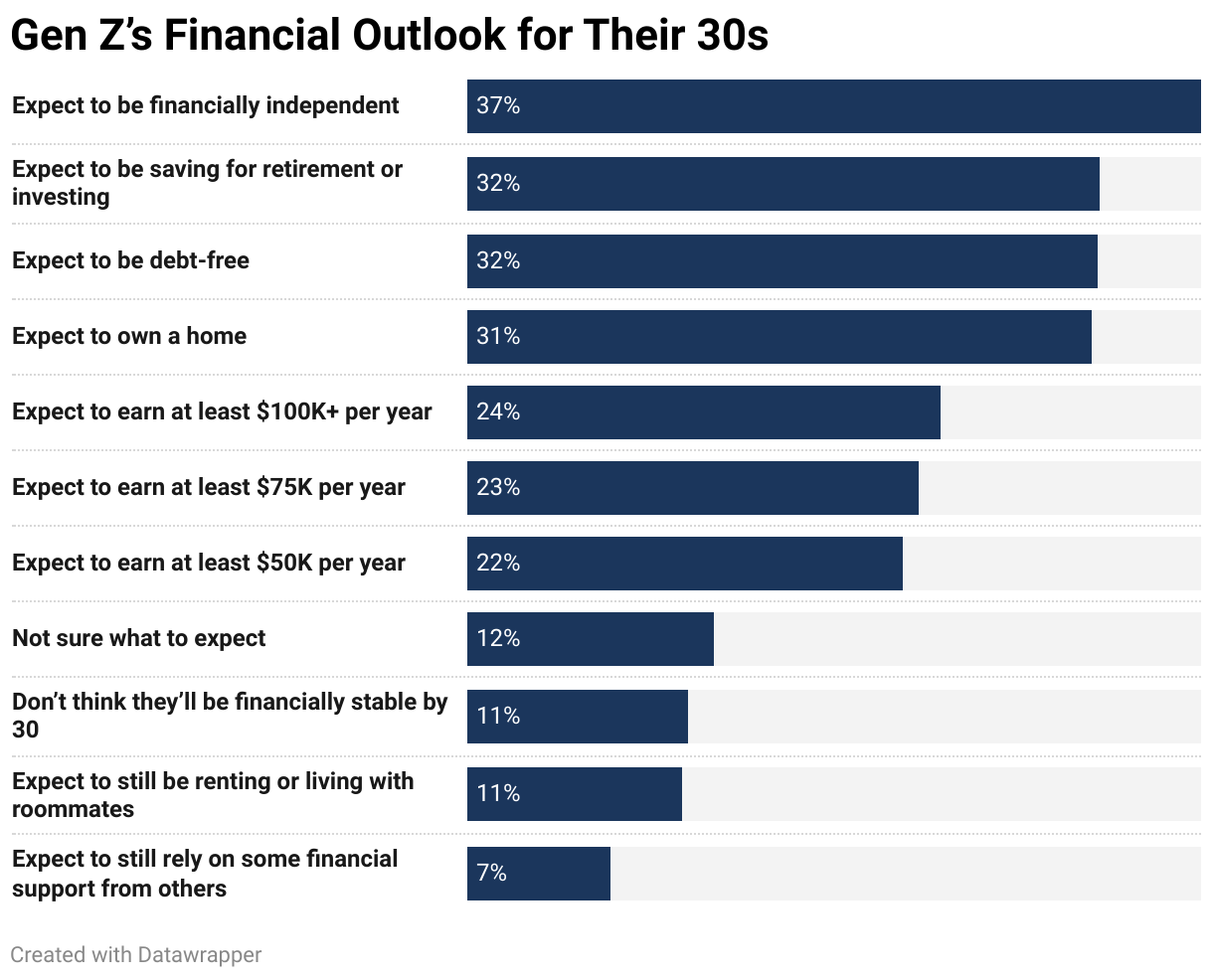

Gen Z Remains Hopeful Despite Present Challenges

Despite facing financial turbulence from every angle, Gen Zers are moving through their 20s with clear goals and cautious optimism. Here’s what they hope to accomplish by age 30:

Gen Z has big income goals for their 30s — and $100,000 is the new benchmark. While 22% expect to earn at least $50,000 and 23% aim for $75,000 or more, a full 25% believe they’ll be making six figures by the time they hit their 30s.

Though positive goals dominate the dreams of many, some are bracing for a rockier reality. After all, only 16% can afford to live on their own, and nearly half (45%) still live with their parents because they aren’t able to find their footing.

This is the financial future they envision:

- 1 in 10 don’t expect to be financially stable by 30.

- 1 in 10 expect to be still renting or living with roommates.

- 7% foresee relying on others to make ends meet.

Shaped by the 2008 crash, entering school or the job market during COVID-19, and a new wave of tariff fears and layoff anxiety, Gen Z knows better than to count on a stable future, but they haven’t stopped planning for one. They’re adapting in real time: cutting spending, adjusting expectations, and turning to digital tools to build resilience.

In the face of uncertainty, this generation is blending pragmatism with ambition and rewriting what preparedness looks like in the 21st century.

Methodology

This study draws on responses from 1,000 Gen Z participants, born between 1997 and 2012. To ensure a representative sample, we included individuals from various U.S. regions and income brackets.

We asked questions about general financial hardships and worries, specific concerns, and the use of fintech and online platforms for financial management and side hustles. We also covered the political climate and recent government decisions to see how these affected respondents’ financial outlook. Finally, we included quality-of-life questions about non-essential spending and living situations.

Together, these insights gave us a complete look at the financial actions, thoughts, concerns, and ambitions of Gen Z.

Fair Use Policy

Users are welcome to utilize the insights and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. When referencing or citing this article, please ensure proper attribution to maintain the integrity of the research. Direct linking to this article is permissible, and access to the original source of information is encouraged.

For commercial use or publication purposes, including but not limited to media outlets, websites, and promotional materials, please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.